What role can health mutuals and community-based health insurance play in social health protection systems?

Review of experiences

Abstract

Social health protection systems are constantly evolving, offering a wide range of institutional, administrative, and financial arrangements. International standards in social health protection are outcome-based, and grant flexibility in the institutional and administrative arrangements chosen by each state to implement these guarantees, as long as certain fundamental principles are upheld. These principles include the establishment of state-guaranteed benefit entitlements, solidarity in financing, and broad risk pooling. The flagship Social Security (Minimum Standards) Convention, 1952 (No. 102), globally recognized as a reference for system design, is thus conceived around the idea that systems are adaptable and that no single model applies universally.

At the global level, mutuals primarily focus on providing complementary or supplementary coverage to basic health schemes. Only a small number of countries incorporate mutuals and community-based health insurance (CBHI) into the architecture of their basic health coverage systems. This working paper explores various country experiences where mutuals and CBHI contribute to basic health coverage within national social protection systems. Despite a wealth of literature on mutuals and CBHI, little is known about the practical methods used to integrate them into national social health protection architectures.

This work is based on a literature review (Niang et al., 2023) and seventeen case studies spanning countries in Europe, Africa, Asia, and Latin America.

This comparative analysis highlights that the involvement of mutuals and AMBCs in national social health protection schemes is the result of a historical process unique to each country, evolves dynamically over time, and varies significantly in the conceptual and legal frameworks that govern them.

Executive Summary

Social health protection (SHP) is a human right rooted in the right to social security and the right to health enshrined in the Universal Declaration of Human Rights (1948) and the International Covenant on Economic, Social and Cultural Rights (1966). This fundamental right is formalized through a range of legal instruments, including ILO standards, 1 which provide a flexible framework for the progressive expansion of all types of social protection system based on social solidarity.

Today, it contributes to the achievement of the Sustainable Development Goals (SDGs) of the 2030 Agenda for Sustainable Development (2030 Agenda), particularly targets 1.3 and 3.8 on universal social protection and universal health coverage (UHC), which is a priority shared at the global level. In addition to the availability of a quality healthcare system, UHC relies on social protection strategies for health, based on the values of solidarity and social justice. These strategies aim to free the demand for healthcare from its financial constraints, thereby enabling everyone to have access to healthcare services regardless of their resources, in the event of illness, accident or disability.

Social health protection systems are constantly evolving and there is now a variety of institutional, administrative and financial arrangements. International standards in SHP are results-based and are not prescriptive in terms of the institutional and administrative arrangements chosen by each State to implement these guarantees, provided that they respect certain basic principles, including the establishment of state-guaranteed benefit entitlements, solidarity in financing and broad risk pooling. The flagship Social Security (Minimum Standards) Convention, 1952 (No. 102), which is recognized worldwide as a benchmark for the development of systems, is built around the idea that systems are flexible and that there is no single model.

At the global level, the role of mutual benefit societies (mutuals) tends to be focused on complementary or supplementary cover to the basic health cover scheme and only a small proportion of countries use mutuals and community-based health insurance (CBHI) in their basic health cover scheme architecture. This working paper examines these different country experiences where mutuals and CBHI have a role in basic health cover within the national social protection system. Despite an abundance of literature on mutuals and CBHI, the description of the operational methods used to integrate them into national SHP systems architecture is still not widely documented and the scope of the definitions varies widely, making comparisons difficult.

The terms "mutual" and "community-based health insurance" are often used interchangeably in the literature. Yet they often refer to very different realities. These two terms tend to bring together a heterogeneous range of organizations from the social and solidarity-based economy, national programmes or even from processes of decentralization of public schemes, which do not all share the common and commonly understood characteristics of mutuality. For the purposes of this working paper, the term mutual is therefore used in a very broad sense, reflecting this diversity, and a more precise classification is also proposed.

This work is based on a literature review

This comparative analysis shows that the involvement of mutuals/CBHI in national SHP schemes is the result of an historical process specific to each country concerned, changes significantly over time and there is great variability in the conceptual and legal frameworks in which they operate.

In countries where mutuals/CBHI have developed in the absence of an organized national SHP system, these have frequently led to an increased use of healthcare by beneficiaries and to their financial protection. On the other hand, they have not led to a significant increase in population coverage and have encountered problems of financial viability, including linked to the low level of pooling of funds.

The experiences that have been successful in terms of extending cover are those in which:

-

from the outset, a national SHP system led to the creation of community mechanisms to ensure its integrated implementation at the local level (Lao People’s Democratic Republic, Rwanda, United Republic of Tanzania);

-

the national SHP institution absorbed the mutuals or CBHI that existed prior to the creation of the national SHP system (Cambodia, Ghana); and

-

the SHP scheme has delegated certain management functions, generally to mutuals or CBHI that existed prior to the SHP system (Belgium, Colombia, Côte d’Ivoire, France, Germany, Japan, Morocco, Uruguay).

In several countries, the role of mutuals within SHP systems has evolved between these different models, which can thus be seen as a continuum in some countries. Conversely, some cases do not yet fall into these categories, where the system is still under construction, as in Burkina Faso.

The experiences where true delegation of management took place:

-

mainly concern “front office” functions, with the “back office” functions (design of scheme parameters, pooling of funds and risks) remaining a public function; and

-

have been facilitated by the clear architecture of the SHP system, with public funding and compulsory membership, and by a professionalization of actors.

The option of integrating mutuals into the implementation of the national strategy for UHC requires the organization of an enabling environment (see below):

-

When management is delegated, it must necessarily be based on an agreement between the health insurance administrator and the mutual in order to clearly define the objectives of the delegation, the mutual’s remit and the operating procedures. The examples observed in Côte d'Ivoire, France, Mali, and Morocco show that these agreements also impose technical constraints on mutuals so as to guarantee their ability to fulfil their functions.

-

Delegation of management must take place within a clear political and regulatory framework. The role of the State is important. It must lead a national dialogue with all stakeholders in order to define the fundamental principles of health insurance and then put in place oversight and regulatory measures.

In countries where SHP systems are emerging, external partners and national non-governmental organizations (NGOs) often influence national options oriented towards CBHI. This responds to the concerns over short-term results of development support programmes. However, building sustainable SHP requires long-term investment.

Introduction

Social health protection (SHP) is a human right rooted in the right to social security and the right to health enshrined in the Universal Declaration of Human Rights (1948) and the International Covenant on Economic, Social and Cultural Rights (1966). This fundamental right is formalized through a range of legal instruments, including ILO standards, which provide a flexible framework for the progressive expansion of all types of social protection system based on social solidarity.

Today, it contributes to the achievement of the Sustainable Development Goals (SDGs) of the 2030 Agenda for Sustainable Development (2030 Agenda), particularly targets 1.3 and 3.8 on universal social protection and universal health coverage (UHC), which is a priority shared at the global level. In addition to the availability of a quality healthcare system, UHC relies on social protection strategies for health, based on the values of solidarity and social justice. These strategies aim to free the demand for healthcare from its financial constraints, thereby enabling everyone to have access to healthcare services regardless of their resources, in the event of illness, accident or disability.

International SHP standards are results-based and are not prescriptive in terms of the institutional and administrative arrangements chosen by each State to implement these guarantees, provided that they respect certain basic principles, including the establishment of state-guaranteed benefit entitlements, solidarity in financing and broad risk pooling. These standards recognize that any system must be adapted to domestic circumstances to be acceptable and effective and that countries may use different approaches to achieve the goal of universal protection through the optimal mix of different institutional arrangements and sources of financing. Countries that have achieved universal coverage in SHP generally combine a variety of funding sources and institutional mechanisms. The flagship Social Security (Minimum Standards) Convention, 1952 (No. 102), which is recognized worldwide as a benchmark for the development of systems, is built around the idea that systems are flexible and that there is no single social security model. Every country must work to develop its own sustainable and progressively comprehensive social protection system, in a manner adapted to national circumstances (ILO, 2020b). In practice, the chosen administrative architecture for the provision of SHP benefits varies from country to country, and mutual benefit societies (mutuals) or community-based health insurance (CBHI) have been identified as playing a role

At the global level, the role of mutuals tends to be focused on complementary or supplementary cover to the basic health cover scheme. However, some countries, which have embarked on major reforms of their health and social protection systems, use mutuals in their basic health cover scheme architecture. These processes have prompted this review of experiences, with a view to examining the role given to mutuals and the methods used for implementation.

Historically, mutuals developed in Europe, Japan and Latin America in contexts where the public protection system was nascent

Despite an abundance of literature on mutuals, the description of the operational methods used to integrate them into national SHP systems architecture is still not widely documented and the scope of the definitions varies widely, making comparisons difficult. This work is also based on a previous literature review

This document presents a summary of these studies, organized into three main sections (see below).

-

The first section proposes a set of definitions of SHP and mutuals in order to map out the scoping review.

-

The second section provides an overview of the role of mutuals and CBHI within SHP systems, based in particular on the above-mentioned scoping review and the 17 countries selected for the case studies.

-

Lastly, the third section deals specifically with the delegation of management and proposes various lessons drawn from these experiences, concerning the current and potential role of mutuals in the context of the West African Economic and Monetary Union (WAEMU).

This summary is followed by case studies for each country.

Conceptual framework

Key messages

-

Countries have a wide range of institutional, administrative and financial arrangements for constructing their national SHP systems, with a common objective of moving progressively towards UHC.

-

The current and interchangeable use of the terms “mutual” and “CBHI” covers very different circumstances; there is not always conceptual clarity in their use, nor a single legal framework at the global level to oversee them.

-

The characteristics of these entities (mutuals/CBHI) are also influenced by the role they play in the SHP system in some countries.

1.1. Social health protection

The ILO defines social health protection (SHP) as "a series of public or publicly organized and mandated private measures against social distress and economic loss caused by the reduction of productivity, stoppage or reduction of earning or the cost of necessary treatment that can result from ill health” (Scheil-Adlung, 2007). SHP is firmly grounded in international law: the Universal Declaration of Human Rights, the International Covenant on Economic, Social and Cultural Rights, ILO Convention No. 102 and the Social Protection Floors Recommendation, 2012 (No. 202). The latter defines SHP as access to healthcare without financial hardship, guaranteed by the State over the life cycle, and income security in cases of sickness and maternity. It contributes to the achievement of the SDGs under the 2030 Agenda, and in particular targets 1.3 and 3.8 on universal social protection and universal health coverage (box 1).

Box 1. Universal social protection throughout the life cycle and universal health coverage: Two key goals of the 2030 Agenda for Sustainable Development (2030 Agenda)

Universal social protection (USP) is firmly grounded in the international human rights framework and international social security standards, including the Universal Declaration of Human Rights, the International Covenant on Economic, Social and Cultural Rights, ILO Convention No. 102 and Recommendation No. 202. USP refers to comprehensive, sustainable and adequate protection for all throughout the life cycle, according to the three core dimensions described below.

-

Universal coverage for persons protected. All should have effective access to social protection throughout the life cycle, if and when needed.

-

Comprehensive protection with regard to the social risks and contingencies that are covered. This includes access to healthcare and income security. Convention No. 102 sets out nine contingencies that every person may face over the course of life. These are the need for medical care and the need for benefits in the event of: sickness; unemployment; old-age; employment injury; family responsibilities; maternity; invalidity; and survivorship (paid to certain relatives in the event of the death of a breadwinner). This dimension also includes protection against new and emerging risks, such as long-term care needs.

-

Adequate protection. Benefits provided need to be set at a level that effectively prevents poverty, vulnerability and social exclusion, maintains a decent standard of living and allows people to lead healthy and dignified lives (ILO, 2021).

In the SDGs, progress on USP is measured through indicator 1.3.1 – Proportion of population covered by social protection floors/systems.

Universal health coverage is defined by the World Health Organization (WHO) as a situation in which all people have access to the full range of quality health services they need, when and where they need them, without financial hardship. It covers the full continuum of essential health services, from health promotion to prevention, treatment, rehabilitation, and palliative care across the life course.

In the SDGs, progress on UHC is measured through two indicators:

-

coverage of essential services (SDG indicator 3.8.1)

-

catastrophic health spending (and related indicators) (SDG indicator 3.8.2)

Virtually all countries have constructed systems based on a combination of different financing mechanisms, which translates into a wide variety of systems on an international scale. This is the result of a pragmatic approach by each country to dealing with a number of specific problems linked to the distribution of the population geographically and by category, the availability of health services, decentralized administration, and so on. International social protection standards recognize this plurality in the institutional and administrative arrangements that each State chooses to implement these guarantees, provided that they respect certain basic principles, in order to build systems that are adapted to domestic circumstances, and are acceptable, effective and financially sustainable (see box 2).

Box 2. International social health protection standard

Universality

The Medical Care Recommendation, 1944 (No. 69) introduced the principle of universality, setting out that healthcare services should cover all members of the community, “whether or not they are gainfully occupied” (para. 8). The right to health was subsequently formally enunciated by human rights instruments. The human rights to health and social security create an obligation to guarantee universal effective access to adequate protection. In this context, SHP represents the optimal mechanism for substantiating these human rights (ILO, 2020).

Financing and institutional arrangements

International social security standards promote collectively financed mechanisms to cover the costs of health services, recognizing recourse to taxes and contributions made by workers, employers and government. Likewise, these standards recognize a range of institutional arrangements, namely national healthcare services, by which public services deliver affordable health interventions, and national social health insurance, by which an autonomous public entity collects revenues from different sources (social contributions and/or government transfers) to purchase health services, either only from public providers, or from both public and private providers. In practice, most countries use a combination of financing sources and institutional arrangements to achieve universal coverage for their population.

The ILO underlines that “there is no one-size-fits-all approach. International standards provide guiding principles for Governments to ensure universal protection in a way that reflects risk-sharing, equity and solidarity in a fiscally, economically and socially sustainable fashion” (ILO, 2020). Strategies to extend coverage have a twofold objective (see below).

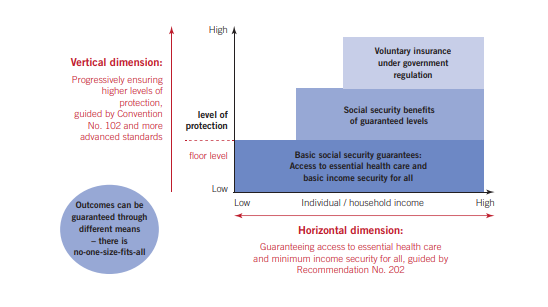

-

Horizontal extension of coverage aims to cover the entire population with at least a minimum level of protection across four basic social protection floor guarantees, including healthcare, in line with ILO Recommendation No. 202).

-

Vertical extension of coverage aims to improve benefit adequacy progressively, ensuring higher levels of protection. International social security standards establish a minimum level of benefit to be guaranteed by law, encompassing two dimensions:

-

range of services actually accessible

-

financial protection against the costs of such services

With respect to the first element, the range of services to be included has to be progressively widened. While social protection floors should include the provision, at a minimum, of “essential healthcare” as defined nationally, including free prenatal and postnatal care for the most vulnerable, countries should progressively move towards greater protection for all, as reflected in Convention No. 102 and the Medical Care and Sickness Benefits Convention, 1969 (No. 130), which stipulate the provision in national law of access to a comprehensive range of services. To be considered adequate, in line with human rights compliance monitoring mechanisms, health services need to meet the criteria of availability, accessibility, acceptability and quality (Recommendation No. 202, Para. 5(a)).

With respect to the second element (financial protection), ILO instruments provide for the right to healthcare “without financial hardship”. Direct payments from households should not be a primary source of financing for healthcare systems. The rules regarding cost-sharing must be designed to avoid hardship, with no or limited contributions and free maternity care.

As illustrated in figure 1, once countries have achieved effective protection for the entire population covering a range of services and financial protection aligned with guaranteed levels of protection in conformity with international standards, complementary and supplementary mechanisms can be put in place under state regulation.

Figure 1. Two-dimensional strategy on the extension of coverage

Source: ILO, 2012.

Within this framework, the State, which is responsible for the SHP system, may choose to entrust one or more ministries or public agencies with its implementation. They may also delegate certain functions to operational bodies. For example, Indonesia has a national health insurance agency, Malaysia has a very low-cost national public health service managed by the Ministry of Health, Thailand has three public agencies covering different population groups, and Switzerland mandates private insurers to implement compulsory, collectively financed health insurance. All of these systems also tend to regulate voluntary private insurance to cover services deemed non-essential (elective surgery, and so on), or to complement basic financial protection by covering the co-payment or additional services (single room during hospitalization, and so on).

1.2. Mutuals and community-based health insurance

The terms "mutual" and "community-based health insurance" (CBHI) (the latter in English describing health insurance mechanisms put in place at the community level) are generally used interchangeably in the literature. However, these organizations often refer to distinct circumstances, and these terms tend to draw together a heterogeneous mix of organizations from the social and solidarity economy, national programmes and even the process to decentralize public schemes, which do not all share the common and generally understood characteristics of mutuality.

This reflects a more general diversity within the social and solidarity economy, where definitions differ according to national contexts as well as the legal framework (ILO, 2022), which can act as a brake on the delegation of public services. However, an international definition was adopted by the ILO in 2022 and then taken up by the United Nations General Assembly in 2023: 2

“The [social and solidarity economy (SSE)] encompasses enterprises, organizations and other entities that are engaged in economic, social, and environmental activities to serve the collective and/or general interest, which are based on the principles of voluntary cooperation and mutual aid, democratic and/or participatory governance, autonomy and independence, and the primacy of people and social purpose over capital in the distribution and use of surpluses and/or profits as well as assets. SSE entities aspire to long-term viability and sustainability, and to the transition from the informal to the formal economy and operate in all sectors of the economy. They put into practice a set of values which are intrinsic to their functioning and consistent with care for people and planet, equality and fairness, interdependence, self-governance, transparency and accountability, and the attainment of decent work and livelihoods. According to national circumstances, the SSE includes cooperatives, associations, mutual societies, foundations, social enterprises, self-help groups and other entities operating in accordance with the values and principles of the SSE.” (ILC.110/Resolution II, part II). 5.)

Furthermore, some countries have used the term "mutual" to designate decentralized public administration bodies (Niang et al., 2023). The use of the terms "mutuality" and "mutuals" thus covers a wide range of organizations from the social and solidarity economy.

The International Association for Mutual Benefit Societies (AIM) confirms that there is no clear definition and that there is a diversity of legal forms. However, the AIM underscores that mutuals have five main characteristics:

-

Mutuals are private legal entities.

-

Mutuals are a grouping of people.

-

The governance of mutuals is democratic.

-

The principle of solidarity is very important among members.

-

Profits are used for the benefit of the members (AIM, 2017).

Box 3. Examples of definitions from around the world

In Europe

In March 2013, the European Parliament adopted a legislative own-initiative report on the Statute for a European mutual society, with the aim of increasing the visibility and recognition of mutuality at the European level and allowing mutual societies to access and benefit from the internal market. The European Commission defined mutual societies as “an autonomous association of persons (legal entities or natural persons) united voluntarily, whose primary purpose is to satisfy their common needs and not to make profits or provide a return on capital. It is managed according to solidarity principles between members who participate in the corporate governance. It is therefore accountable to those whose needs it is created to serve”. There is therefore no clear legal concept of what defines a mutual-type organization in the various Member States, as there are differences concerning traditions, history, (political) choices, markets, governance models and rules. However, the 2013 own-initiative report identifies a set of essential traits (see below) that differentiate mutuals from other economic agents.

-

Mutuals are private entities governed by private law, independent and neither controlled by the government nor funded by public subsidies.

-

Mutuals are a grouping of persons (physical or moral) and a pooling of funds.

-

They are subject to democratic governance.

-

Mutuals organize services and provisions in the interests of their members, on a basis of solidarity and in a collectively financed manner.

-

In return, the members pay a contribution or equivalent, the amount of which may be variable.

-

The members cannot exercise any individual right over the assets of the mutual.

-

The profits are used for the benefit of its members (discounted premiums, and so on) or are reinvested to improve services for the members (ISSA, 2013).

Within the West African Economic and Monetary Union (WAEMU)

A definition is also provided in West Africa through Directive No. 07/2009/CM/UEMOA on regulating social mutual schemes within the WAEMU (2009). This defines mutual organizations, including mutual health organizations, as “associations which, primarily through their members' contributions, aim to carry out, in the interest of their members and their dependants, action in terms of a provident fund, mutual assistance and solidarity to prevent social risks related to the person and to address their consequences”. Article 12 of the Directive sets out the principles for mutuals that distinguish them from other forms of insurance. These principles are described below.

-

Voluntary and non-discriminatory membership consists of a voluntary act of participation in a social mutual society not based on gender, race, nationality, political or religious affiliation.

-

Not-for-profit means that activities are carried out for a purpose other than making a profit.

-

Democratic and participative operation means the participation of members, either directly or through their representatives, in the running of the institution.

-

The commitment to solidarity is based on mutual aid between members, with a view to sharing the risks.

-

Autonomy and independence entail the free administration of the institution's assets in compliance with prudential regulation.

-

Voluntary work means that members of the governing body perform their duties free of charge.

-

Responsible participation obliges members to observe a certain loyalty towards the institution and towards other members.

In Japan

The Ministry of Health, Labour and Welfare defines mutual aid associations as "a social security system designed to help cooperative members help each other and improve the stability and welfare of each other's lives" (Ministry of Health, Labour and Welfare of Japan, daini kyosei kumiai 2020).

In Colombia

Mutual associations are not-for-profit enterprises in the solidarity economy, under private law and solidarity-based with social-interest objectives, freely and democratically constituted by the association of natural persons, not-for-profit legal entities or a combination thereof, which undertake to make contributions to the mutual social fund, in order to help each other to meet their needs and those of the community in general, always with a view to social interest or collective welfare (Law No. 2143 of 2021, article 2).

According to these definitions, a mutual organization is a not-for-profit association of persons (membership being voluntary) with the aim of dealing with the consequences of various social risks for its members and their families. A mutual is financed primarily by its members' contributions, which may be supplemented by other resources, including state subsidies. It is managed by the representatives of its members, and a mutual enjoys complete institutional independence provided it complies with certain principles set out in law. It therefore differs from other SHP mechanisms in that it has a democracy less removed from its contributing members. Mutuals also differ from commercial health insurance in that it is not-for-profit, has a much higher degree of solidarity in a number of respects, and is democratic (Boyer et al., 2000).

It emerges from the scoping review carried out on the subject and the case studies that, depending on the country, the autonomy and independence of mutuals and CBHI are not necessarily a defining element in all national contexts, particularly in Ghana, Rwanda and the United Republic of Tanzania. Similarly, with regard to the voluntary nature of membership, although the freedom to choose a mutual is sometimes mentioned, this does not mean that membership of an SHP scheme is voluntary. Several countries, such as Belgium, France and Morocco, combine compulsory SHP membership with the free choice of a mutual (Niang et al., 2023).

1.2 A wide range of mutual organizations emerging from diverse and dynamic historical processes

The case studies show that there are two main groups of mutual organizations, distinguishable by how they started, their founding objectives and their involvement in, and development within, the SHP system.

Mutuals originating from the world of work

A first group is composed of corporate or work-related mutuals, which originated as mutual benefit societies in industry or were set up by various organizations such as trade unions, professional associations, cooperatives, workers’ organizations in the informal economy, and agricultural organizations. Mutual societies thus appeared and spread widely in Europe during the nineteenth century, on the initiative of industrial workers and other socio-professional groups, with a view to collecting and pooling funds to protect themselves against social risks and to organizing safety nets for members (Grijpstra et al., 2011). In these countries, mutuals were already in existence and covered certain population groups before the introduction of social security schemes. The latter were then constructed from national traditions giving rise to a variety of models, including mutuals.

Box 4. The Belgian example

Mutuals in Belgium are social and solidarity economy organizations emerging from initiatives from different ideological worlds, which have retained their origins even though their religious or ideological references have lost some of their importance over time. The mutuals are grouped into five major unions:

-

Alliance nationale des mutualités chrétiennes (National Alliance of Christian Mutual Insurance Funds)

-

Union nationale des mutualités neutres (National Union of Non-denominational Mutual Insurance Funds)

-

Union nationale des mutualités socialistes (National Union of Socialist Mutual Insurance Funds)

-

Union nationale des mutualités libérales (National Union of Liberal Mutual Insurance Funds)

-

Union nationale des mutualités libres (National Union of Occupational Mutual Insurance Funds)

One of the special features of the Belgian health insurance system is the place and role of mutual societies. Unlike other countries, Belgian mutual societies are responsible for compulsory insurance.

In France, for example, the Morice Law of 9 April 1947, setting up the scheme for civil servants, delegated the management of compulsory health insurance for civil servants to mutuals. Subsequently, Law No. 48-1473 of 23 September 1948 entrusted management of the scheme for students to the Mutuelle des Etudiants, (Students’ Mutual, LMDE) as part of a public service delegation. In Belgium, the State supported the development of the mutual society movement from the nineteenth century onwards, before adopting a compulsory health insurance system for all salaried workers in 1944, with its management being entrusted to mutual societies. The role of mutuals diversified after the Second World War and the emergence of compulsory social protection systems, with mutuals being integrated to manage the compulsory scheme, for example in Belgium and Germany, or as part of a shared management arrangement with the State, as in France, or by offering complementary insurance to the basic scheme managed by the State, as in Spain.

Against this background, and within the meaning of the definition of mutuals in the codes on mutual societies in France and Belgium, mutuals are based on the principle of co-opting, between people who trust each other and who share a strong social capital. These mutuals generally develop a high level of management skills and are pools of expertise that have been put to good use in national systems aimed at extending SHP. Similar processes can be observed in other countries, for example in Japan with mutual aid associations, particularly for civil servants, teachers and seafarers (box 5). The European mutual society movement also played a key role in the development of mutuals in Latin America in the nineteenth century and in Africa with European colonization. This can be seen, for example, in the creation of mutuals within government departments and enterprises, such as the Mutuelle générale des fonctionnaires et agents de l’État de Côte d’Ivoire (General Mutual Fund of Civil Servants and State Agents of Côte d’Ivoire, MUGEF-CI) in Côte d'Ivoire, which was set up in 1973 and now has more than 740,000 beneficiaries. Since 2011, it has been operating as a delegated management organization (DMO) as part of UHC implementation, which has forced it to restructure to comply with Directive No. 07/2009/CM/UEMOA on social mutual schemes in order to benefit from the status of a DMO. In Morocco, the management of the compulsory health insurance scheme for public-sector employees and retirees, which came into force in 2005, has been entrusted to the Caisse nationale des organismes de la prévoyance sociale (National Social Insurance Societies Fund, CNOPS), which is a national union of eight public-sector mutuals created in 1950.

Box 5. Integration of mutuals into the National Health Insurance in Japan

Before the introduction of the National Health Insurance Act in 1958, there were mutuals in Japan set up by civil servants, seafarers and teachers. When national health insurance was introduced, the results of a survey showed that more than 90 per cent of people who had already joined a mutual wished to remain covered by it. Mutuals were integrated into the National Health Insurance with a mandate to cover specific population groups, including civil servants and private school staff. Their health benefits have been harmonized with all other schemes, although they can also offer supplementary cover. However, they set their own contribution rates. Mutuals receive state subsidies towards their operating costs.

Mutuals emerging due to external dynamics

More recently, since the 1990s, small-scale health insurance schemes have been promoted by national and international NGOs, donors and governments, as part of national UHC programmes (Mathauer et al., 2017), particularly on the African continent (box 6). These schemes are managed by, or more often with the participation of, communities and are referred to by the terms "community mutuals" or "community-based health insurance (CBHI)". They are particularly numerous in West Africa, where it is estimated that nine out of ten mutuals are small-scale organizations with fewer than 1,000 beneficiaries (Van Rompaey, 2013).

Box 6. Development of mutuals and community-based health insurance in Africa

In low-income countries, the development of SHP is recent, with the main impetus coming in the 1990s and 2000s. In West Africa, this development can be briefly summarized as three key phases of development (Letourmy, 2008):

-

A first phase, which dates back to the post-colonial era and schemes such as mutuals for the armed forces, came with the development of coverage mechanisms within the formal economy sector only, with very different approaches: compulsory public health insurance institutions (Rwandaise d'assurance-maladie, Rwandan Health Insurance, RAMA) in Rwanda, and the Fonds national d’assurance-maladie, National Health Insurance Fund, NHIF) in the United Republic of Tanzania); state healthcare provision for civil servants (budget allocations in Senegal); company medical schemes (Institutions de prévoyance maladie (IPM) in Senegal); setting up mutuals for civil servants and the armed forces (Côte d'Ivoire, Morocco, Senegal); direct employer responsibility (internal plans or contracts with private insurance companies in Burkina Faso); or the introduction of specific healthcare provision (Office de santé des travailleurs (OST) in Burkina Faso).

-

A second phase came in the 1990s and 2000s with the development of mutuals, CBHI and other microinsurance schemes for people in the informal and agricultural sectors. A wide range of schemes have emerged, both from local initiatives (NGOs, not-for-profit healthcare providers) or external initiatives (World Bank, ILO, international NGOs, European mutual societies, and so on).

-

The third phase developed from the momentum of global campaigns for national social protection floors, UHC and the 2030 Agenda. It is characterized by state involvement and the setting of health coverage policies that must cover all categories of the population and, very broadly speaking, merges the two previous phases. With this third phase, health insurance entered a phase of extension, albeit gradual and still insufficient, but very real. The case studies show that the national policies and strategies implemented in the various countries have developed progressively but differently, following pragmatic approaches and local or well-confined experiments; two major trends stand out (see below).

-

Some countries are developing a national SHP system that brings together all existing schemes in a single architecture to offer the same basic protection for all (examples Côte d'Ivoire and Ghana).

-

In other countries, the SHP system is fragmented, with a juxtaposition of schemes and programmes that divide the population into different categories, each with its own adapted scheme and cover (examples Mali, Rwanda, Senegal).

This dynamic can also be seen outside of Africa. In the Lao People’s Democratic Republic, for example, where a voluntary CBHI scheme has been set up under the supervision of the Ministry of Health to protect people in the informal economy, which accounts for 80 per cent of the total population. The scheme was launched as a pilot project in 2002 and gradually extended from 2006 with the support of external partners. In 2012, CBHI covered only 3 per cent of the total population, in 42 districts in nine provinces. From 2017, the CBHI approach was abandoned in favour of a non-contributory scheme managed by the national health insurance scheme and financed by resources from the national budget.

Similarly, in Cambodia, community mutuals were set up by NGOs across the country in the late 1990s to cover people in the informal economy and in rural areas. They were extended until 2012; however, they only ever reached 3 per cent of the total target population, before experiencing a decline and ceasing to exist after 2018. These mutuals provided the country with first-hand experience to enable the setting up of a national health insurance scheme. This currently covers only workers in the formal sector, but with the aim of gradually extending it to the entire population.

Classification

An important lesson can be drawn from the case studies on the capacity of mutuals to act as delegated managers. A clear distinction needs to be made between the different types of organizations commonly referred to as mutuals or CBHI, based in particular on their professionalization.

-

Professionalized mutuals : Often corporate in nature, they may originate from a variety of organizations such as trade unions, professional associations, cooperatives, workers’ organizations in the informal economy, and agricultural organizations. In this context, and within the meaning of the codes on mutual societies in Belgium or France, these entities are based on the fundamental principle of co-opting, between people who trust each other and who share a strong social capital. The case studies show that the expertise developed by professionalized mutuals is not made use of in many West African contexts. Yet they are pools of expertise that could be put to good use in national systems aimed at the extension of SHP. -

Community mutuals : Community mutuals and CBHI are generally set up through external financing, supported or not by national programmes, on the basis of geographical or administrative areas (village, commune, district, and so on). However, neither trust and social capital nor technical skills in social protection management arise spontaneously from this type of planning (Sossa, 2010). The promotion of community mutuals is often part of a programme approach, with no legislation guaranteeing beneficiaries a right to SHP, nor a regulatory framework guaranteeing adequate oversight to protect beneficiaries. They are therefore often developed in isolation, and their weakness in terms of management limits the potential for delegation of management by a public body responsible for SHP. -

Parastatal bodies commonly referred to as mutuals or CBHI : In a number of countries, the term mutual or CBHI actually refers to decentralized administrative branches forming part of the public or parastatal sector. As explained in the following section, this may be the result of an absorption of the mutual society bodies that preceded the creation of the national SHP system (for example, in Cambodia or the Lao People’s Democratic Republic), or of the architecture of the national SHP system seeking to highlight a certain participatory aspect by using this terminology.

It is therefore important not to underplay the mutual society movement or drown it in a mass of organizations if the aim is to use its social and management capital as a lever for extending social protection.

Overview of the role of mutuals and community-based health insurance in social health protection systems

Key messages

-

Few countries in the world use mutuals in their SHP system for base cover, and the role of mutuals is more often confined to complementary coverage.

-

There is a diverse range of mutuals and of SHP systems themselves, limiting comparability and opportunities for making them widespread. The characteristics of these entities (mutuals/CBHI) are also influenced by the role they play in the SHP system.

-

The experiences that have been successful in extension terms are those in which:

-

from the outset, there has been a centralized SHP model with community mechanisms/branches forming an integral part of the public service;

-

there has been absorption into the national SHP institution;

-

there has been delegation of management by the SHP scheme;

-

where mutuals or CBHI have developed outside these schemes, they have not extended base cover; and

-

there are cases that are not yet in these categories because the systems are under construction or in the process of reform.

-

-

More research and documentation is needed on the delegation of management in particular and the practical arrangements for its implementation, its legal framework and its impact.

2.1. A role primarily focused on complementary and supplementary cover at the global level

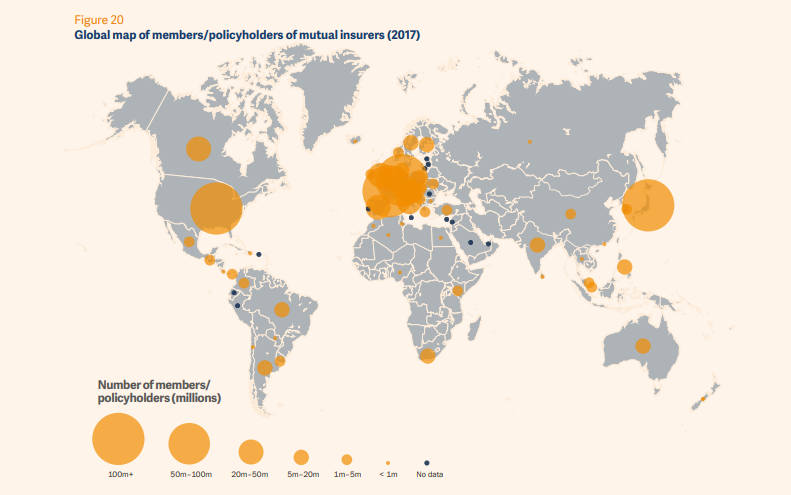

As illustrated in figure 2 below, mutual benefit societies are not found in every country in the world. Moreover, in most countries their role is limited to providing complementary or supplementary cover to the basic scheme, leading to few countries using mutuals in their SHP system for base cover.

Figure 2. Global map of members/policyholders of mutual insurers (2017)

Source: International Cooperative and Mutual Insurance Federation (ICMIF), 2019 2

2.2. The role given to mutuals and community-based health insurance in national social health insurance systems using them for their basic scheme

By studying the information available on the role played by mutuals and CBHI in national SHP systems for the basic scheme, a classification emerges, summarized in table 1, which may also in some cases be a situation that is continuously and dynamically evolving over time (some countries may, in time, be in one or more of the categories below).

Table

|

Delegation of management |

The management organization responsible for public insurance delegates certain management functions to autonomous mutuals for the implementation of base cover for their members. This is generally the case in countries where highly professionalized mutuals predated the SHP scheme. In some cases, the State entrusts the implementation of public insurance to different stakeholders, including mutuals, each covering different target groups of the population. |

France, Belgium, Morocco, Côte d’Ivoire, Uruguay, Colombia, Germany and Japan. |

|

Decentralization |

The SHP system was designed on the principle of setting up decentralized, participative bodies to manage local functions. The entities known as "mutuals" or CBHI are state or parastatal entities and operate as the branches of a national programme. They have only limited autonomy. |

United Republic of Tanzania, Senegal (under departmental health insurance units (UDAM)) and Ethiopia. |

|

Absorption |

When it was set up or reformed, the national SHP system absorbed the pre-existing mutuals or CBHI, thus benefiting from the tools and in some cases even qualified staff. |

Lao People’s Democratic Republic, Cambodia, Rwanda and Ghana after 2003. |

|

Non-involvement |

Mutuals provide base cover where there is not yet a national SHP system setting out the rights for the entire population. In these schemes, mutuals generally benefit from a legal status and framework for their regulation, and act as voluntary mechanisms responsible for all insurance functions. |

Burkina Faso, Senegal and Mali before the recent reforms. |

Delegation of management to autonomous mutuals

Delegation of management to professionalized mutuals that predate the national SHP system is another strategy observed in several countries, including Belgium, Colombia, Côte d'Ivoire, France, Mali, Morocco and Uruguay. In these systems, the State gives a national health insurance fund the task of implementing the insurance scheme and chooses to delegate certain tasks to a limited number of organizations such as mutuals or private insurers. The delegation of certain functions to mutuals is often the result of a process based on historical considerations and aimed at preserving a tradition of mutual organizations rooted in certain socio-professional groups.

The aim of delegating management is to transfer some or all of the responsibilities and tasks linked to management to a third party. This outsourcing is often accompanied by a delegation of the decision-making power associated with these responsibilities and tasks. Mutuals are required to meet certain conditions in order to become delegated managers of compulsory health insurance, particularly in terms of volume of beneficiaries and technical and financial capacity. They have little or no autonomy over the scheme’s parameters, and the tasks delegated are limited and highly regulated.

Box

This is the case in point in Belgium, where general health insurance administration is undertaken by the Institut national d’assurance-maladie-invalidité (National Institute for Health and Disability Insurance, INAMI), with management delegated to the unions of mutual benefit societies, which in turn delegate some of their functions to their member mutual benefit societies. In Morocco, the compulsory health insurance scheme for civil servants (assurance-maladie obligatoire, AMO-public) is managed by the CNOPS, which is a federation of eight mutuals that act as delegated managers. As a result of failings, the CNOPS is in the process of being replaced by the Caisse marocaine de l’assurance-maladie (Moroccan Health Insurance Fund, CMAM), with mutuals remaining delegated managers.

In Côte d'Ivoire, health insurance is managed by the Caisse nationale d’assurance-maladie (National Health Insurance Fund, CNAM), which was initially designed as a simple governance and regulatory structure for universal health cover. The CNAM delegates the functions of registration, collection and benefits to various stakeholders with previous experience, including the MUGEF-CI. The strategy for extending health cover to the informal economy is based on delegating management to mutuals, but the CNAM is developing at a slow pace. Côte d'Ivoire is therefore seeking to encourage the creation of mutuals, organized more by type of trade or sector of activity, which could act both as delegates of the CNAM and as complementary cover for insured persons.

The same trend can also be observed in Mali, where the State is seeking to bring its universal health insurance scheme into operation. The scheme is to be administered at the national level by the Caisse nationale d'assurance maladie (National Health Insurance Fund, CANAM), with management delegated to public funds for the formal sector and to the Union de la mutualité malienne (Malian Mutual Union) for informal sector households and the farming community. While waiting for this scheme to come into operation, cover for the latter will be provided by developing mutuals, including mutuals that in several respects (parameters defined as part of the National Strategy for the Extension of Health Coverage) are more akin to CBHI than to mutual insurance.

The system in place in Colombia is also part of this group. The State, through the Ministry of Health and Social Protection, has the role of steering the SHP system and defines its parameters. The collection of contributions and the purchase of benefits are delegated to health promotion entities (Entidades promotoras de salud - EPS); the contributions are paid and pooled at the level of the Entidad administradora de los recursos del sistema general de seguridad social en salud (ADRES), attached to the Ministry of Health and Social Protection, which redistributes them to the EPS according to the number of beneficiaries (capitation).

Some national schemes do not depend on the creation of a health insurance management organization centralizing the operation of the insurance scheme at the national level by choosing, or not, to delegate some functions to other actors. In these schemes, the management of the basic scheme is entrusted to different types of actors, including social security funds, company funds, trade guilds and mutuals, tasked with covering certain population groups. These actors enjoy a high degree of autonomy within a legal framework set by the State, which plays a regulatory role. This model allows the State to influence the development of the SHP system, while freeing itself from direct administration and relying on the expertise of the management organizations.

Germany illustrates this model with a public insurance system decentralized since its creation. The management of public health insurance is entrusted to a variety of decentralized insurance funds with complete management autonomy, a large proportion of which are governed by mutual societies. However, the system is now increasingly regulated by the federal government and the number of funds has fallen sharply (from 35,000 at the end of the nineteenth century to 105 in 2022). Similarly, in Japan, 85 mutual aid associations manage compulsory health insurance for national and local public employees, teachers and private school staff. These mutuals offer the same benefits as other compulsory health insurance schemes, but set their own contribution rates based on their yearly expenditure.

Some countries classified here in other categories are also part of this decentralization model, such as Rwanda, which illustrates the absorption of mutuals by the Rwandan Social Security Office. However, the latter does not cover the entire population, and other systems are in place for the military, students and private enterprises. Morocco is another example, with the various economic social groups managed by three major stakeholders: the CNOPS (public-sector employees and students), the Caisse nationale de sécurité Sociale (CNSS) (private-sector employees and the self-employed) and the Agence nationale de l’assurance-maladie (National Health Insurance Agency, ANAM) (poorest members of the population). However, Morocco is classified here under delegated management schemes providing cover for public-sector employees and retirees.

Mutuals as decentralized structures of an SHP system

The experience of community mutuals has inspired some countries to adopt this approach as part of national CBHI programmes. The aim of these programmes is to roll out a geographically close network of services to all communities throughout the country, such as in the Lao People’s Democratic Republic (where CBHI was set up by the government, with the support of external partners), Senegal's Décentralisation de l’assurance-maladie (Decentralization of Health Insurance, DECAM) programme and Ethiopia's Health Extension Programme (HEP). Other examples include Rwanda and Ghana, before the mutuals were absorbed and merged into the national health insurance system. This aim can be summed up in the slogan for the DECAM project: "One local community, at least one mutual". In this context, the term mutual or CBHI actually refers to decentralized administrative branches forming part of the state or parastatal sector, with a certain degree of community participation.

This scheme may include two levels of intervention by mutuals or CBHI:

-

Mutuals are simply branches limited to carrying out procedures defined at the national level.

-

Mutuals are able to offer complementary cover or other services to their members, thereby retaining a degree of autonomy.

Box

The aim of decentralizing health insurance by setting up community mutuals throughout the country is to reach all sections of the population through local structures. The experiences of countries such as Ethiopia, Ghana, the Lao People’s Democratic Republic and Senegal shows that this deployment is also the main weakness of this approach.

In the various countries concerned, these approaches have been built on promising initial experiences taking place on a small scale, but their success has been undermined as CBHI was rolled out and made more widespread. This led to the dispersal of community mutuals and the inability of the national promoter to ensure quality coordination, oversight and technical support, and to provide training in the skills needed as the system was extended. As a result, many challenges have arisen in CBHI. They are listed below.

-

lack of human resources and motivation of management committee members working on a voluntary basis in addition to their other professional duties

-

lack of budget and operating resources

-

lack of awareness-raising and communications campaigns

-

failings in the registration and renewal of memberships, the updating of information on policyholder cards, contribution deposits, and so on

-

inaccuracy or non-compliance with management procedures and national guidelines

-

poor governance in some CBHI, non-compliance with national guidelines and corrupt practices in the management of healthcare claims

-

inadequate implementation of fraud control measures, adverse selection and prevention of benefit cost overruns

-

lack of cooperation from healthcare providers (non-compliance with drug lists and tariffs, over-billing, fictitious, erroneous or overcharged services, excessively long deadlines for submitting claims, and so on)

These difficulties tend to discourage new memberships and renewals, or to encourage households to renew their membership only when there is a known need to use health services (elective surgery, an individual at high risk of illness in a household, and so on), which generates a risk of adverse selection and leads to financial problems for health insurance, exacerbated by poor risk pooling.

Absorption

One scenario observed in the case studies is the absorption of mutuals by the SHP system. This situation can be seen in Cambodia, the Lao People’s Democratic Republic and Rwanda after 2014, and Ghana after 2003, where the mutuals promoted under national programmes were dissolved and replaced by branches or other decentralized structures responsible for local services and governance. This approach is generally justified by the desire to improve the efficiency, rationalization and harmonization of population coverage.

In Rwanda, for example, the administration of CBHI was taken over and centralized by the Rwanda Social Security Board (RSSB) from 2015. Staff from community mutuals were integrated into the RSSB to represent insurance at branches set up in health facilities. Similarly, in Ghana, most of the 145 district mutuals that operated as independent schemes have been integrated into a single national health insurance system since 2012, becoming district offices under the technical and financial management of the National Health Insurance Authority (NHIA). In Cambodia, CBHI schemes, generally supported or even managed by an international or local NGO, were dissolved after 2018 and coverage integrated into the SHP schemes currently in operation managed by the National Social Security Fund (NSSF). This is also the case in the Lao People’s Democratic Republic, where the CBHI scheme has been replaced by a tax-based "national health insurance", with no prepayment required but payment of a reduced amount when health services are used; CBHI continues to exist in the capital, however. The pattern is more mixed in the United Republic of Tanzania, where the management of CBHI has been taken over by the NHIF, which is developing improved CBHI (improved Community Health Fund - iCHF) and continues to belong to the districts and regions, but with technical management provided by the NHIF.

In France, a return to the delegation of management to the historical mutual societies for students and civil servants has led to the closure of some mutuals. Others have stopped participating in the management of the compulsory scheme and are now focusing on complementary cover. The health insurance fund has also proposed new types of partnership to the civil service mutuals, based in particular on shared management and the use of the same information system.

Mutuals in the absence of a basic public insurance scheme

At the global level, the role of mutuals is limited in most countries to providing complementary or supplementary cover to the basic scheme, meaning that few countries are using mutuals in their SHP system for base cover (including the case study countries).

In other countries, the absence of SHP, which sets out the rights of the entire population in terms of a healthcare package and financial protection, has been at the root of the creation and development of mutual societies within the world of work, particularly in Europe. More recently, in countries such as Burkina Faso, Cambodia, Mali and Senegal, prior to recent reforms and the construction of national SHP schemes, this has led to the promotion of mutual societies by NGOs or external partners with a view to offering basic protection to communities, generally identified on the basis of geographical or administrative area (village, commune, district, and so on). Thus, these community mutuals are generally set up as a result of external initiatives and under a project approach, with no legislation guaranteeing beneficiaries a right to SHP, and so often developing in isolation. They are generally rolled out by replicating a successful initial experience, through a support structure that defines the technical parameters of the insurance and remains heavily involved in the management of the mutuals for the duration of the projects. An inventory of mutuals in Burkina Faso in 2020 showed that mutuals set up under projects undertaken by national NGOs and financed by donors and backers were no longer in operation after the projects ended, due to a lack of follow-up by the NGOs (Burkina Faso, 2022). The same situation can be observed in Cambodia, where CBHI systems were built on a similar organizational and operational model and were managed by NGOs with the support of development partners. These systems began to decrease in number from 2014 and then stopped in 2018, following the withdrawal of support projects.

In the various countries, any successes of the initial small-scale experiences were quickly eroded when they were rolled out nationwide, and a number of challenges were identified through the case studies, including in terms of governance, human, material and financial capacities, efficiency of procedures, and cooperation with service providers, in addition to the inability of the support structures to ensure quality coordination, oversight and technical support as the system was extended. These challenges are similar to those detailed in box 8 on decentralized structures.

Box

Latin American countries addressed the issue of extending social protection in the 1970s. In Africa, the issue began to be addressed through marginal projects in the early 1990s, with the development of community-based systems combining traditional mutual aid practices and insurance mechanisms to cover the risk of illness. These initiatives multiplied in the 2000s, promoted by a wide range of stakeholders, in order to meet the priority needs of populations excluded from formal social security schemes. The vision widely shared by all stakeholders at the time was that the proliferation of mutual health insurance projects should ultimately lead to cover for all.

A number of lessons can be drawn from this process of developing community mutuals. Various innovative approaches have been developed and some mutuals have demonstrated their ability to reach a significant proportion of individuals at community or organization level (for example, cotton producers in Benin and Burkina Faso), with good results in terms of the financial protection provided and the impact on the use of health services. These experiences have also made a major contribution to popularizing insurance mechanisms among people in the informal economy and rural areas.

However, despite locally successful experiences, the systems put in place cover only a small proportion of these populations overall, have weak management capacity and remain financially very fragile. Overall, the systems set up by support organizations and external funding under project approaches are not capable of instilling trust and mobilizing social capital or technical skills in social protection management (Sossa, 2010).

In addition, these experiences have generally promoted a vertical vision of social protection, with compartmentalized responses for each population group, separating systems for the poorest people, workers in the informal economy and rural areas, and those in the formal sector, with no cross-cutting solidarity mechanisms.

Type of functions performed

Some functions seem to be delegated more than others and/or with greater success. In particular, in all the delegation experiences the accredited mutuals were given local responsibilities, in other words, management of registration, sometimes the collection of contributions, management of beneficiaries, local governance, and management of reimbursements/payments to healthcare providers.

The brief summary compilation presented in the table below does not reflect all the variations observed in the case studies. It does, however, identify a general trend: the main advantage sought in the delegation of management is to make use of the proximity of mutuals to certain population groups. This is particularly so in situations where the vast majority of individuals are involved in the informal economy and agriculture, with all the attendant complexity in terms of identification, contributory capacity and collection. The role assigned to community mutuals in CBHI promotion programmes is significant in this respect. Community mutuals are developed as local and participatory management mechanisms, intended to serve as a gateway to SHP and as points of service for a highly heterogeneous and dispersed population. In other countries, where the formal economy is more widely developed and individuals are more easily identifiable through the employment relationship and tax framework, the choice of delegation is also based on the proximity of mutuals to certain target groups, but is justified more by a political will to preserve the historical role of pre-existing mutuals, or even the benefits acquired by the socio-professional groups at the root of these mutuals.

In contrast, the situations seem more varied for decision-making functions concerning the parameters of coverage, the pooling of resources, risk sharing, financing (including contribution rates, if applicable), and relations with healthcare providers at the national level (contracting, tariff negotiations). In several countries, these functions are centralized and seen as the prerogative and duty of public bodies

Table

|

|

Decision on coverage parameters |

Implementation |

||||||||||

|

|

Population coverage |

Healthcare package |

Level of financial protection |

Healthcare provider network |

Information and promotion |

Membership |

Contribution collection (if applicable) |

Contracts with healthcare providers |

Payment of benefits |

Provision of healthcare services |

Quality control |

Complaints mechanisms |

|

Belgium |

|

|

|

|

X |

X |

X |

X |

X |

X |

|

|

|

Burkina Faso |

|

|

|

|

X |

X |

|

X |

X |

|

|

|

|

Cambodia before 2018 |

|

|

|

|

X |

X |

X |

X |

X |

|

X |

|

|

Colombia |

|

|

|

X |

X |

X |

|

|

|

X |

|

|

|

Côte d’Ivoire (1) |

|

|

|

|

|

X |

X |

|

X |

|

|

|

|

Ethiopia |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

France |

|

|

|

|

X |

X |

|

|

X |

|

|

|

|

Germany |

X |

X |

X |

X |

X |

|||||||

|

Ghana |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

Japan |

|

|

|

|

|

X |

X |

|

|

|

|

X |

|

Lao People’s Democratic Republic |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

Mali (1) |

|

|

|

|

X |

|

X |

|

X |

|

|

|

|

Morocco |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

Rwanda |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

Senegal |

|

|

|

|

X |

X |

X |

X |

X |

|

|

|

|

United Republic of Tanzania |

|

X |

|

|

X |

X |

X |

X |

X |

|

|

|

|

Uruguay |

|

|

|

X |

X |

X |

|

|

|

X |

|

|

-

Functions delegated to DMOs, including mutuals

Thus, a division of functions between the public bodies responsible for SHP and the delegated mutuals can be observed:

-

The public bodies responsible for SHP retain a number of key “back office” functions:

-

In all countries, the coverage parameters (healthcare packages, reimbursement rates, contribution rates, and so on) are defined at the national level and are imposed on the delegated mutuals. As noted in the table, mutuals in some countries (Cambodia, Ethiopia and Ghana) can set or adjust contribution rates.

-

Healthcare providers are generally identified at the national level, as part of a concerted national accreditation and agreement process, with or without the participation of mutuals.

-

Except in the case of CBHI, risks and resources are pooled at regional or national levels.

-

The monitoring and steering of the SHP system and the performance of delegated tasks are carried out at the national level, by the delegator or by a public body designated for that purpose.

-

-

The activities delegated to mutuals primarily concern the insurance business directly linked to insured persons and healthcare providers, known as “front office” functions:

-

Registering and managing memberships, including poor households exempt from paying contributions, with the support of the administrative, traditional and religious authorities and sometimes door-to-door collection agents, in the case of CBHI.

-

Collection of contributions. France and Belgium stand out for having set up social security bodies dedicated to contribution collection.

-

The collection and handling of user complaints is often the responsibility of the delegated mutual, but some countries have set up a specific regional or national mechanism.

-

It should also be noted that some functions are carried out jointly. Table 3 summarizes examples of divisions of operations taken from the case studies.

Table

|

Education/Promotion |

|

|

Function of mutuals |

Function of the management organization |

|

In Belgium, mutuals are in close proximity to their members through their local mutual society branches and offices, and organize information and health promotion activities, to which they attach high importance. In Burkina Faso and Cambodia, the NGOs responsible for implementing the community mutuals work with them on promotion and education activities. In the United Republic of Tanzania and Senegal, mutuals carry out promotion activities with the national agencies that support them. In Colombia and Uruguay, mutuals are required to carry out promotion and prevention activities for members, such as information, education, training and communications. In the Cambodia example, some systems set up networks of agents who make door-to-door visits and organize village meetings. |

In most countries, insurance management organizations, ministries or other public agencies run national campaigns jointly with mutuals. |

|

Membership/renewal |

|

|

Function of mutuals |

Function of the management organization |

|

In all countries, delegated mutuals are in charge of the enrolment and membership of insured persons and beneficiaries. In Côte d'Ivoire, delegated structures are specifically designated for this function. In Uruguay, beneficiaries register with public or private healthcare providers. |

In Morocco, the CNOPS, in coordination with mutuals, handles employer enrolment, registration and membership and updates the administrative status of insured persons. In Mali and Côte d'Ivoire, the final registration of enrolments is undertaken by the national fund. In Côte d'Ivoire, the fund has deployed a computerized network of terminals and enrolment sites throughout the country, which handle registration, enrolment and the issuance of policyholder cards, to make up for the lack of delegated structures. |

|

Recovery/collection of contributions |

|

|

Function of mutuals |

Function of the management organization |

|

In most countries, contributions are collected by mutuals or dedicated delegated bodies, as in Côte d'Ivoire. In some countries, contributions are paid to the management organization. |

In Belgium and France, contributions are collected by administrative bodies responsible for social security funds. In Uruguay, contributions from worker and employer members of the contributory scheme are collected by the Social Security Bank. In Morocco, contributions for civil servants (employer and worker parts) are paid to the CNOPS. |

|

Pooling |

|

|

Function of mutuals |

Function of the management organization |

|

In Senegal and Rwanda (before 2015), member contributions are kept at the level of community mutuals (low level of pooling). State subsidies, which complement these contributions, are pooled at regional and national levels to cover secondary and tertiary care. In Japan, resources and risks are pooled at mutual society level. |

In all other countries, resources are pooled at the level of a public body or a federative structure to which the mutuals pay the contributions collected. These bodies redistribute resources and pool risks at regional or national level. |

|

Contracts |

|

|

Function of mutuals |

Function of the management organization |

|

In CBHI programmes, mutuals sign agreements with the (mainly public) healthcare providers in their area of intervention, often on the basis of a standard agreement provided by the national agency. In Colombia, Health Promotion Enterprises (EPS) have contracts with service providers. |

In other countries, agreements or approvals are signed by the insurance management organization or by the ministry responsible for health. |

|

Payment for services/purchases |

|

|

Function of mutuals |

Function of the management organization |

|

In CBHI programmes, mutuals act as purchasers, on a fee-for-service or capitation basis, as in the case of the EPS in Colombia. In Japan, providers' invoices are sent to the "Healthcare bill check and payment organization”, which pays them and then charges the mutuals concerned. |

In other countries, mutuals oversee benefits and arrange reimbursements to healthcare providers; payments are made by the national management body (or by the regional federations in Germany). In France, mutuals paid service providers and were then reimbursed by the health insurance fund. |

|

Service provision |

|

|

Mutuals providing health services |

No health services |

|

In Germany, France, Belgium and Japan, mutuals can provide health and support services through the health facilities they manage. In Morocco, the law prohibits mutuals from managing health services; some mutuals with medical units have created autonomous mutual society structures to manage them. |

Mutuals in other countries do not manage health services. |

|

Feedback/user complaints/quality assurance |

|

|

Mutuals |

Other |

|

In France, delegated mutuals were in charge of service quality, but with serious shortcomings. In Japan, there is no official harmonized complaint system, so users go through their mutual. Members of community mutuals can complain to their representatives on the management bodies (General Assembly and Governing Body). |