Jobs and global supply chains in South-East Asia

Abstract

South-East Asia has become a key player in global supply chains (GSCs) during recent decades, and the region’s participation in GSCs has had a profound impact on labour markets. This paper presents new 2000–2021 estimates of the number of GSC-related jobs in the region, with an estimated 75 million workers linked to GSCs in 2021—or more than one in four workers. Over time, the region has become increasingly dependent on GSCs for employment despite some short periods of sharp volatility and setbacks, including in 2020, the first year of the COVID-19 pandemic. The paper also presents the results of an econometric analysis, finding that the region’s increased GSC participation was associated with some important, albeit mixed, progress in improving job quality. While deeper GSC integration was robustly tied to a rapid decline in working poverty and gains in labour productivity, it also shows that a positive relationship between increased GSC participation and greater wage employment, high-skill employment, and female employment was limited to specific sectors. Several policies could strengthen the links between GSCs and decent work. These include well-designed social protection and labour market policies, and investments in a broad range of skills that allow countries to shift into higher value-added segments of a value chain. Also, deep trade agreements, which increasingly include labour provisions, can help strengthen the link between increased GSC participation and decent work.

Acknowledgements

The authors are grateful for the valuable comments and inputs provided by David Bescond, Sotiris Blanas, Marva Corley-Coulibaly, Sukti Dasgupta, Sara Elder, Sajid Ghani, Sameer Khatiwada, Stefan Kühn, Elina Scheja and Paul Vandenberg.

Executive summary

Since 2000, South-East Asia has become increasingly dependent on global supply chains (GSCs) for employment despite some short periods of sharp volatility and setbacks. In 2021, an estimated 75 million workers had GSC-related jobs, or more than a quarter of total employment.

Some countries such as Singapore, Thailand and Viet Nam were more dependent on GSC employment than others such as Indonesia, the Lao People’s Democratic Republic (Lao PDR) or the Philippines. Likewise, manufacturing accounted for the highest share of GSC employment, while an increasing share of jobs in agriculture have become linked to GSCs, especially during the past decade.

Increased GSC participation in the region was associated with some important, albeit mixed, progress in improving job quality. While deeper GSC integration was robustly tied to the rapid decline in working poverty and gains in labour productivity, a positive relationship between increased GSC participation and greater wage employment and high-skill employment was limited to specific sectors.

GSCs do provide jobs for millions of women, as they work in sectors well-integrated into GSCs. However, enhanced GSC engagement is associated with employment gains for women only in sectors where jobs are typically less skill-intensive and lower paid.

Well-designed social protection and labour market policies are central to cushion any shocks GSCs propagate and how they are distributed. Investments covering a broad range of skills are needed to shift into higher value-added GSC segments. Also, deep trade agreements, which increasingly have labour provisions, can play an important role in strengthening the link between increased GSC participation and decent work.

Introduction

Globalization is one of the key drivers of “transformative change in the world of work, with profound impacts on the nature and future of work, and on the place and dignity of people in it.” 1 One way globalization manifests itself is through the proliferation of global supply chains (GSCs).2 Governments and social partners—including trade unions and employer associations—find it important to “foster more resilient supply chains that contribute to decent work.” 3 South-East Asia has become a key player in GSCs over recent decades, with the region’s GSC participation having a profound effect on labor markets, creating jobs for millions of workers. 4 South-East Asia is a very economically diverse region—including high-income, upper-middle, and lower-middle income economies, with varying degrees of GSC participation. The type of GSC economic activity also varies greatly, from low-cost, labor-intensive to high-value added, technology-intensive sectors.

Increased integration of the region’s economy into GSCs also affect job quality. For example, GSCs help some workers join the formal labor market. 5 Also, women are often delegated into lower wage or lower status employment, within and across sectors highly integrated into GSCs. In some cases, decent work deficits within GSCs remain severe, with evidence and reports of poor working conditions in GSC sectors. There are also important distributional implications of advanced and developing country participation in GSCs by way of increased wage inequality. 6 GSC participation has been associated with higher productivity gains in firms than gains in wages, raising concerns over these gains from GSC participation being shared fairly. 7

GSC employment in the region is deeply related to the broad macroeconomic context and other transformative dynamics. South-East Asia’s labor markets were heavily affected by the coronavirus disease (COVID-19) pandemic (Box 1). The current global economic environment—characterized by high inflation and geopolitical tension—will likely further hurt employment. Spiking commodity prices and tightening financial conditions, as well as exit strategies from the unprecedented stimulus taken in some advanced economies, will particularly affect countries in South-East Asia through the GSC channel. At the same time, major GSC transformations—including boosting their resilience and the longer-term efforts to decarbonize supply chains—are expected to impact South-East Asia’s labor markets. 8 While not necessarily having led yet to job losses at a large scale, technology is continuing to reshape GSCs—driving production processes, logistics and trade financing—affecting both jobs and tasks involved. 9

Box 1: The COVID-19 Pandemic and its Impact on Labour Markets in South-East Asia

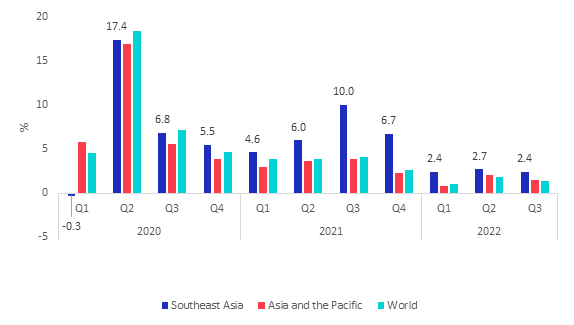

Labor markets in South-East Asia were hit hard by the pandemic. In 2020, aggregate working-hour losses—reflecting both contractions in employment and declining working hours for those still employed—were at 7.4 per cent relative to the fourth quarter of 2019. These working-hour losses are equivalent to more than 20 million full-time jobs, assuming a 48-hour work week. The second quarter 2020 had the highest working hour losses in South-East Asia, more than 17 per cent (Figure B1.1).

Due to various surges in virus infections, gaps in vaccine access and distribution, and containment policies, decreases in working hours in South-East Asia remained high in 2021 (6.8 per cent). Working hours are estimated to have remained below pre-crisis levels in 2022 as well, with a slower recovery in South-East Asia than elsewhere—as geopolitical uncertainties and increasing food and energy prices add to the pandemic impact.

Figure B1.

Source: ILO, ILOSTAT database, accessed 3 March 2023; ILO, ILO Monitor on the World of Work, 10th Edition, 2022.

Integration into GSCs can exacerbate and compound geopolitical, environmental and pandemic shocks, but they can also reduce vulnerability by diversifying suppliers and clients.10 What can policy makers do to leverage the large potential of GSCs for decent job creation, while at the same time addressing risks related to GSCs and their potential impact on labour markets? This paper contributes to a better understanding of the nexus between GSC integration and labour market outcomes in South-East Asia. It identifies several policy options that can increase resilience to shocks and ensure GSC integration leads to more inclusive, sustainable and resilient outcomes. 11

The purpose of this paper is threefold. First, it assesses trends and patterns in the number of GSC-jobs located in South-East Asia, offering new estimates and analyzing how these jobs have shifted between 2000 and 2021 by sector and country (also looking at these trends during the COVID-19 pandemic). To get a better idea of the diversity of the types of jobs and workers employed in GSCs, the paper presents jobs disaggregated by sex, age group, employment status and occupational skill level. Second, the paper presents results of an econometric analysis which investigates the empirical relationship between forward and backward GSC participation on one hand, and a range of labour market indicators on the other, relative to countries outside South-East Asia. Labour market indicators include working poverty, labour productivity, and the shares of wage employment, high-skill employment and female employment to total employment.12 Third, the paper identifies and discusses policies that increase resilience and support inclusive, sustainable and job-rich outcomes for women and men from participation in GSCs, during the pandemic recovery and beyond.

The paper is organized as follows. Chapter 1 provides a detailed picture of the jobs in South-East Asia linked to GSCs, presenting and discussing new estimates and trends. Chapter 2 discusses the results of an empirical analysis, investigating the links between GSC integration and South-East Asia’s labour market. The final chapter concludes by providing some policy considerations moving forward.

How many workers in South-East Asia have jobs linked to GSCs?

To understand the role GSCs play in creating jobs in South-East Asia, this chapter presents new estimates of the number of jobs provided by GSCs located in South-East Asia using data available for 2000 and 2007–2021. The analysis shows that, in 2021, 75 million workers—or around one in four workers—had a job linked to GSCs, with large differences between countries and sectors. Also, the share of workers in GSCs has been increasing over time, despite some short periods of sharp volatility and setbacks—such as during the first year of the COVID-19 pandemic in 2020. In addition, women, the youth, wage workers and low- or medium-skilled workers are part of the GSC-linked workforce, and are generally particularly well-represented in sectors highly integrated in GSCs.

The estimation methodology builds on ILO (2015) and Kizu, Kühn and Viegelahn (2019), combining data from international input-output tables with detailed data on employment by sector (Annex A).13 The methodology estimates the number of jobs in a particular country and sector that are dependent on the production of goods and services that—either as an intermediate input or final good—cross borders at least once before reaching the final consumer. The estimates consider both direct and indirect GSC linkages between countries and sectors (Box 2). Estimates of the number of GSC jobs are available for 62 countries, accounting for more than 75 per cent of the global workforce. The estimates include nine South-East Asian countries—Brunei Darussalam, Cambodia, the Lao People’s Democratic Republic (Lao PDR), Malaysia, Indonesia, the Philippines, Singapore, Thailand and Viet Nam—which collectively cover nearly 93 per cent of South-East Asia’s workforce. Estimates for Myanmar and Timor-Leste are not available.

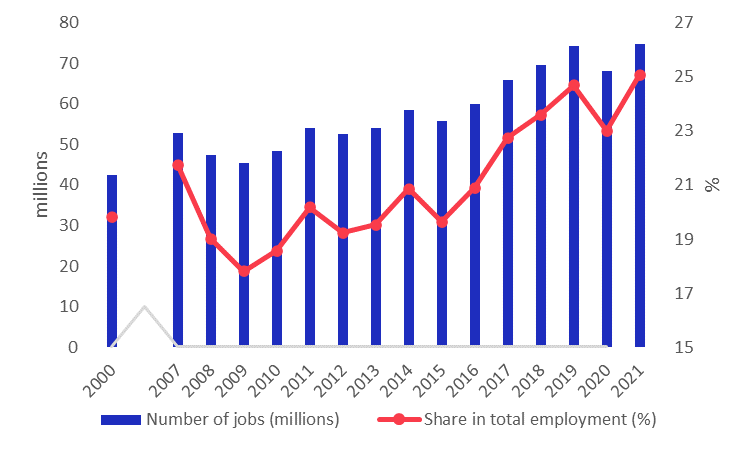

Using this methodology, 75 million workers in South-East Asia had GSC-related jobs in 2021, accounting for more than 25 per cent of total employment (Figure 1). This was nearly 7 million jobs more than in 2020, bringing the number of jobs linked to GSCs above 2019 pre-pandemic levels—compensating for the more than 4 million jobs not linked to GSCs that were lost in 2021. The share of GSC-linked jobs to total employment rose by more than 2 percentage points between 2020 and 2021. Given the harmful impact the pandemic had on the South-East Asian labour markets in 2021, GSCs helped enhance the recovery in South-East Asia.

In 2015–2019, the number of GSC-related jobs grew by 19 million, its share increasing by more than 5 percentage points. In 2019, both the number of GSC workers and their share of total employment peaked, driven to a large extent by the trade conflict between the United States (US) and the People’s Republic of China (PRC) and subsequent relocation of some production and jobs to South-East Asia.14 In 2020, the COVID-19 pandemic disrupted the rising trend in the number and share of GSC-related jobs in South-East Asia.15 Especially during the initial months of the pandemic, the sharp fall in global consumer demand hurt GSC-related jobs in the region.16 Workplace closures inside and outside South-East Asia disrupted production and in many cases prevented the normal supply of inputs within and across borders, thereby affecting related jobs.17

Box 2: Which Jobs Are Linked to Global Supply Chains?

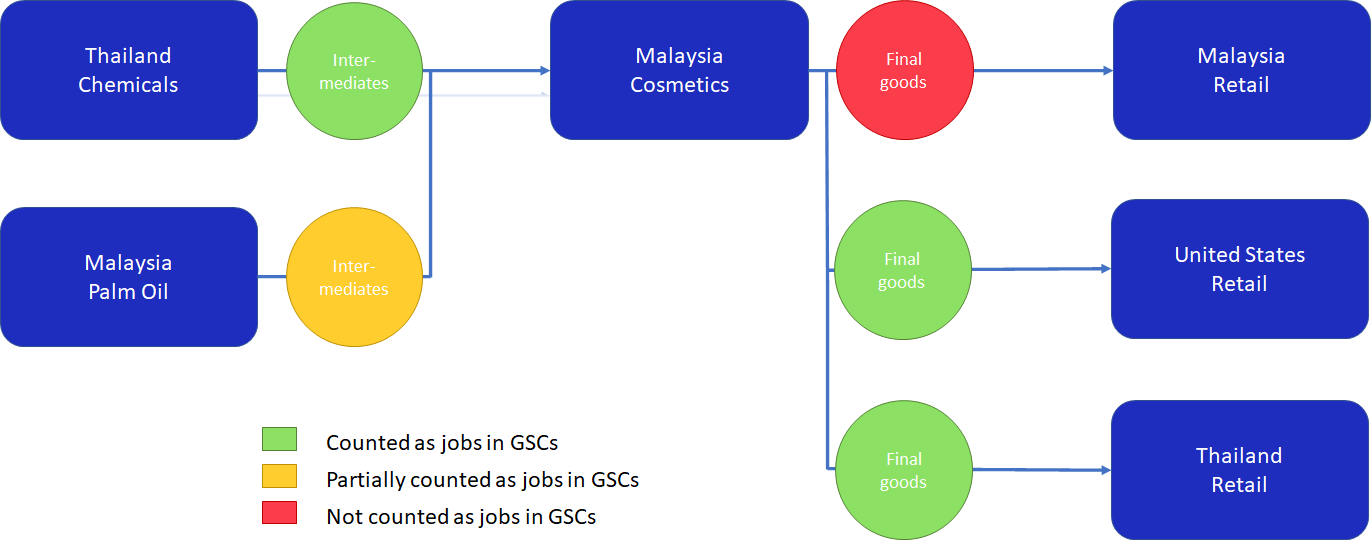

Jobs in global supply chains (GSCs) include both those with direct and indirect GSC linkages (see Annex A). For example, workers employed by a cosmetics manufacturer in Malaysia which sells cosmetics to the United States or Thailand would be counted in the estimate, as they produce final goods that cross borders at least once (Figure B2.1). Similarly, jobs in the Thai chemicals industry, related to the production of chemicals that are used as intermediate inputs and further processed in Malaysia by the cosmetics manufacturer, would also count as jobs in GSCs, regardless of whether the final cosmetics product is sold in Malaysia, the United States (US) or Thailand; this is because these inputs cross the border from Thailand into Malaysia. Finally, also those jobs in the Malaysian palm oil sector which produce palm oil that ends up as an input for cosmetics sold in the US or Thailand would be counted as jobs in GSCs; the palm oil—after being processed into a cosmetics product within Malaysia—in this case ends up crossing the border into the US and Thailand in order to reach the final consumer.

Figure B2.1: Jobs in GSCs—Illustrating the Methodology

Note: The circles represent the jobs linked to the production of intermediates or final goods in the given supply chain, which are located in the country and sector specified in the blue box to the left.

GSC jobs are not limited to manufacturing. They include jobs in manufacturing, agriculture, services and the non-manufacturing industrial sector. For example, cotton, palm oil or food are agricultural products that require labour before entering GSCs. Rare earth elements are examples of mining products that enter GSCs, thus some mining jobs are counted as GSC jobs. Tourism-related services are exported, thereby a part of GSCs. The common denominator is that they are either directly exported—as a final or intermediate for further processing—or they enter as an intermediate input into domestically produced goods or services that end up being exported. Using the methodology used here, all jobs related to these activities are counted as GSC jobs.

To estimate the number of jobs in GSCs, an assumption is made on labour productivity in GSC-related and non-GSC-related economic activities. Earlier International Labour Organization (ILO) estimates and those of other institutions assume equal labour productivity, regardless of whether the economic activity within a sector is related to GSCs or not.18 However, the literature shows that total factor productivity and labour productivity is typically higher in GSC-related activities than those not related to GSCs in a particular sector. For example, enterprises that contribute to GSCs through exports are more productive than non-exporting enterprises.19 As these differences are particularly stark in agriculture, the methodology makes some assumptions on productivity differentials in agriculture (see Annex A).

Figure 1: Number and Share of Jobs in Global Supply Chains, South-East Asia

Source: ILO estimates.

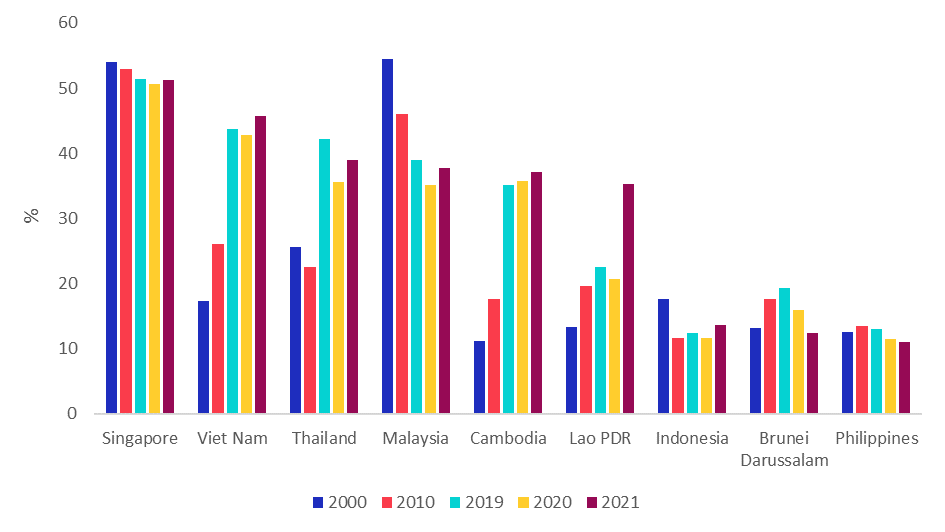

There are major differences in the number of GSC jobs in each country (Figure 2). Countries that rapidly increased their share of GSC jobs over the past decades include Viet Nam, Thailand, Cambodia and Lao PDR. In particular, Lao PDR and Cambodia saw their share of agricultural jobs linked to GSCs expand, with a growing portion of domestic value-added contributing to agricultural supply chains.20 The expansion in Viet Nam was driven by garment manufacturers producing for global brands, as well as by the foreign direct investments in electronics and semiconductors that helped create new jobs. The Philippines and Indonesia have relatively small shares of GSC jobs, largely due to the vast size of their domestic markets and demand which favors domestic trade over external trade.

Figure 2: Share of Jobs Associated with Global Supply Chains by Economy, South-East Asia

Note: Countries are sorted from the highest to the lowest share of GSC jobs in total employment in 2021.

Source: ILO estimates.

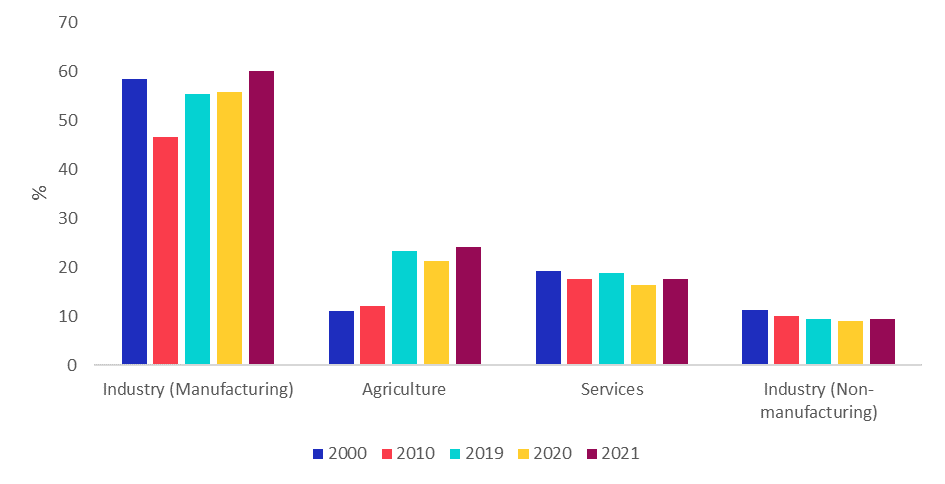

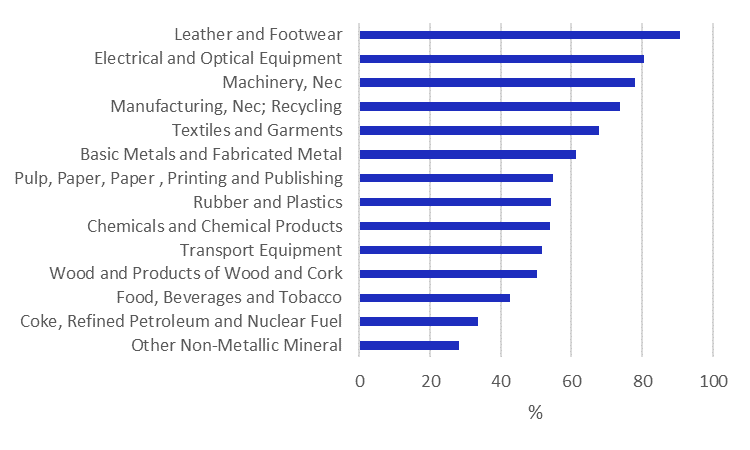

Manufacturing holds the highest share of jobs in South-East Asia’s GSCs. In 2021, more than 60 per cent of manufacturing employment was linked to GSCs, a substantial increase over 2020—emphasizing the strong role GSCs in manufacturing play in helping the labour market recover (Figure 3). Within manufacturing, the highest share of GSC-related jobs was in leather and footwear, followed by electrical and optical equipment and machinery. Production in these sectors is organized through highly complex GSCs, with inputs processed and shipped across borders multiple times to produce the final output. Some segments of the agricultural sector in South-East Asia also link to GSCs, with 24 per cent of all agricultural employment linked to GSCs in 2021. Over the past decade, agriculture has played an increasingly important role in GSC integration, doubling the share of agricultural jobs in GSCs since 2010. Also, in 2021, nearly 18 per cent of jobs in services were GSC-related, with tourism an important contributor. More than 9 per cent of other non-manufacturing industrial sector jobs—including mining, construction and utilities—were linked to GSCs.

Figure 3: Share of Jobs Associated with Global Supply Chains by Sector, South-East Asia

Panel A: By Broad Sector, 2021

Panel B: By Manufacturing Sub-sector, 2021

Source: ILO estimates.

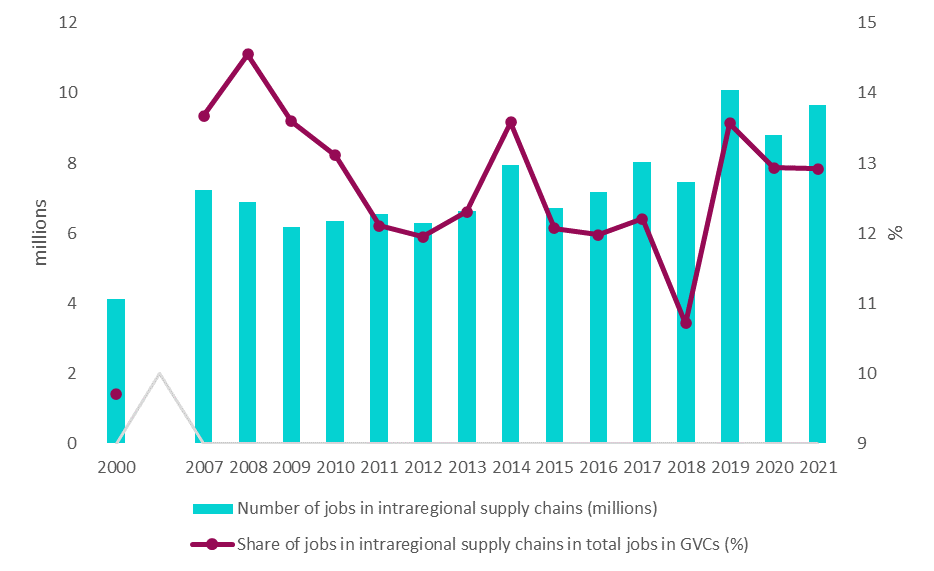

Only about 10 million jobs, or 13 per cent of total GSC jobs, were linked to intraregional GSCs (Figure 4). These jobs include those linked to final goods exports for consumption within South-East Asia, as well as jobs linked to intermediate goods exports for further processing in South-East Asia. This relatively low number shows the large potential for South-East Asia to enhance intraregional integration, as well as the important role played by the region as a supplier to countries outside South-East Asia. The share of GSC jobs linked to intraregional GSCs increased significantly from 2000 to 2007 but has stagnated since.

Figure 4: Number and Share of Jobs Associated with Intraregional Supply Chains, South-East Asia

Notes: Jobs in intraregional supply chains include those linked to final goods exports for consumption within South-East Asia, as well as jobs linked to intermediate goods exports for further processing in South-East Asia

Source: ILO estimates.

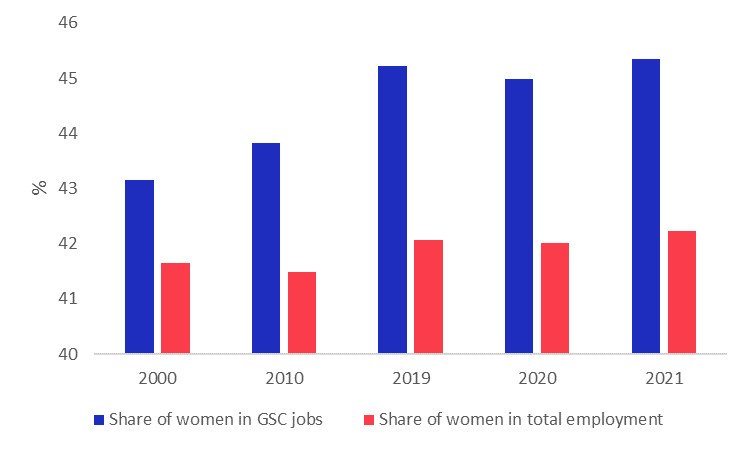

GSCs provide jobs for millions of women across South-East Asia. In 2021, about 34 million women worked in GSCs, accounting for 45 per cent of all GSC jobs, which is slightly higher than the share of women in total employment in South-East Asia (42 per cent) (Figure 5). In 2000, 18 million women worked in GSCs. As the estimates assume that the share of women in non-GSC and GSC activities within a sector are identical, differences arise from a composition effect, as sectors more integrated in GSCs on average employ more women—garment and electronics are two prominent examples (Box 3). In general, trade helps foster gender equality and better working conditions for women under certain circumstances.21 However, while GSCs have undoubtedly offered opportunities for more women to find jobs, many are still found in sectors that tend to require lower skills and offer lower pay (see chapter 3).

Figure 5: Share of Women Employed in GSCs, South-East Asia

Source: ILO estimates.

Box 3: Women in Sectors Highly Integrated in Global Supply Chains

Garment and electronics are particularly important entry points for integrating into global supply chains (GSCs) for some South-East Asian countries. They have also created important opportunities for women, including young women, to join the labour market.

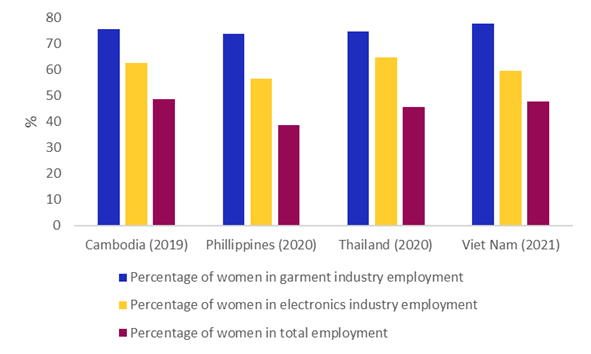

Women in Indonesia, the Philippines and Thailand took advantage of this some decades ago—at earlier stages of development—while female employment in garments has fallen or remained stable more recently. By contrast, women in less developed economies in the region have only found work in these sectors in recent years.22 In Cambodia, female employment in the garment industry tripled in a decade, rising from 256,000 in 2007 to 831,000 in 2017, with women accounting for 80 per cent.23 Similarly, in Viet Nam, female garment workers more than doubled between 2007 and 2020, rising from 1.6 million to 3.4 million, with women accounting for almost 75 per cent of all workers. In Myanmar, female employment in garments almost doubled over 4 years, rising from 612,100 in 2015 to 1.0 million in 2019, accounting for more than 85 per cent of garment workers.

Similarly, electronics GSCs in South-East Asia also played an important role in absorbing women labour, with the share of women in electronics higher than the female share of total employment in Cambodia, the Philippines, Thailand and Viet Nam (Figure B3.1). While the number of women working in sectors such as electronics or garments expanded sharply over the past decades in some countries, it is important to stress that—at least in some of these sectors—female jobs are disproportionately low-wage and lower skilled.24

Figure B3.1: Female Employment in Garments, Electronics and Overall in Selected South-East Economies

Source: ILO calculations based on ILO, ILOSTAT database

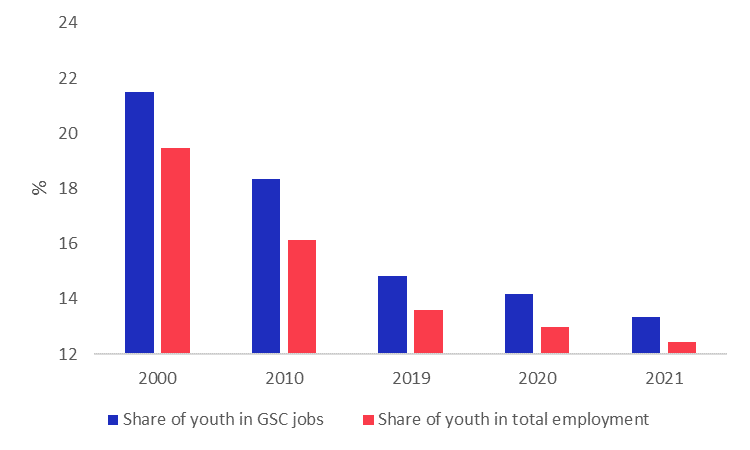

Sectors that integrate into GSCs offer a disproportionately large number of jobs to youth, indicating the importance of GSCs in providing labour market opportunities for young people (Figure 6). However, the share of youth in GSC-related jobs, as well as their share in total employment, has decreased over time as more young people spend more years in education and training. In 2021, about 10 million young workers in South-East Asia were estimated to have jobs linked to GSCs, accounting for 13 per cent of all GSC employment. These estimates by age group assume that the share of young workers in non-GSC and GSC activities within a sector are identical.

Figure 6: Share of Youth Workers Employed in GSCs and the Total Economy, South-East Asia

Source: ILO estimates.

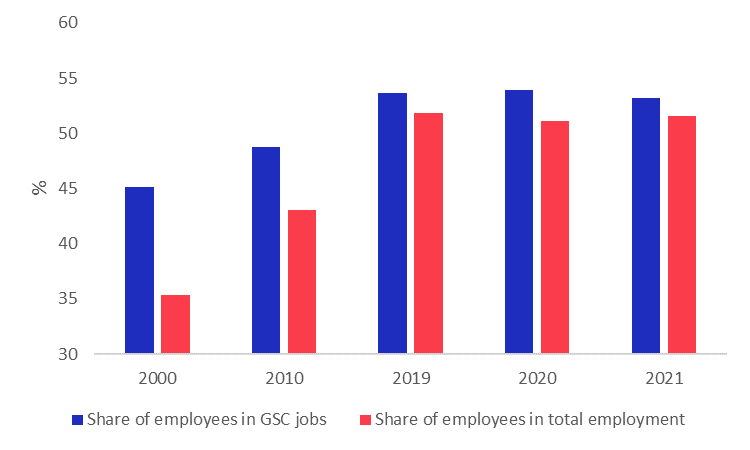

GSCs offer jobs for employees as well as the self-employed. In South-East Asia, the share of employees among GSC jobs has been consistently higher than their share in total employment, but the difference in shares has been declining (Figure 7). In 2021, 53 per cent GSC jobs were held by employees. Over time, the share of employees has been going up, reflecting rising development levels—self-employment and contributing family work are less and less important. These estimates by employment status assume that the shares of employees in non-GSC and GSC activities within a sector are identical, which in turn implies that differences are entirely driven by a sectoral composition effect, as those sectors that do show higher GSC integration on average employ a higher share of employees.

Figure 7: Share of Employees Employed in GSCs and in the Total Economy, South-East Asia

Source: ILO estimates.

Figure 8: Share of Workers in High-skill Occupations Employed in GSCs and in the Total Economy, South-East Asia

Source: ILO estimates.

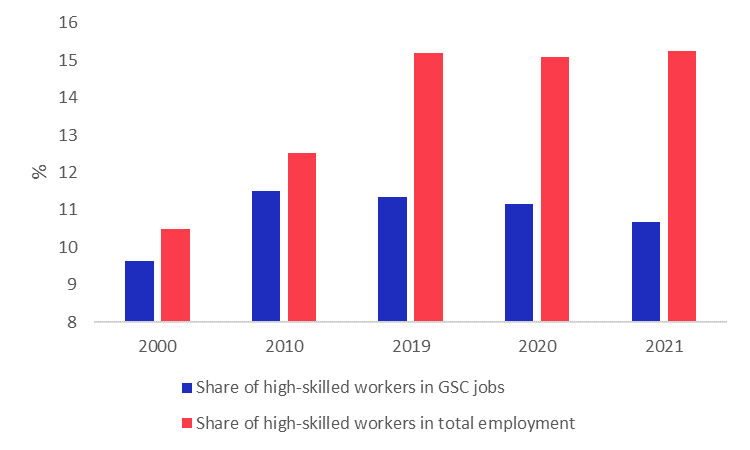

Employment can also be classified by skill level, where high-skilled employment includes managers, professionals, along with technicians and associate professionals—following the International Standard Classification of Occupations (ISCO). In 2021, 11 per cent of those in high-skill occupations were in GSCs, compared to a 15 per cent share of high-skill occupations to total employment (Figure 8). The share in high-skill occupations has consistently been lower in GSC-related jobs than in total employment. This indicates that GSCs in South-East Asia continue to create jobs mostly in low- and medium-skill occupations. For example, most workers in garments or electronics are medium-skilled, working as plant and machine operators.

How is backward and forward participation linked to jobs in South-East Asia?

A. Impact on the labour market: A literature review

This section describes empirical relationships based on regression analyses examining the association between forward and backward GSC participation with South-East Asian labour markets after controlling for a variety of factors. Forward GSC participation refers to a country’s or a sector’s participation in GSCs as a supplier of inputs to other countries, while backward GSC participation refers to the participation in GSCs as a foreign input user.

One important motivation for policy makers to help enterprises join GSCs is to create more and better jobs. Deeper GSC participation is indeed linked to employment and higher income for some workers and enhanced working conditions overall. 25 This is critical as better employment conditions, higher productivity and more pay are fundamental to raising living standards sustainably. Also, more GSC participation in labour-intensive industries can help create employment opportunities and overcome barriers to decent work for certain groups, such as women.26 Evidence shows that increased GSC linkages have helped expand paid wage employment of women in formal firms. 27 Still, GSC participation does not automatically mean there is gender equality. Persistent inequalities in GSCs, for example, are evident through gender segregation both across and within sectors, lower pay for women compared to men and a higher concentration of women in lower skilled and lower value-added GSC segments. 28

The employment and labour market effects of GSC integration vary widely across countries, depending on factors such as the type of sector and position within the GSC, strategies used by lead firms, the domestic skills base and institutional environment. 29 Through backward GSC participation, for example, the positive employment and wage effects have been biased towards more skilled workers in developing countries, although less than in high-income economies. 30 This could be a factor in aggravating wage inequality. 31 The sizeable barriers to GSC participation can also exacerbate inequality, particularly given the constraints faced by smaller firms. 32

There are myriad ways deeper GSC integration affects jobs with spill over to the labour market. For instance, backward GSC participation suggests that enterprises use and benefit from foreign inputs. This gives companies better access to a wider choice of higher quality inputs with better technology. This can have positive effects through learning and knowledge transfer as access to information and open markets improves and technology and expertise flows between buyers and sellers across the supply chain. 33 Firms can become more competitive and profitable, which strengthens the factors that lead to better working conditions. Also, in some cases, deeper GSC involvement can contribute to a higher skilled workforce. Deeper forward GSC linkages can attract investments in training from GSC-linked firms—helping increase overall skill levels in the labour market—to meet the higher product standards and service quality buyers require.34 On the other hand, having a skilled workforce supported by strong, responsive education and training is often a precondition for successful GSC participation. 35

GSC linkages can spur growth in aggregate productivity through different mechanisms. Investments in forward GSC segments that export final products or produce inputs for further upstream processing can speed structural transformation and the shift into higher value-added, relatively less labour-intensive and more productive GSC sectors. In numerous South-East Asian economies, for example, rising labour productivity has been linked to the shift in labour demand from agricultural production for domestic consumption toward textile and garment manufacturing for external markets. 36 Enhanced productivity can also come from deepening GSC integration as core tasks are specialized. This helps firms (i) become more efficient; (ii) find new ways to acquire higher-technology foreign inputs; (iii) absorb knowledge from innovative GSC-linked firms; and (iv) provide incentives for upscaling that results in higher productivity. 37 However, this can also lead to job losses as labour-saving technologies can help meet the quality standards required by upstream markets. 38

Deeper GSC participation, given its positive impact on productivity, has been associated with a reduction in poverty in some cases, especially where GSC-linked firms provide wages to attract economically inactive women and men into the labour market—or appeal to workers from lower-paid sectors. This can happen through several indirect channels: productivity gains in supplier industries can generate sharp labour demand because of input-output linkages; productivity growth can stimulate final demand; and associated structural shifts in the economy could expand labour-intensive sectors. 39 For the rural poor, agriculture supply chains in principle can reduce poverty by integrating smallholder farmers and rural households to supply chains, expanding their access to domestic and international markets and inducing a shift to higher-value agricultural exports. 40 Empirical evidence, however, points to a different reality in many cases. Smallholder farmers in developing countries typically face insurmountable barriers—including higher agricultural product standards, limited technical and financial capacity and gaps in monitoring and compliance, among others—that prevent linking to forward GSCs, thus slowing the reduction in working poverty. 41

Enhanced GSC participation can theoretically lead to better working conditions from both gains in productivity, wages and skills and through improved governance—as governments and GSC-linked firms strive to ensure compliance with buyer standards. Oftentimes driven by pressure from international consumers concerned about worker welfare, there is increasing concern over labour standards, fair wages, employment conditions, and workplace safety and health, although in many cases compliance remains limited to larger first-tier suppliers. 42, 43 Nevertheless, evidence points to the prevalence of informality and poor working conditions in GSCs, especially in small-scale enterprises and subcontractors in lower-tier segments. 44 Related to this, there is also persistent child labour and forced labour in GSCs, which can be traced back to the interaction of three critical dimensions. 45 These include (i) gaps in statutory legislation, enforcement and systems of justice that allow non-compliance; (ii) poverty and other socio-economic pressures faced by individuals and workers; and (iii) a lack of awareness, capacity and policies on the part of businesses of their responsibility to uphold fundamental principles and labour rights.

While strengthening labour provisions in bilateral and regional trade agreements can have positive impacts (see also section IV), empirical evidence remains limited, given the longer-term nature of the expected impacts. 46 Nonetheless, there are concrete results in terms of ratifying international labour standards. For example, in 2020, Viet Nam ratified the ILO Convention 105 on the Abolition of Forced Labour to conclude the European Union (EU)-Viet Nam free trade agreement (FTA), which required Viet Nam to continue working toward ratifying all fundamental conventions—Viet Nam has ratified 9 of the 10 fundamental conventions, the exception being ILO Convention 87 on the Freedom of Association and Protection of the Right to Organize. 47

B. The link between backward and forward participation in global supply chains and jobs in South-East Asia

This section discusses the labour market implications of deeper GSC integration, based on the econometric analysis by Blanas, Huynh and Viegelahn (forthcoming), which covers 62 economies and 35 industries (Annex B). 48 It includes detailed findings for nine South-East Asian economies—Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia, Philippines, Singapore, Thailand, and Viet Nam—for 2000 and 2007–2020. It provides empirical evidence from novel econometric analysis of different measures of GSC participation from ADB’s Multi-Regional Input-Output Tables as well as real and estimated labour market data from the ILO’s global repository of harmonized household survey microdata.

The econometric analysis gives some insights into the link between deeper GSC involvement in South-East Asia and jobs over the past two decades. First, improvements in employment quality—approximated specifically by reductions in working poverty and increases in labour productivity—were positively associated with increased backward and forward GSC participation. Second, the results show that, on the contrary, enhanced GSC participation was not universally linked to other important dimensions of better job quality, such as higher shares in wage employment and high-skilled employment. Greater forward GSC engagement in South-East Asia was tied to a lower wage employment share overall—notwithstanding higher wage employment shares in manufacturing—coming from the intense demand for self-employment in the agriculture-driven primary sector. Enhanced GSC participation was also linked to greater demand for low- and medium-skill employment at the expense of high-skill jobs. Third, greater backward GSC integration was correlated with some employment gains for women. However, the benefits were concentrated in the primary sector and personal and professional services, both typically less skill-intensive, less productive and lower paid.

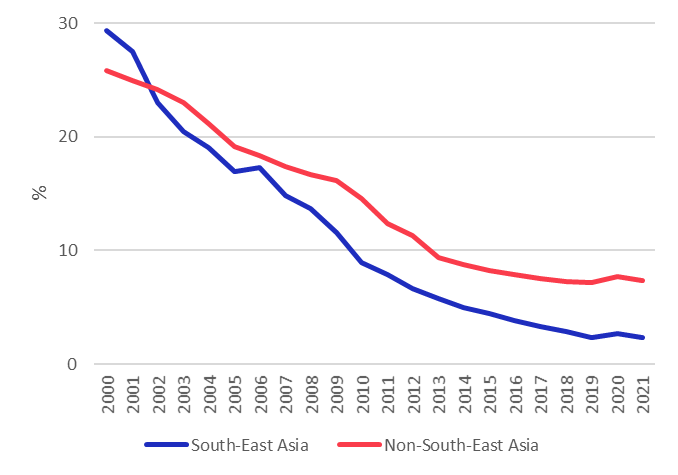

Figure 9: Working Poverty Rate in South-East Asia and Non-South-East Asia Countries, 2000–2021 (per cent)

Note: Working poverty is measured as the percentage of employed persons living in poverty, defined using the international poverty line of $1.90 per day in purchasing power parity.

Source: Authors’ calculations based on ILO, ILOSTAT Database.

GSC participation has intensified in South-East Asia over the past couple of decades. During this period, the region made progress in the labour market by expanding productive employment and enhancing job quality. The share of workers living in extreme poverty decreased considerably from 29 per cent in 2000 to just above 2 per cent in 2021 (Figure 9). The 27 percentage point drop far outpaced progress in the world excluding South-East Asia, where it declined by 18 percentage points since 2000. The reduction occurred across segments of the labour market, including women and young workers. Similarly, the region made remarkable strides in boosting labour productivity—critical for a sustained increase in wages and labour income—as a structural transformation led workers into higher value-added sectors. Between 2000 and 2021, labour productivity—measured as output per worker—increased by an annual average of 3 per cent in South-East Asia. By comparison, labour productivity globally grew by 2.1 per cent annually during the same period. 49

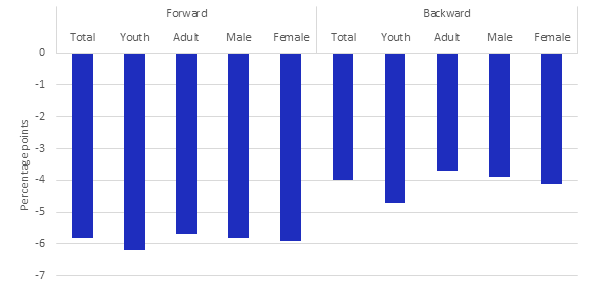

The better labour market coincided with deeper GSC participation over the past two decades. In many cases, they may be linked. First, the expansion of backward GSC participation by one standard deviation can be associated with a decline in the total working poverty rate of 4 percentage points, using data for 2000 and 2007–2019 (Figure 10). Similarly, the expansion of forward GSC participation is associated with a decline in the total working poverty rate by 5.8 percentage points. While the result on backward GSC participation is not significantly different from the result for countries outside South-East Asia, the result on forward GSC participation is specific to South-East Asia and not found in countries outside the region. Importantly, the robust, inverse relationship also holds for the fall in working poverty across sub-groups—male and female workers and working youth and adults—and by comparable magnitude.

Figure 10: Estimated Change in Working Poverty Associated with an Increase of One Standard Deviation in Backward and Forward GSC Participation in South-East Asia by Age and Sex (percentage points)

Note: All estimates are statistically significant at the 5 per cent level. Estimates are based on ordinary least squares (OLS) regressions at the country level, with country and year fixed effects. Working poverty is measured as the percentage of employed persons living in poverty, defined using the international poverty line of $1.90 per day in purchasing power parity. Youth are defined as those aged 15-24 years and adults aged 25+ years. Regression results are based on a sample that includes 2000 and 2007–2020.

Source: Authors’ calculations based on Blanas, Huynh and Viegelahn (forthcoming).

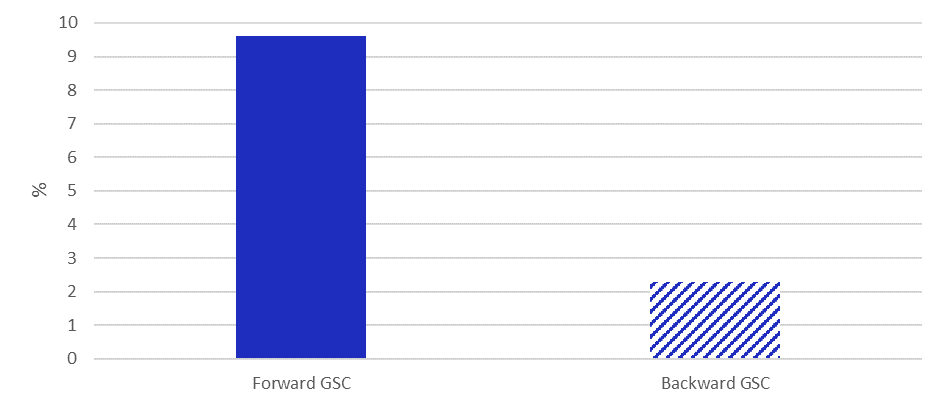

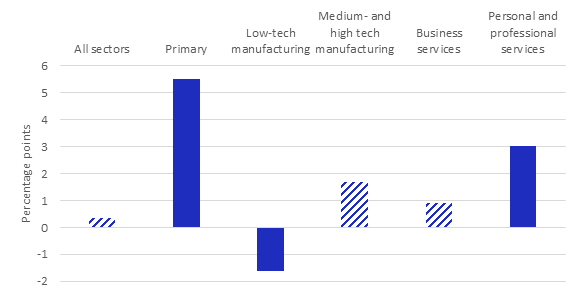

The link between GSC participation and increased labour productivity has also been quite stark, and—based on the results of Blanas et al. (forthcoming) –significantly more than countries outside the region under analysis. The level of labour productivity is positively associated with forward GSC participation in the South-East Asian countries (Figure 11). An increase in forward GSC participation by one standard deviation is associated with an increase in real labour productivity of 9.6 per cent. Even though the overall link between backward GSC participation and real labour productivity is statistically not significant, countries in the region are still found to perform better than those countries under analysis outside South-East Asia when translating higher backward GSC participation into higher real labour productivity. These findings corroborate the literature on the beneficial link between GSCs and labour productivity and align with South-East Asia’s recent economic diversification, structural transformation and skills upgrading.

Another labour market trend in South-East Asia is the considerable progress made in expanding the portion of paid employees in total employment—a suggestive, although imperfect, measure of job security and stability. From 2000 to 2021, the wage employment share grew from 34 per cent to 50.1 per cent—or by 16.2 percentage points, nearly double the rate for the rest of the world (8.6 percentage points). 50 The region also recorded some moderate gains for employment in high-skill occupations—jobs as managers, professionals and associate professionals typically requiring higher qualifications, skills and experience. Between 2000 and 2020, the share of employment in high-skill occupations in the region increased by 4.6 percentage points, from 9.9 per cent to 14.5 per cent. Although this slightly outpaced progress in the rest of the world (4.2 percentage points), employment outside the region remained more reliant on high-skill employment overall (21.8 per cent in 2020). 51

Figure 11: Estimated Change in Labour Productivity Associated with an Increase of One Standard Deviation in Backward and Forward GSC Participation in South-East Asia (per cent)

Note: All estimates are statistically significant at the 5 per cent level. Estimates are based on OLS regressions at the country level, with country and year fixed effects. Labour productivity is defined as the log of the total volume of output (measured in terms of gross domestic product in constant prices) produced per employed persons. Regression results are based on a sample that includes 2000 and 2007–2020.

Source: Authors’ calculations based on Blanas, Huynh and Viegelahn (forthcoming).

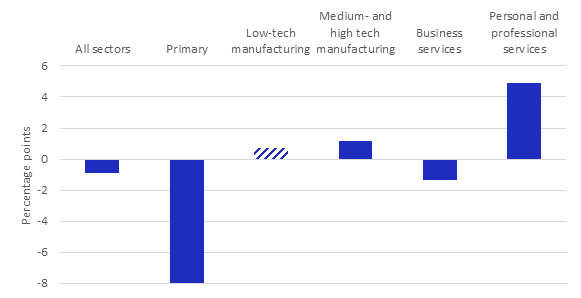

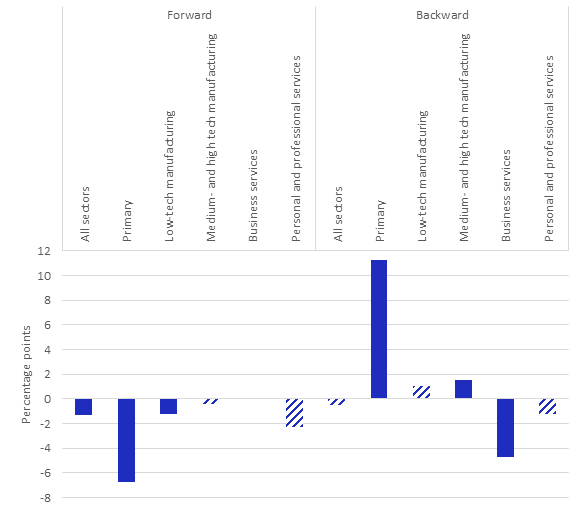

Figure 12: Estimated Change in Employment Shares Associated with an Increase of One Standard Deviation in GSC Participation in South-East Asia by Economic Sector (percentage points)

Panel A: Wage Employment, Forward GSC Participation

Panel B: Employment in High-Skill Occupations, Backward and Forward GSC Participation

Panel C: Female Employment, Backward GSC Participation

Note: Solid bars indicate that the estimate is statistically significant at the 10 per cent level. Diagonally striped bars indicate that the estimate is statistically not significantly different from zero. Estimates are based on country-industry OLS regressions with robust standard errors and country-industry and country-year fixed effects. Employment shares are constructed so that each dimension totals 1—(a) employment status: wage employment and self-employment; b) skill: high and low/medium; and (c) sex: male and female. Employment in high-skill occupations includes managers, professionals, technicians and associate professionals. See Annex for list of sub-sectors under broad sector headings. Regression results are based on a sample that includes 2000 and 2007–2020.

Source: Authors’ calculations based on Blanas, Huynh and Viegelahn (forthcoming).

For wage employment and high-skill employment growth, however, the region’s enhanced forward GSC participation, especially in certain sectors, may have actually slowed these trends. Deeper forward GSC engagement is associated with a quantitatively small decrease in the wage employment share, or conversely an increase in the share of self-employed workers (Figure 12.A). This finding is specific to South-East Asia, but the dynamic is heavily influenced by the agriculture-driven primary sector, where self-employed own-account workers and contributing family workers are prevalent, and to a lesser degree in business services, which includes considerable shares of self-employment in retail trade. By comparison, greater forward GSC participation in manufacturing as well as personal and professional services is associated with positive gains in the wage employment share, suggesting an expansion of opportunities for wage employment in these sectors.

Similarly, the results show a heterogeneous relationship between greater GSC participation and the share of employment in high-skill occupations based on economic sector (Figure 12.B). Greater forward GSC participation is associated with a lower share of employment in high-skill occupations overall. This pattern is specific to South-East Asia and driven by the primary sector (with a heavy concentration of low-skilled agricultural employment) and low-technology manufacturing such as garments (which is largely reliant on medium-skill employment of plant and machine operators). The relationship between backward GSC participation and the share of employment in high-skill occupations is statistically insignificant overall. However, business services are negatively associated with the share of workers in high-skill occupations; subsectors such as retail trade and hotel and restaurants are dominated by medium-skill occupations in clerical support, services and sales. Conversely, deeper backward GSC linkages in agriculture and medium- and high-technology manufacturing are both associated with robust gains in high-skill employment, which suggests increased demand for high-skilled workers. The increased use of foreign inputs in these sectors often require special skill requirements, which can only be met by increasing high-skill occupations such as professionals and technicians.

For women workers, the sectoral results also show that employment gains from backward GSC engagement are shaped by the primary sector and personal and professional services. An increase in backward GSC linkages is significantly associated with a positive expansion in the share of female employment, and particularly positive in South-East Asian economies when compared to other countries worldwide (Figure 12.C). Nevertheless, both sectors in general tend to be less skill-intensive and provide comparatively fewer productive jobs with lower remuneration, meaning that gains from deeper GSC participation for female employment in South-East Asia have been mixed. Increased GSC backward participation in low-tech manufacturing is associated with a lower female employment share; the increased sourcing of foreign inputs from other countries may in many cases make jobs currently held by women obsolete. 52 For example, an apparel factory might have previously produced textiles as an input for garment production using female labour—increased sourcing of textiles abroad would make some of those jobs obsolete.

The association of forward GSC participation and female employment shares is not statistically significant. While GSCs do create jobs for millions of women in the region, it appears that these jobs are created mainly because women are well-represented in more integrated GSC sectors (see chapter 1) and not because a sector increases its forward GSC participation over time. In other words, the garment industry is more integrated in GSCs than many other sectors and employs a high share of women. But if the garment industry further increases forward GSC participation, there appears to be no impact on female employment share.

Young women and men have increased their time in school and delayed joining the workforce, as seen in the declining employment share of youth generally. The proportion of youth in total employment in the region decreased from 21.2 per cent in 2000 to 13.5 per cent in 2021, a 7.8 percentage point contraction. 53 In the rest of the world, the decrease in the youth employment share was also significant, although slightly lower at 6.2 percentage points. The progressively lower (higher) share of jobs taken up by youth (adults) follows trends in GSC engagement. Deeper forward GSC participation in South-East Asia is associated with relatively greater adult employment. This likely shows the heightened demand for older workers with more experience and expertise in industries with more forward GSC engagement.

In sum, deeper GSC participation during the past two decades is linked to some positive gains in South-East Asia’s labour market—most notably the drop in working poverty and increase in labour productivity. However, some important benefits—expanding wage employment, high-skill employment and more and better jobs for women and youth—happened only in certain economic sectors. These results underline a critically important dynamic: the link between GSCs and the creation of higher-quality and more inclusive jobs is not automatic.

Conclusion and way forward

This paper analyzed GSCs and employment in South-East Asia over the past two decades. First, since 2000, the region as a whole has become increasingly dependent on GSCs for employment despite some short periods of volatility and setbacks. In 2021, an estimated 76 million workers had GSC-related jobs, or more than a quarter of total employment. Second, regional trends mask country- and sector-specific trends. Some countries—such as Singapore, Viet Nam and Thailand—were more dependent on GSC employment than others like Indonesia, Lao PDR or the Philippines. Manufacturing accounted for the largest share of GSC employment, while an increasing share of agricultural jobs were linked to GSCs. Third, increased GSC participation was associated with some important, albeit mixed, progress in improving job quality. While deeper GSC integration was associated with rapid declines in working poverty and to gains in labour productivity, the relationship between increased GSC participation and greater wage employment and high-skill employment was negative in several sectors, and positive in a few. Fourth, while GSCs provide millions of jobs for women—in sectors highly integrated into GSCs—some results indicate the employment gains were associated with enhanced GSC engagement only in sectors where jobs are typically less skill-intensive and lower paid. Finally, a review of the literature highlighted that deficits in decent work in GSCs persist.

In this context, policy makers must navigate through a complex landscape.54 Even prior to the COVID-19 pandemic, the confluence of technological change, growing economic nationalism and the need for sustainability was expected to reshape several GSCs trajectories—including reshoring, diversification, regionalization and replication.55 The pandemic—and the Russian invasion of Ukraine, which led to a variety of export restrictions—has further amplified questions over the future trajectory of GSCs in the region. What policies can contribute to inclusive, sustainable, and job-rich development from GSC participation during the recovery phase? What policies can help GSCs move up from low productivity to higher productive activities? To help navigate the way forward, several policy areas stand out as important for future policy making.

First, well-designed social protection and labour market policies are essential to cushion the shocks that GSCs propagate as well as dealing with distributional consequences. The number of workers engaged in GSCs continues to increase, and job dependence on GSCs makes them vulnerable to external shocks. Growth in GSC jobs has hardly been smooth, with both the 2008–2009 global financial crisis and the more recent COVID-19 pandemic leading to large fluctuations in the number and share of GSC workers across the region. It is also well understood that trade and GSC participation require structural transformation, which in turn requires workers to move across jobs and sectors. Social protection can provide worker support during these structural shifts and transitions. Unemployment insurance, for example, ensures income security and allows for smoothing household consumption. This allows jobseekers the time to find a new job that matches their skills, increasing labour market efficiency.56 In addition to these passive labour market policies that provide income replacement, active labour market policies (ALMPs) that facilitate the finding of jobs and the matching between workers and vacancies are important to support workers affected by shocks, and are particularly relevant for informal workers. These policies can also slow the transmission of external shocks from urban to rural areas when rural migrant workers face retrenchment.57 As GSCs are reshaped in response to the evolving “new normal”, workers, firms and labour markets will be affected.58 Social protection and labour market policies are critical not only to cushion any adverse impact from the transformation, but also in building a foundation that promotes innovation and risk-taking.59 This is critical in particular for upgrading to higher productivity segments within GSCs.

Despite considerable progress in strengthening social protection systems and ALMPs, particularly on the heels of the 1997–1998 Asian financial crisis and the global financial crisis, the majority of workers in South-East Asia do not have access to unemployment protection—with only a small portion with access to ALMPs.60 The COVID-19 pandemic also led countries to experiment with different policies that can be leveraged to further extend social protection and access to ALMPs. In the Philippines, for example, the COVID-19 Adjustment Measures Program (CAMP) provided a one-time cash transfer to affected workers of establishments with flexible working arrangements or had to suspend operations due to the pandemic.61 It was implemented together with the Tulong Panghanapbuhay sa Ating Disadvantaged/Displaced Workers (Tupad) Program, which offered community-based temporary employment to workers in the informal economy.

In Cambodia, a wage subsidy programme for garment workers with temporarily suspended contracts provided $70 per month for each worker, with $40 provided by the government and the remaining $30 by the employer.62 To protect informal workers, the government also expanded its cash transfer programme, providing monthly average payments of $30–$50 depending on household size and vulnerability. At the same time, a first-ever state-owned Credit Guarantee Corporation of Cambodia Plc (CGCC) was set up in 2020 to support micro, small, and medium-sized enterprises (MSMEs) access formal loans and stay afloat. More comprehensively, Indonesia recently introduced its first unemployment benefit package—the Job Loss Guarantee program (Jaminan Kehilangan Pekerjaan, or JKP), which in addition to cash transfers to the unemployed, provides access to labour market information and job training so affected workers can find new employment opportunities.63 The programme provides 45 per cent of monthly wages for the first 3 months and 25 per cent of wages for the subsequent 3 months. Regionally, the Association of Southeast Asian Nations (ASEAN) Comprehensive Recovery Framework (ACRF) secured a political commitment to expand social protection, including informal workers, protecting employment in pandemic-affected sectors, and preparing labour policies through social dialogue.64

For countries without a comprehensive social protection system and vulnerable to GSC trade shocks (for example Lao PDR and Cambodia), consideration could be given to pivoting one-time pandemic-related policies providing targeted assistance to those directly affected by trade. Several countries around the world, mostly advanced economies, have trade adjustment assistance programme. While there are certainly concerns whether those suffering from trade liberalization should be treated differently than those affected by other shocks, experience in the Republic of Korea and US indicate these programmes can be useful in fostering greater public support for trade reforms.65, 66 For less developed economies in the region, budgetary constraints will likely require financing though international cooperation, including aid for trade.

As mentioned earlier, there is growing evidence that the international fragmentation of production increases wage inequality in developing countries. One study finds that the share of value-added accruing to capital and higher skilled workers increased while the corresponding share declined for low skilled workers in developing countries between 1995 and 2008.67 There is also growing concern that further GSC automation and robotics—in addition to raising anxieties in developing countries that jobs will be re-shored or near-shored—will further exacerbate wage inequalities. Social transfers and employment policies need to address these inequalities.

Second, the heterogenous relationship between GSC participation and skills development suggests that investments in a broad range of skills are needed to move into higher value-added GSC segments. These are particularly important for women, who, as the results in this paper highlight, are concentrated in the primary sector and low-technology manufacturing. National development plans indeed place strong emphasis on skills development to apply upgraded technology; with skills roadmaps designed for specific sectors in some countries. Governments also promote vocational education for skilling, reskilling and upskilling. Overall, countries tend to focus on the development of high-skilled human resources to bring the country to the technological frontier of Industry 4.0 and the digital economy. While this is important, it is equally critical to recognize that the future of work is not just high-skilled. Skills development policies and programme often focus on the highly educated or high-skilled workers—at the expense of the large number of workers in low- or medium-skilled occupations. Some national development plans are unrealistic and overly simplified, given the difficulty of predicting the skills required for the future. Reskilling has its limitations. For example, garment workers will not easily transform themselves into data scientists.68 Well-designed and realistic skills development policies and programmes as part of a human-centered pandemic recovery will help South-East Asian countries move into higher GSC segments.69

A few countries in the region also have policies and programmes that form and deepen linkages between domestic MSMEs and foreign investors, in part to encourage skill diffusion. These programmes exist in Singapore, Malaysia and Thailand—other ASEAN countries lack these programmes or they are not well-funded.70 Singapore’s Pioneer Certificate incentive and Development and Expansion Incentive programmes provide tax incentives to foreign investors that introduce more advanced technology, skills and knowledge or that carry out new or pioneering activities.71 In Thailand, tax incentives are provided to investors doing research and development and advanced technology training. Also, they apply to investors that donate to technology and personnel development funds, educational institutions and specialized training centers in science and technology.72 In designing tax incentives, however, while they can make investing more attractive, they cannot compensate for institutional or physical infrastructure shortcomings, including deficiencies in labour market institutions.73

Third, as the link between increased GSC participation and decent work is not automatic, as highlighted in the findings of this paper, deep trade agreements—which increasingly cover labour provisions—is one tool to strengthen the link. Labour provisions also provide an entry point for stakeholders, in particular social partners, to discuss issues related to decent jobs in GSCs.74

Trade agreements have evolved from simply targeting tariffs to covering a broad range of provisions, including those relating to intellectual property protection, anti-corruption and environmental and social issues – often termed as deep trade agreements. For example, trade agreements in the 1950s covered eight policy areas, whereas trade agreements recently average 15.75 As mentioned, trade agreements now increasingly cover labour, to ensure a certain minimum level of labour standards. More specifically, these can be defined as “(i) any principle or standard (including international labour standards) or rule, which addresses labour relations, minimum working conditions, terms of employment, and/or other labour issues; (ii) any framework to promote compliance with standards through cooperative activities, dialogue and/or monitoring of labour issues; and/or (iii) any mechanism to ensure compliance with standards, either set under national law or in the trade agreement”.76 With a safe and healthy working environment now recognized as a fundamental principle and right at work, trade provisions, which amongst labour issues tend to reference fundamental principles and rights at work the most, this area will likely become increasingly standard within trade agreements. For garment factories that had questionable occupational safety and heathy records, this could help countries in the region ensure a safer and healthier work environment.77

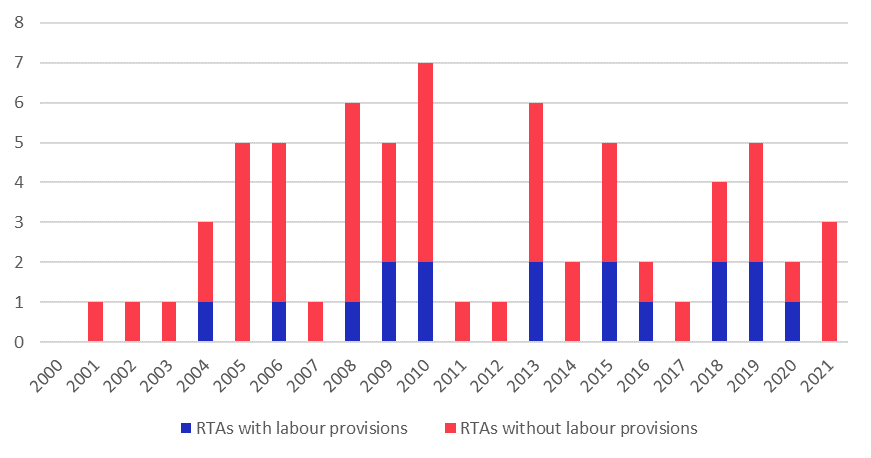

Around half of trade agreements concluded worldwide between 2011 and 2020 contained labour provisions, compared to around a quarter between 2001 and 2010. At the same time the content of more recent labour provisions has become more comprehensive, including in content, application and enforceability.78 Longer-term trends in South-East Asia (Figure 3.13) are less clear. But in the years leading up to the COVID-19 pandemic, labour provisions appeared in almost half of concluded FTAs. These include the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP)—with Brunei Darussalam, Malaysia, Singapore, and Viet Nam as members—which contains provisions on cooperation for job creation and productive, quality employment. Other recent agreements with labour provisions include the EU-Viet Nam FTA (2020); the Chile-Indonesia Comprehensive Economic Partnership Agreement (CEPA) (2019); the EU-Singapore FTA (2019); the agreement between the Philippines and the European Free Trade Association (EFTA) States (2018).

Figure 13: Number of Regional Trade Agreements (RTAs) Involving At Least One South-East Asian Country

Source: Authors’ calculations based on ILO. 2022. ILO Labour Provisions in Trade Agreements Hub (LP Hub).

A growing body of literature finds that deep trade agreements have a positive effect on trade and welfare, beyond that provided by shallow trade agreements.79 In Cambodia, the gender pay gap in garments is estimated to have been reduced from 32 per cent prior to the Cambodia–US Bilateral Textile Agreement, which included labour provisions, to 6 per cent after implementation. By comparison, the gender wage gap in other manufacturing sectors remained unchanged.80 Labour provisions in trade agreements neither appreciably divert nor decrease trade flows. Taken together, the findings suggest opportunities for countries in the region to benefit from increasingly deeper FTAs with labour provisions, while at the same time using them to engage with social partners and other stakeholders on more elusive benefits, including growth in higher skilled jobs and wage employment.

References

Aho, C. Michael, and Thomas O. Bayard. 1984. “Cost and Benefits of Trade Adjustment Assistance”. In The Structure and Evolution of Recent U.S. Trade Policy, edited by Robert E. Baldwin and Anne O. Krueger, 153–194. Chicago: University of Chicago Press.

Aked, Jody. 2021, “Supply Chains, the Informal Economy, and the Worst Forms of Child Labour”, CLARISSA (Child Labour Action Research Innovation in South & South-Eastern Asia) Working Paper No. 8. Brighton: Institute of Development Studies.

Anukoonwattaka, Witada, Pedro Romao, and Richard S. Lobo. 2020. “If the US-China Trade War is Here to Stay, What are the Risks and Opportunities for Other GVC Economies Outside the War Zone?”, ARTNeT Working Paper Series No. 209. UNESCAP (United Nations Economic and Social Commission for Asia and the Pacific).

ASEAN-Japan Centre. 2019. “Global Value Chains in ASEAN: Cambodia”, Paper No. 3.

———. 2021. “Global Value Chains in ASEAN: Lao People’s Democratic Republic”, Paper No. 5.

ADB (Asian Development Bank). 2021. COVID-19 and Labor Markets in Southeast Asia: Impacts on Indonesia, Malaysia, the Philippines, Thailand and Viet Nam.

ADB. 2023. ASEAN and Global Value Chains: Locking In Resilience and Sustainability.

ADB and ILO (International Labour Organization). 2014. ASEAN Community 2015: Managing Integration for Better Jobs and Shared Prosperity.

Bárcia de Mattos, Fernanda, Sukti Dasgupta, Xiao Jiang, David Kucera, and Ansel F. Schiavone. 2020. Robotics and Reshoring: Employment Implications for Developing Countries. Geneva: ILO.

Blanas, Sotiris, Phu Huynh, and Christian Viegelahn. Forthcoming. “Is Deeper Global Value Chain Integration Linked to More Inclusive Labour Markets in South-East Asia? A Global Comparative Analysis”, ILO Working Paper.

Caspersz, Donella, Holly Cullen, Matthew C. Davis, Deepti Jog, Fiona McGaughey, Divya Singhal, Mark Sumner, and Hinrich Voss. 2022. “Modern Slavery in Global Value Chains: A Global Factory and Governance Perspective.” Journal of Industrial Relations 6 (2): 177–199.

Choi, Paul Moon Sub, Kee Beom Kim, and Jinyoung Seo. 2019. “Did Capital Replace Labor? New Evidence From Offshoring.” The B.E. Journal of Macroeconomics 19 (1): 1–22.

Corley-Coulibaly, Marva, Ira Postolachi, and Netsanet Tesfay. 2022. A Multi-faceted Typology of Labour Provisions in Trade Agreements: Overview, Methodology and Trends. Geneva: ILO.

Criscuolo, Chiara, Jonathan Timmis, and Nicholas Johnstone. 2015. “The Relationship Between GVCs and Productivity”, Background Paper. Paris: OECD.

Dasgupta, Sukti, Tuomo Poutiainen, and David Williams. 2011. From Downturn to Recovery: Cambodia’s Garment Sector in Transition. Bangkok: ILO.

Distelhorst, Greg, and Diana Fu. 2017. “Wages and Working Conditions in and out of Global Supply Chains: A Comparative Empirical Review”, ILO ACT/EMP Research Note.

Farole, Thomas. 2016. “Do Global Value Chains Create Jobs? Impacts of GVCs Depend on Lead Firms, Specialization, Skills, And Institutions”, IZA World of Labour No. 291.

Fernandes, Ana, Nadia Rocha, and Michele Ruta (eds). 2021. The Economics of Deep Trade Agreements. CEPR Press and World Bank.

Francois, Joseph, Marion Jansen, and Ralf Peters. 2011. “Trade Adjustment Costs and Assistance: The Labour Market Dynamics”. In Trade and Employment: From Myths to Facts, edited by Marion Jansen, Ralf Peters, and José Manuel Salazar-Xirinachs, 213–252. Geneva: ILO.

Goldberg, Pinelopi Koujianou, and Nina Pavcnik. 2007. “Distributional Effects of Globalization in Developing Countries.” Journal of Economic Literature 45 (1): 39–82.

Hagemejer, Krzysztof, and Kee Beom Kim. 2010. “Challenges to Social Security in Asia and the Pacific: Crisis and Beyond.” In Social Assistance and Conditional Cash Transfers: Proceedings of the Regional Workshop, edited by Sri Wening Handayani and Clifford Burkley, 23–44. Manila: ADB.

Harvey, Jenna. 2019. “Homeworkers in Global Supply Chains: A Review of Literature”, WIEGO Resource Document No. 11.

Heo, Yoon. 2013. “Assisting Trade Adjustment in Korea: Is it a Facilitating Device for FTA Implementation?” Journal of International Logistics and Trade 11 (1): 87-98.

Hollweg, Claire. 2019. “Global Value Chains and Employment in Developing Economies”. In Global Value Chain Development Report 2019: Technological Innovation, Supply Chain Trade, and Workers in a Globalized World, 63–82. Washington, DC: World Bank.

Horvát, Peter, Colin Webb, and Norihiko Yamano. 2020, “Measuring Employment in Global Value Chains”, OECD Science, Technology and Industry Working Papers No. 2020/01. Paris: OECD.

Indonesia G20 Presidency, “G20 Presidency Note on Policy Setting on Exit Strategy to Support Recovery and Addressing Scarring Effect to Secure Future Growth”, 2022.

ILO. 2014. World of Work 2014: Developing with Jobs.

———. 2015. World Employment and Social Outlook: The Changing Nature of Jobs.

———. 2016. Assessment of Labour Provisions in Trade and Investment Arrangements. Studies on Growth with Equity.

———. 2017. World Employment and Social Outlook 2017: Sustainable Enterprises and Jobs – Formal Enterprises and Decent Work.

———. 2018. “Gender Gaps in the Garment, Textiles and Footwear Sector in Developing Asia”, ILO Asia-Pacific Garment and Footwear Sector Research Note.

———. 2019a. Extension of Social Security to Workers in Informal Employment in the ASEAN Region.

———. 2019b. Preparing for the Future of Work: National Policy Responses in ASEAN+6.

———. 2020a. “The Supply Chain Ripple Effect: How COVID-19 Is Affecting Garment Workers and Enterprises in Asia and the Pacific”, ILO Research Brief.

———. 2020b. “COVID-19 and Global Supply Chains: How the Jobs Crisis Propagates Across Borders”, ILO Policy Brief.

———. 2020c. “The Effects of COVID-19 on Trade and Global Supply Chains”, ILO Research Brief.

———. 2020d. “ILO Welcomes Milestone to End Forced Labour in Viet Nam”, 8 June 2020. https://ilo.org/hanoi/Informationresources/Publicinformation/Pressreleases/WCMS_747233/lang--en/.

———. 2020e. Rapid STED: A Practical Guide.

———. 2021a. Trade and Decent Work: Indicator Guide.

———. 2021b. “COVID-19, Vaccinations and Consumer Demand: How Jobs are Affected Through Global Supply Chains”, ILO Brief.

———. 2021c. “COVID-19 and the ASEAN Labour Market: Impact and Policy Response”, ILO Brief.

———. 2022. Asia-Pacific Employment and Social Outlook 2022: Rethinking Sectoral Strategies for a Human-Centred Future of Work.

———. 2022a. ILO Monitor on the World of Work, 10th Edition.

———. 2022b. Global Employment Trends for Youth 2022: Investing in Transforming Futures for Young People.

———. n.d. “COVID-19 and the World of Work: Country Policy Responses”. https://www.ilo.org/global/topics/coroncavirus/regional-country/country-responses/lang--en/index.htm.

ILO, OECD (Organisation for Economic Co-operation and Development), IOM (International Organization for Migration), UNICEF (United Nations Children’s Fund). 2019. Ending Child Labour, Forced Labour and Human Trafficking in Global Supply Chains.

Kizu, Takaaki, Stefan Kühn, and Christian Viegelahn. 2019, “Linking Jobs in Global Supply Chains to Demand.” International Labour Review 158 (2): 213–244.

Korwatanasakul, Upalat, and Sasiwimon Warunsiri Paweenawat. 2020. “Trade, Global Value Chains, and Small and Medium-Sized Enterprises in Thailand: A Firm-Level Panel Analysis”, ADBI Working Paper Series No. 1130.

Kucera, David, and Fernanda Bárcia de Mattos. 2020. “Automation, Employment, and Reshoring: Case Studies of the Apparel and Electronics Industries.” Comparative Labor Law & Policy Journal 41 (1): 101– 128.

Lee, Joonkoo. 2016. “Global Supply Chain Dynamics and Labour Governance: Implications for Social Upgrading”, ILO Research Paper No. 14.

Montalbano, Pierluigi, and Silvia Nenci. 2020. “The Effects of Global Value Chain (GVC) Participation on the Economic Growth of the Agricultural and Food Sectors”, Background Paper for The State of Agricultural Commodity Markets (SOCO) 2020. Rome: FAO (Food and Agriculture Organization of the United Nations).

OECD. 2017. OECD Skills Outlook 2017: Skills and Global Value Chains.

OECD and UNIDO (United Nations Industrial Development Organization). 2019. Integrating Southeast Asian SMEs in Global Value Chains: Enabling Linkages with Foreign Investors.

Pahl, Stefan, and Marcel P. Timmer. 2019. “Do Global Value Chains Enhance Economic Upgrading? A Long View.” Journal of Development Studies 56 (9): 1683–1705.

Ravallion, Martin. 2006. “Transfers and Safety Nets in Poor Countries: Revisiting the Trade-offs and Policy Options”. In Understanding Poverty, edited by Abhijit Vinayak Banerjee, Roland Bénabou, and Dilip Mookherjee. New York: Oxford University Press.

Shepherd, Ben, and Susan Stone. 2013. “Global Production Networks and Employment: A Developing Country Perspective”, OECD Trade Policy Papers No. 154.

Shingal, Anirudh. 2015. “Labour Market Effects of Integration into GVCs: Review of Literature”, R4D Working Paper 2015/10, World Trade Institute, University Bern.

Singapore Economic Development Board. 2022. “Pioneer Certificate Incentive and Development and Expansion Incentive”. https://www.edb.gov.sg/content/dam/edb-en/how-we-help/incentive-and-schemes/PC%20and%20DEI%20Brochure.pdf.

Solingen, Etel, Bo Meng, and Ankai Xu. 2021. “Rising Risks to Global Value Chains”. In Global Value Chain Development Report 2021: Beyond Production, 134–178. Asian Development Bank, Research Institute for Global Value Chains at the University of International Business and Economics, the World Trade Organization, the Institute of Developing Economies—Japan External Trade Organization, and the China Development Research Foundation.

Thailand Board of Investment. 2021. A Guide to the Board of Investment 2021.

Timmer, Marcel P., Abdul Azeez Erumban, Bart Los, Robert Stehrer, and Gaaitzen J. de Vries. 2014. “Slicing Up Global Value Chains.” Journal of Economic Perspectives 28 (2): 99–118.

Wang, Zhi, Shang-Jin Wei, and Kunfu Zhu. 2013. “Quantifying International Production Sharing at the Bilateral and Sector Levels”, NBER Working Paper No. 19677.

UNCTAD (United Nations Conference on Trade and Development). 2020. World Investment Report 2020: International Production Beyond the Pandemic.

UNESCAP. 2018. Asia-Pacific Trade and Investment Report 2018: Recent Trends and Developments.

United Nations and CIAT (Inter-American Center of Tax Administrations). 2018. Design and Assessment of Tax Incentives in Developing Countries: Selected Issues and a Country Experience.

Viegelahn, Christian. 2017. “How Trade Policy Affects Firms and Workers in Global Supply Chains: An Overview”. In Handbook on Assessment of Labour Provisions in Trade and Investment Arrangements, 109–114. Geneva: ILO.

Wagner, Joachim. 2007. “Exports and Productivity: A Survey of the Evidence From Firm-Level Data.” The World Economy 30 (1): 60–82.

World Bank. 2017. “Jobs in Global Value Chains”, Jobs Notes No. 1.

World Bank. 2020. World Development Report 2020: Trading for Development in the Age of Global Value Chains.

World Bank and World Trade Organization. 2020. Women and Trade: The Role of Trade in Promoting Gender Equality.

Annex

Annex A: Estimates of jobs in global supply chains

This annex describes the data and methodology used to produce estimates of the number of jobs in GSCs.

Data

Estimates of the number of jobs in GSCs are constructed based on a combination of two data sources: The first consists of international input-output tables, which are available for 62 countries worldwide for 2000 and 2007–2021 from ADB’s MRIO Database. These cover 35 sectors and provide information on country-sector level linkages in production. They are combined with a novel balanced panel database of ILO estimates of employment by detailed sector for 1991–2021, developed specifically for this project.

Besides the estimate of total employment in a sector, the ILO’s database also includes for each sector an estimate of employment by sex (male and female), by age group (youth and adult), by employment status (employees and self-employed) and by occupational skill level (high-skilled and low-/medium-skilled). The ILO’s harmonized microdata repository, which is the world’s largest repository of national labour force survey datasets, is the primary source of those labour market indicators. Some additional data were taken from other national sources. These data are cleaned, adjusted for breaks in the data series, as well as for the lack of reliability in case of data points based on less than 30 observations in the labour force survey. All missing data points are estimated using information such as GDP, sectoral value added and employment data from other data sources such as UNIDO or the OECD. The estimation approach followed ILO’s standard methods to estimate labour market data.

Methodology

The methodology applied to estimate the number of jobs in GSCs consists of three main steps.

First, the gross output is calculated for each country and sector that is required to produce one unit of final good demanded in any country and sector. The Leontief inverse matrix allows to determine these technical coefficients and is computed based on international input-output tables from the ADB MRIO Database following standard input-output modelling procedures.

Second, gross output for each sector within a country is translated into a corresponding number of jobs. By dividing employment in a sector by its gross output, the employment input per unit of gross output can be computed. In line with estimation approaches also used by other international organizations, the assumption is made that labour productivity in agriculture of high-income countries, in industry of all countries, as well as in services of all countries does not differ between GSC-related and non-GSC-related economic activity within a sector. For the agriculture sector of upper-middle income and lower-middle income countries, it is assumed that only two-thirds or one-third of workers are needed in GSC-related activities relative to non-GSC-related economic activities. This assumption aims to reflect that the agricultural sector in these countries is often characterized by a large segment with relatively low labour productivity levels, serving mainly local markets, and a small but highly productive segment that is integrated into GSCs serving international markets. 81, 82

Third, a demand vector needs to be defined that captures output produced for GSCs. The methodology used defines the latter to include any type of supply relationship that crosses borders. This includes exports of final goods and services consumed elsewhere, exports of intermediates to for the production of final goods or services consumed globally, or the production of intermediates that are processed further domestically but end up as exported intermediates or final goods or services. When combining the data sources in this way, the methodology produces estimates of GSC jobs for 35 sectors in 62 countries for 2000 and 2007–2021 (

Table A.

|

Section/Division Code |

Industry Name |

|---|---|

|

A-B |

Agriculture, Hunting, Forestry and Fishing |

|

C |

Mining and Quarrying |

|

15-16 |

Food, Beverages and Tobacco |

|

17-18 |

Textiles and Textile Products |

|

19 |

Leather, Leather and Footwear |

|

20 |

Wood and Products of Wood and Cork |

|

21-22 |

Pulp, Paper, Paper, Printing and Publishing |

|

23 |

Coke, Refined Petroleum and Nuclear Fuel |

|

24 |

Chemicals and Chemical Products |

|

25 |

Rubber and Plastics |

|

26 |

Other Non-Metallic Mineral |

|

27-28 |

Basic Metals and Fabricated Metal |

|

29 |

Machinery, n.e.c. |

|

30-33 |

Electrical and Optical Equipment |

|

34-35 |

Transport Equipment |

|

36-37 |

Manufacturing, n.e.c.; Recycling |

|

E |

Electricity, Gas and Water Supply |

|

F |

Construction |

|

50 |

Sale, Maintenance and Repair of Motor Vehicles and Motorcycles; Retail Sale of Fuel |

|

51 |

Wholesale Trade and Commission Trade, Except of Motor Vehicles and Motorcycles |

|

52 |

Retail Trade, Except of Motor Vehicles and Motorcycles; Repair of Household Goods |

|

H |

Hotels and Restaurants |

|

60 |

Inland Transport |

|

61 |

Water Transport |

|

62 |

Air Transport |

|

63 |

Other Supporting and Auxiliary Transport Activities; Activities of Travel Agencies |

|

64 |

Post and Telecommunications |

|

J |

Financial Intermediation |

|

70 |

Real Estate Activities |

|

71-74 |

Renting of Machinery and Equipment and Other Business Activities |

|

L |

Public Administration and Defense; Compulsory Social Security |

|

M |

Education |

|

N |

Health and Social Work |

|

O |

Other Community, Social and Personal Services |

|

P |

Private Households with Employed Persons |

Notes: Based on ISIC Rev. 3.1.

Source: ADB MRIO.

Table A.

|

ISO Code |