Balancing Act

The Role of Digital Platforms in Shaping the Conditions of Creative Work

Abstract

The platformization of the creative economy has fundamentally reshaped the organization, production and monetization of creative work. This paper examines how digital platforms transform employment relations in creative industries, focusing on the structural tension between platform control and worker autonomy. It considers both conventional artistic occupations—such as musicians, photographers and performers—and emerging platform-native professions including bloggers, streamers and digital content creators.

The study adopts a qualitative, theory-informed methodology that combines political economy analysis of platform governance with a structured synthesis of literature and comparative evidence across platform types. The approach centres on how algorithmic management, revenue-sharing models and data-driven intermediation shape labour market outcomes, including earnings distribution, employment status and career paths. By situating platform work within broader institutional and market contexts, the paper highlights heterogeneity across occupations, worker profiles and regulatory environments.

The findings underscore the dual nature of platformization. On the one hand, platforms lower barriers to entry, expand access to global audiences, and enable flexible and entrepreneurial forms of work. On the other, they generate new forms of precarity characterized by income volatility, opaque algorithmic governance, weak bargaining power and increasing concentration of market power among a small number of dominant intermediaries. Platform architectures not only mediate transactions but actively shape creative practices, visibility and income opportunities, influencing both individual behaviour and sectoral dynamics.

The paper argues for a more coherent policy response that integrates labour market regulation, competition policy and cultural policy to address emerging risks. Priorities include strengthening labour protections, improving transparency and accountability of algorithms, ensuring fair remuneration and safeguarding intellectual property rights. It concludes by identifying key research gaps, particularly around measurement frameworks for platform-based creative work, long-term career trajectories and the implications of artificial intelligence for creative labour markets.

Introduction

The term “platformization” describes the rise of the platform as the dominant infrastructural and economic model of the web and its expansion and integration into other websites, apps, and industries (Helmond 2015). Indeed, today we interact on the web mainly through digital platforms, and they have become part of our everyday lives, defining and shaping how we communicate with each other, how we work and how we buy and sell goods and services.

Platform operators, many of which started as digital "disrupters", are now vast multinationals and publicly traded companies, such as Facebook, YouTube, Uber, Spotify and Amazon. Recently we have witnessed a large consolidation of platform companies, followed by attempts to reduce platform power through a spate of monopoly litigation in parts of the world.

Platformization is reshaping entire industries and markets. One sector that has faced a heavy restructuring is the creative industry. Platforms have penetrated nearly every aspect of the economic, infrastructural and governmental foundations of the cultural industry, forcing a remaking of cultural practices of labour, creativity and democratic structures (Nieborg and Poell 2018). Platforms have achieved these transformations not only as social, political and economic entities but also as discursive constructs that shape and are shaped by the narratives they promote (Gillespie 2010; Banks 2007).

In past years, there has been a significant trend towards the consumption of creative products like music, film, photography and literature through digital platforms, a trend that has forced the artists, authors and filmmakers behind these industries to adapt to the new ways consumers view their creations. These “creative workers” are experiencing positive effects stemming from the potential access to new audiences that platforms offer and their ability to break down traditional market structures, but also adverse effects stemming from copyright restrictions, steep competition, an absence of relevant regulation and challenging working conditions.

Concerns have emerged centring on the idea that the rapid growth in digital platforms has come at the expense of the workers behind the platforms. Platform workers face unstable work arrangements including low pay, zero-hour contracts, discrimination and weak or no social benefits (De Stefano 2015). However, previous research and policy have mainly focused on the employment situations of so-called "app-based" workers such as ride hailing drivers and delivery workers. Relatively little in-depth analysis has been done on another type of labour, which can be described as "content creation", “playbour” (a merging of the words “play” and “labour”) or, using Casilli's (2019) term, the work of "produsers” (a merging of “producer” and “user”).

This working paper focuses on creative workers and how their employment has been affected by the platformization of the cultural industries. The research methodology applied involves a multifaceted approach to understanding the complex interactions between platforms and creative labour. The paper employs a combination of literature review, conceptual framework development and empirical analysis to explore how platformization affects the working conditions of creative workers. The literature review presents differing perspectives on the democratizing potential of digital platforms, balancing their promise of enhanced accessibility and opportunities for creative work with the challenges they pose regarding fairness and working conditions. It synthesizes a range of academic viewpoints, from optimistic outlooks on increased opportunities to critical assessments that emphasize instability, overwork, and the casualization of labour. By situating the discussion within broader academic traditions of political economy and cultural studies, the paper aims to offer a nuanced analysis of the impact of digital platforms on creative workers' autonomy, income stability and overall working conditions. In doing so, the paper will identify research gaps while pointing to new areas of inquiry.

Defining and contextualizing digital platforms, the creative sector and creative workers

Recent scholarship strives to bring to light how working conditions in the creative sector are being redefined due to the influences of digitalization, focusing mainly on digital platforms. Given the novelty and rapidly evolving nature of the topic and the potential for misinterpretation, it is important to define key terms such as “digital platform,” “creative sector,” “content industry” and “creative” or “content” worker.

The creative sector and the content industry

This paper considers both the creative sector and the content industry. A sector describes a large segment of the economy, whereas an industry refers to a specific group of similar types of companies. The main relevant international classifications to consider are those in the International Standard Industrial Classification (ISIC) and the International Standard Classification of Occupations (ISCO). Countries and regions use different categorizations for the creative sector with many alternatively terming it the “cultural” sector. ISIC classifies the sector as “creative, arts and entertainment” activities, whereas the European Union (EU), and increasingly the Organisation for Economic Co-operation and Development (OECD), use “creative and cultural sector”, which includes seven sub-sectors including performing arts, music and visual arts, crafts, cultural heritage, film, book publishing and press, and radio, television, games and animation.

However, the activities included in the creative or cultural sector designation have come under increasing criticism, and there is a lack of conformity amongst countries on their definitions in survey work (Qmetrics 2022). Many occupations and activities are considered only “partially” cultural, leading to underestimation in official statistics. Surveys that report on respondents’ jobs sometimes capture only primary employment even though many individuals’ creative pursuits represent secondary sources of income.

On the other hand, in a narrow application, only activities that are “artistic in nature” (Hesmondhalgh and Pratt 2005) and non-utilitarian functions should be categorized as creative. The approach of this paper is not to include all activities in the creative sector, but rather only those economic activities, and their associated workers or occupations, that have high levels of interactions with digital platforms and are particularly impacted by them.

A more useful path to distinguishing the creative sector would be to identify the most popular creative outputs or products, given that digitalization is strongly associated with the commercialization of creative products. In the creative sector, music, film, images, books, and video games are examples of cultural products whose distribution and consumption are increasingly dominated by digital platforms. The dominant platforms include Amazon, Netflix, Spotify, YouTube and Apple Music but also mainstream social media platforms like Facebook, Twitter and TikTok. Together, these platforms make up the “content industry” (Aguiar, Reimers and Waldfogel 2022), an umbrella term that encompasses the companies that distribute, and in some cases own and create, media and creative products through digital platforms.

Creative digital platforms

There exist many different definitions of digital platforms, and the understanding of a digital platform depends on the context in which it is being used. A generally accepted, broad definition comes from the OECD (2019): “Digital platforms are online entities providing digital services and products that facilitate interactions between two or more distinct but interdependent sets of users, such as firms or individuals, who interact through the service via the internet”. There are three common traits amongst all types of platforms: the existence of the internet to connect users and services; the strategic use of data; and a network effect, meaning the more users connect through the platform, the more valuable the service becomes. Traditionally, platforms have been viewed as inherently disruptive, aiming to shape large-scale transformations of markets across existing industries (Graz 2019), although today they are a mainstream feature of many industries, including the creative industry.

Similarly, different typologies of platforms exist, with no “one-size-fits-all”. Platforms can be organized by function (what they do or the type of service they offer), the type of user (such as advertiser, seller, worker), the type of data they collect, or how they collect revenue (through ads or subscriptions). For this paper, we are interested in both the function and the type of user. In terms of the user, we use the term “creative worker” or “content creator” to refer to someone who produces creative material and is interested in monetizing that material through distribution on an online platform. This type of user is related to but distinct from a user of a digital labour platform where workers offer their services (their labour) on platforms and receive payment for these services (ILO 2018). Digital labour platforms have a structured work organization to enable matches between supply (the worker) and demand (the requester or employer). An agreement is established between the client and the worker, with terms of payment, to fulfil that request. This contrasts with a creative platform where workers post content they deem likely to be popular and are compensated (or not) based on the level of advertisement or viewership that the content attracts. The two defining features of a digital labour platform — the existence of a request for services and an organization of work — are included in several proposed legislations defining what a digital labour platform is. This includes article 2(1)(1) of the EU’s proposed platform work directive (European Parliament and Council 2019). Researchers have nonetheless questioned the legitimacy and legal justification to exclude creative workers from regulation related to digital labour platforms (see Silberman et al. 2023).

Content creators

The term “content creator” designates the activities of contributors to social media and other types of media platforms. These workers contribute, either paid or unpaid, creative content such as blogs and vlogs, music, videos, photographs, stories and podcasts to platforms. Content creators include newly minted occupations that emerged in the wake of the advent of digital platforms. These content-creating occupations comprise, among others, influencers, live-streamers, video creators and bloggers (Casilli 2021) but also traditional creators such as musicians, authors and photographers.

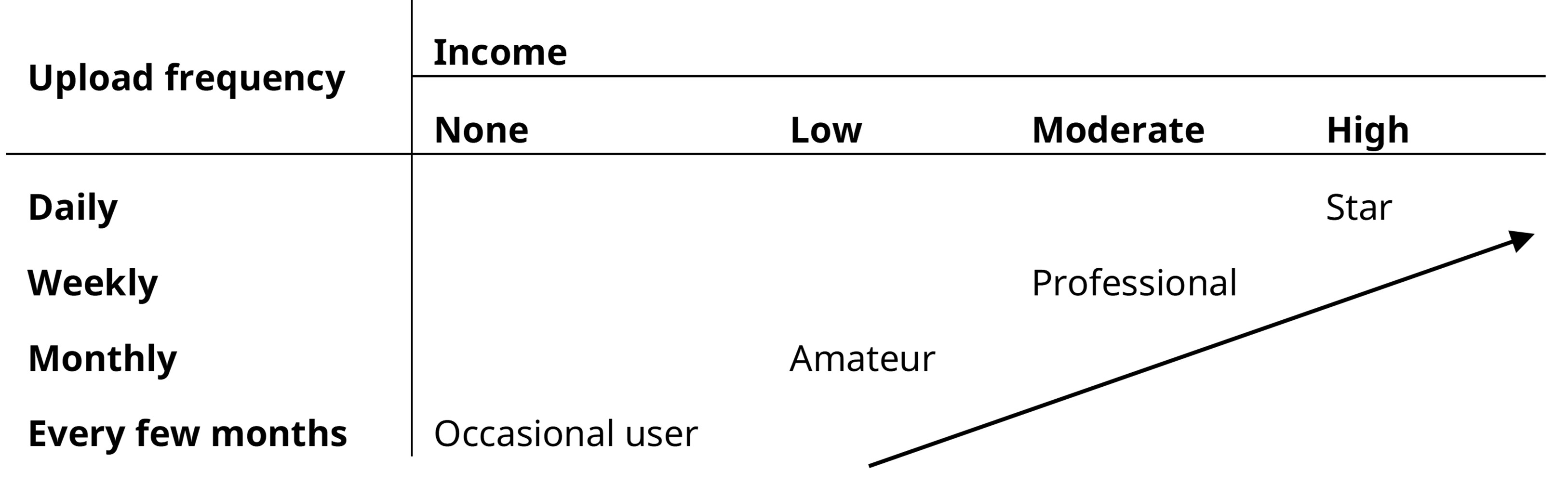

Table 1. Content creators according to type, product and platform

As illustrated in Table 1, content creators are a heterogeneous group. More research is needed to understand their characteristics, working habits and sources of income. They are difficult to define and describe because, in theory, anyone who has an internet connection and uses platforms can be a content creator. Similarly, there is no precise definition of what constitutes “online content”, whether it be professional or amateur creation or as simple as clicking the “like” button on Facebook.

Platforms like YouTube, Facebook and TikTok are considered “passive platforms” (Aguiar, Reimers and Waldfogel 2022), meaning that anyone can upload content and qualify for compensation, as long as they follow a set of guidelines. This format provides opportunities for independent creatives to promote their material. Passive platforms contrast with “curated platforms” where the platforms select (and usually create) the content for consumers. Curated platforms are common in the film industry, with providers such as Netflix and Disney+.

Content creators can be divided into four groups, based on the amount of content produced and expected earnings. Shown in Table 2, the four groups are “occasional users”, “amateurs”, “professionals” and “stars”. This depiction is theoretic and, in reality, content creators can alternate amongst the different categories and their income can be highly unpredictable. Although “occasional users” receive no compensation for their contributions, they are central to viewing and sharing creative content and may contribute a large portion of shared content. They are also central to the extraction of user-generated data that can be commodified and sold for advertising interests. The structure of the aggregate of different content creators resembles a pyramid, with a few high-earning “stars” at the top receiving the most views and subscribers and millions of unremunerated “occasional users” at the bottom.

Table 2. Content creators by income and upload frequency

This table also depicts two groups that are in constant juxtaposition: amateur, routine users who post content in a spirit of participatory culture, and careerists and professionals who post content as part of the cultural industries. Routine users are characterised by networking, online collaboration and sharing, whereas professionals represent corporate concentration, profit-making and the “glamour” of online exposure. Establés et al. (2019, 215) depict well this relationship: “Between these two areas there is a grey area (Scolari 2014) where some people, many of them fans of certain cultural products, transition from the amateur field of the participatory cultures to the professional field of the cultural industries, which characterises the phenomenon of cultural convergence” (Jenkins 2006).

“Participation” has become a key concept in various fields, including user-generated content, crowdsourcing, peer production, fan fiction and citizen science. Despite its widespread use, the term often lacks precision, leading to confusion and inconsistent application. Kelty et al. (2015) provide a framework to analyse and understand the multifaceted nature of participation, identifying seven dimensions: educative dividend, access to decision-making, control of resources, voluntary character, effectiveness of voice, use of metrics and collective, affective experience. “Effectiveness of voice” and the “use of metrics” are critical for creative workers, emphasizing the value-transparent metrics and genuinely incorporating artist feedback into platform policies. For instance, changes in algorithms on YouTube can significantly impact creators' visibility and income, highlighting the need for clear communication and responsive adjustments.

Opposing theories about the impact of platforms on creative work

As a start, it is important to review some predominant theories on the working conditions of creatives on digital platforms. One position, which emerged alongside the initial acceleration of platform growth in the early 2000s, was the notion that platforms would democratize creatives’ access and ability to distribute their work to a global audience (Jenkins 2006; Bruns 2008; Poell, Nieborg and Dijck 2019). Platforms had the potential to expand opportunities for creative employment to anyone with a computer, microphone, camera or smartphone. Bruns (2008, 21) described this as a “participatory mode, which breaks down the boundaries between producers and consumers and instead enables all participants to be users as much as producers of information and knowledge”, what Casilli (2019) calls “produsers”. This position is still relevant today and serves as a rallying cry from the industry for creatives to join platforms. Nowhere is this more telltale than in YouTube's infamous marketing slogan, "Broadcast Yourself".

It is broadly recognized that creative and cultural workers have always faced decent work deficits when compared to other sectors, even before the internet. This relates to the concept of aspirational labour, whereby creatives accept below-average working conditions in exchange for the possibility of a “dream job.” Such work is presumed to offer fame and financial success, while allowing a seamless fusion of personal passion and professional activity. Banks (2007) discusses how creative work is often perceived and treated differently from conventional labour due to its unique characteristics and perceptions of societal value. Creative work is frequently romanticized as inherently fulfilling and self-actualizing, leading to the perception that it is not “real work.” This perception is partly due to the cultural value placed on creativity and the arts, which are often seen as passion-driven rather than economically motivated endeavours. This impression, infused with the ideal that creative work is characterized by autonomy and flexibility, puts creative workers in a vulnerable position. The platformization of cultural workers may have exacerbated this situation, with social media holding out the potential of endless opportunity and instant success in achieving career goals and visibility in the absence of regular and sufficient income.

The media scholar Hesmondhalgh (2010, 270) describes succinctly the paradox that digital workers in the creative industries face, “forms of labour that are characterised by high degrees of autonomy, creativity and ‘play’, but also by overwork, casualisation and precariousness”. In a paper about freelance creative workers in Europe, Gill (2002) claimed that many features of creative work that seem attractive, such as autonomy and aesthetic engagement, were superficial, masked restrictions on career mobility and promoted aspirational disillusion (Gill 2002; McRobbie 2016).

Terranova (2000) even went so far as to describe the "shamelessly exploitative nature" of content creation and described it as “24–7 electronic workshops” coupled with “ruthless casualization”. Under these autonomist theories, free labour is a distinct feature of the cultural economy and a vital yet unacknowledged source of value for capitalist societies (Terranova 2000; Andrejevic 2013; Scholz 2013). Casilli (2017, 3934), speaking in the tradition of the European social contract, describes how the "exclusive focus on free labour has progressively given way to new analyses showing that digital labour is a continuum of unpaid, micro paid, and poorly paid human tasks". Defying these viewpoints, other scholars posit that it is a matter of priority and political economy and that we cannot reasonably label digital media workers as exploited when we compare them to, for example, artisanal gold miners in Africa or sweatshop workers in Indonesia (Hesmondhalgh 2010). Creative work is seen as a choice and a means to earn extra income, whereas other occupations are for survival and pay only subsistence wages. Contributing content to the web is done with full knowledge and responsibility and should be considered a voluntary act. In terms of the benefits so-called "free digital labour" brings, researchers have documented the personal satisfaction and self-worth brought about by contributing to a cultural project, and the opportunity to build new, specialized skills that can lead to higher wages and more career mobility in the long run, essentially a deferred wage (Hesmondhalgh 2010).

These different analyses illustrate the tension between two ways of considering content creators, one that emphasizes the potential positive capitalistic force of industry and employment growth versus one that underlines the potential unstable and unfair nature of work on digital platforms. This contrast shows the complex and often paradoxical nature of this area of study and a reason for the current lack of conclusive evidence or theories on whether digital platforms have weakened or improved the employment situations of creative workers.

A model for understanding how platforms impact working conditions in the cultural industry: Control versus autonomy

This section reviews the conceptual issues that set the basis for understanding how platforms impact working conditions in the cultural industry, building on the definitions and contextual factors described in the previous sections.

Digital platforms and their modalities of interactions with creative workers play an increasingly important role in shaping working conditions. These interactions contain some features that resemble an employment relationship, and some creative workers wholly depend on platforms for their income. However, there is no contractual basis for this relationship, and regulation related to the platform economy does not in general include content creators (see Silberman et al. 2023). Still, more research is needed to understand how and to what extent platforms affect creatives’ working lives positively or negatively and what policy measures can be proposed to enhance working conditions as creative industries inevitably face increasing platformization.

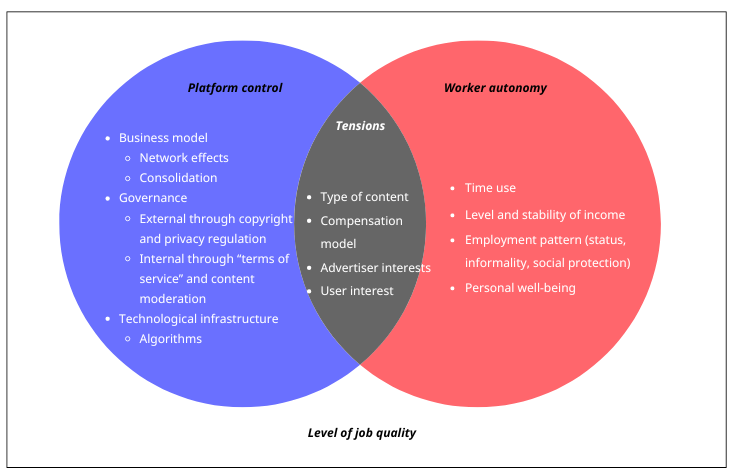

Building on studies related to political economy, culture, employment and labour relations, we need to explore the tensions between platforms’ push for control of content and creative workers’ desire for independence. Platforms’ quest for control is driven by the mission to attract advertisers and subscribers, with governance structures set up to moderate content and consolidate creative industries. The classic effect of consolidation is pressure on labour. From the perspective of creative workers, autonomy has always been a fundamental dimension of the creative process, and platforms have introduced new opportunities for autonomy and flexibility in terms of when, where and how often creatives work. They also strive for autonomy and independence in creative production as well as the freedom to produce and disseminate the content that they want. The friction between control by platforms and autonomy for workers can, in large part, define the working conditions of creatives. Nieborg and Poell (2018, 4277) describe this dichotomy thus: “(A)s cultural production is becoming increasingly platform dependent, the autonomy and economic sustainability of particular forms of cultural production is increasingly compromised”.

The struggle between platform control and worker autonomy serves as the theoretical underpinning of this study (see Figure 1). This research explores these tensions independently, first through the lens of platform operators, showing how they have leveraged systems of markets, governance and technological innovation to become one of the dominant features of the creative sector; and then through the lens of creative workers, to show how industry platformization increasingly affects income, worker status and other employment dimensions. This framework aims to make sense of the tense relationship between platform and worker and the mechanisms and dependencies that ultimately define the livelihoods of creative workers.

Figure 1. Conceptual framework: Dichotomy of autonomy and control of creative work on digital platforms

The level to which platforms impact the working conditions of creatives is contingent on the level of dependency each worker has on the platform. By exploring these relations, we can make basic distinctions between platform-dependent and platform-independent cultural workers. Platform-dependent workers rely on platforms for the creation, distribution, marketing and monetization of content and services, whereas platform-independent workers can create content independent of the platform. Several factors determine the degree of worker dependency, including if a worker relies on one or more platforms, the extent to which the worker derives income from the platform, the opportunity for alternative employment and how much the platform dominates its market.

Digital creative platforms

Building on the conceptual model in Figure 1, this section focuses on how the platform industry managed to capture large market shares and the associated labour before turning to describe how this is impacting the working conditions of content creators. The section is limited in the sense that it is not a comprehensive review of platforms’ capitalistic and business practices, such as investment and financing structures, business strategies or corporate management, and instead focuses on topics that directly affect workers, especially their income and other working conditions.

Platform consolidation

The study of creative workers and platforms is of special interest to the political economy not only because of its perceived impact on labour markets but also because of how global and national systems of institutions and governance set the foundations for the establishment and unparalleled growth of what we might term the digital content industry.

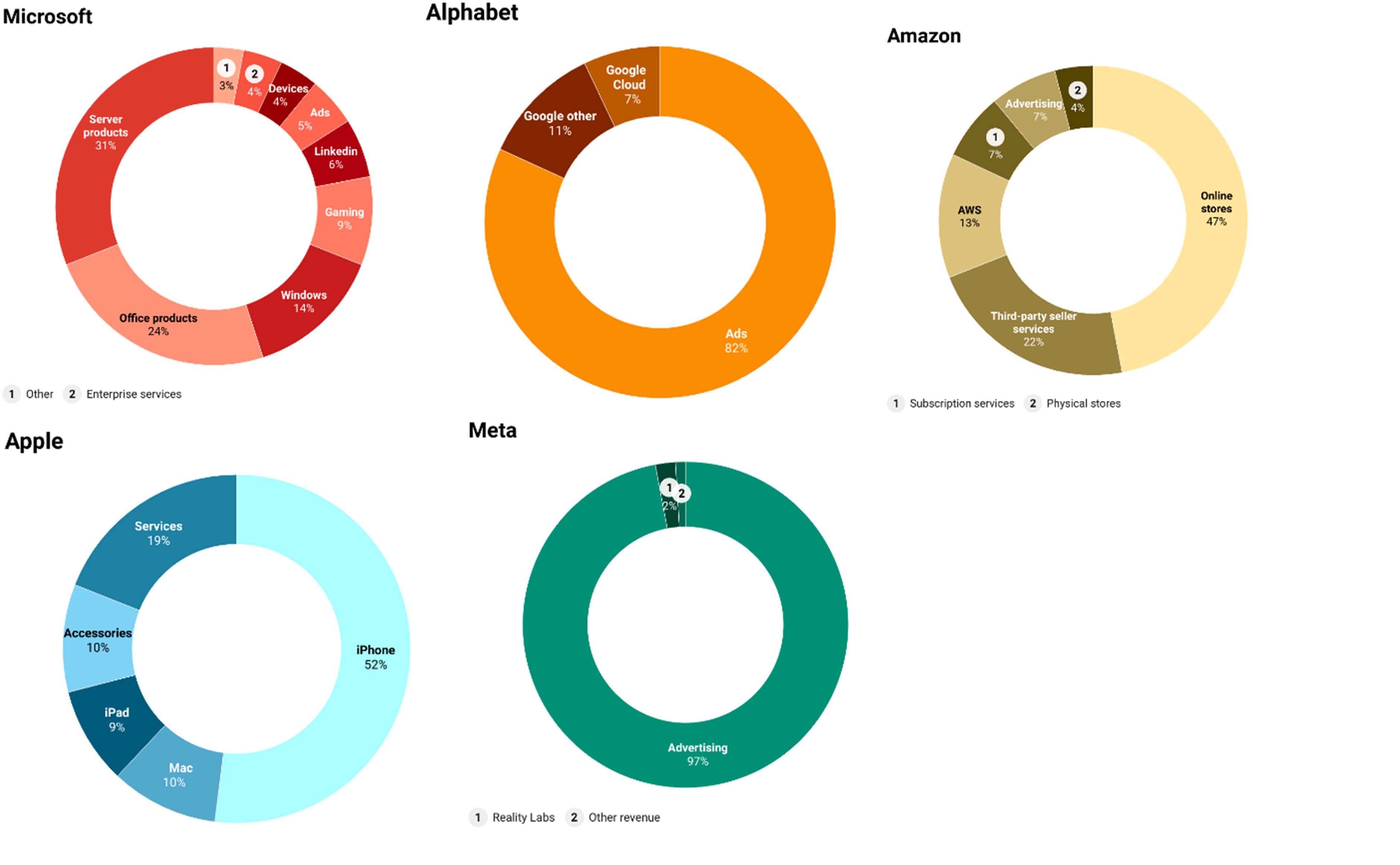

Today, the content industry is increasingly vertical, dominated by the Big Five firms, also known as “GAFAM”: Google, Apple, Facebook, Amazon and Microsoft. Together, they make up over a quarter of the value of the S&P 500 companies and are worth an estimated $7.1 trillion (‘Big Tech’ 2023). These companies develop and operate specific apps, their "infrastructure", which serve as a foundation for market interaction: the Google app store including YouTube, the global video sharing platform; Apple's Apple Music; the social networking sites led by Facebook (now called Meta), which also owns Instagram and WhatsApp; and cloud hosting services by Amazon, Microsoft and Google (Alphabet).

Early innovators such as Facebook's Mark Zuckerberg and Google's Sergey Brin and Larry Page understood the internet's potential as both a consumer platform and a communication enabler. The concept "network effects" describes the phenomenon whereby an increase in users or participants improves the value of a good or service (Katz and Shapiro 1985, 424). The concept is especially relevant for the internet economy, which allows for unlimited access, and the value users place on the internet’s usefulness is directly related to the potential to make connections with other users. The expansion of Facebook provides an extreme example of network growth — from 1 million end-users in 2004, to 10 million in 2006, to 100 million in 2008, more than 2 billion in 2017 and 2.91 billion in 2022.

Similar to platform network effects, consumption of cultural and creative products is also subject to strong network effects whereby the new hit song or the new hit movie gains popularity by word of mouth and positive reviews. This means that digital platforms in the cultural industry, more so than in other industries, are subject to exponential growth because of the confluence of these two types of network effects.

Network effects can be both direct and indirect, with direct effects explained above. In contrast, indirect effects act as catalysts whereby, in addition to the growth of direct participants, in our instance creative workers, developers, buyers and other types of consumers and producers are also drawn to the platform. In the case of creative platforms dedicated to music, as more end users (listeners) join the platform, talent agencies or production companies are pulled into the industry.

Network effects generate “a cycle whereby more users beget more users, which leads to platforms having a natural tendency towards monopolization” (Srnicek 2017, 45). In the case of platform competition, if a winner emerges, it tends to become dominant (Barwise and Watkins 2018). This situation has brought creative platforms under the scrutiny of regulators; however, network effects are not the same thing as a natural monopoly. A natural monopoly is supply-sided, meaning the cost of producing a product or service declines with volume to such an extent that a new entrant cannot afford to price goods at the established dominant supplier prices. Digital platforms also do not limit participants’ choices, and they are free to leave the platform at their will or to join multiple platforms at the same time.

The creative digital industry has seen consolidation due to several high-profile mergers and acquisitions, a "crowding in" of creative companies, and some now consider it an oligopoly. In the ten years leading up to 2020, the GAFAM companies alone acquired more than 400 firms, predominantly in the tech sector (Affeldt and Kesler 2021). Prominent examples include the acquisition of YouTube by Google, and that of Instagram and WhatsApp by Facebook. More recently, Spotify acquired several major podcasting companies in a move to capture a portion of the rapidly expanding podcasting market.

"Coring" and "enveloping" are two strategies platforms used to build market share, leading to the consolidation of the industry. Coring involves building a platform by strengthening and enhancing its basic capabilities and functions. Strong cores have helped platforms gain market share. The iOS operating system and Google search platform are examples of this technique. These basic capabilities attract suppliers and customers who appreciate distinctive goods and services. Envelopment, on the other hand, is a platform's plan for growth by exploiting its core strengths and the skills and functions of other organisations with which it might build strategic alliances. The acquisitions of YouTube by Google and of WhatsApp by Facebook are instances of platform envelopment. YouTube enriches Google searches with helpful and relevant multimedia information, allowing Google to direct searchers to YouTube content, which YouTube uses for advertising. Facebook recognized WhatsApp's messaging strengths and decided to acquire the company rather than expand its messaging resources through Facebook Messenger (Basu and Muylle 2023).

Similar to the United States antitrust lawsuit against Microsoft in the late 1990s and early 2000s, whereby Microsoft was found to operate an illegal monopoly (a decision later overturned upon appeal), tech giants again face antitrust litigation in the United States and Europe. It is claimed that big tech firms are operating monopolies and oligopolies and practice anticompetitive behaviour such as restricting third-party applications (for example, an Apple iPhone can run only the Apple operating system, iOS); misuse of data (for example, collecting detailed user data, making it difficult for new firms to enter); and adjacency (for example, forcing customers to buy additional services linked to their main product, creating price asymmetries). To regulate some of these practices, Europe recently passed the Digital Markets Act1, which sets criteria to identify gatekeepers. Gatekeepers are large digital platforms providing core platform services, such as online search engines, app stores and messenger services. YouTube and TikTok are two of 22 digital services classed as gatekeepers in that, among the other criteria they meet, they have at least 45 million active monthly users. Under the Act, Google must share YouTube data with competitors and ensure that the platform is interoperable with other smaller platforms (Espinoza 2023).

Corporate and market concentration can have substantial effects on labour markets, including downward pressure on wages and lower overall employment. For creative workers on digital platforms, this translates into corporations applying business strategies to capture the most value from content creation, leading to unremunerated and poorly remunerated content. Clearly, “the integration of the GAFAM quintet in the everyday life of billions of global citizens is a continuation and an intensification of corporate concentration, up to the point where ‘platform imperialism’ is becoming a legitimate concern” (Jin 2015; Nieborg and Poell 2018, 4279; Lehdonvirta 2022).

Governance structures

The term platform governance can be defined as “the layers of governance relationships structuring interactions between key parties in today’s platform society, including platform companies, users, advertisers, governments, and other political actors” (Gorwa 2019, 854). Content policies, terms of service, algorithms, interfaces and other socio-technical regimes form the governance mechanisms of today's online infrastructures (Plantin et al. 2018). Following a series of scandals such as Russia’s interference in the 2016 US election and the emergence of “fake news”, substantial research and policy action has been undertaken to understand and define responsibility for material disseminated online and how content should be regulated.

The concept of platform governance has two dimensions. The first pertains to public policy and regulation to provide a legal framework for how platforms operate, with a particular focus on the creation, sharing and distribution of content. Recent regulation has mainly been at the national level, but increasingly regional and transnational level supervision is being discussed to help deal with the offshoring of digital content creation. International standards have become a prominent tool of global governance and, while much of the focus is on technical specifications to protect goods and property, nonphysical fields such as labour have become increasingly important (Graz 2019). The second relates to how platforms govern themselves and the content on their platform to be profitable and sustainable. The governance that online platforms implement significantly affects content creation, distribution, marketing and monetization in the digital realm.

External governance

Issues of public governance are strongly associated with copyright and liability. The most significant piece of jurisprudence that set the basis for the era of content sharing is Section 230 of the US Communications Decency Act from 19962, which provides for what is called "safe harbour protection". The Act absolves "digital service providers" from responsibility for any content posted on their websites by third parties. Proponents of the Act label it as a core pillar of internet freedom and the protection of free speech, both of which have led to the proliferation of the platform business model. Platforms focus on user-generated content (and, increasingly, professionally generated content) and the data it produces to sell advertising. In the realm of the Act, if platforms moderate the content posted on their websites, they then risk being classified as publishers and would lose their safe harbour protection.

The second public regulation with a significant impact on the governance of platforms has been copyright legislation. Copyright is an exception to the immunity that platforms enjoy in content sharing. In essence, copyrighted content can be shared only by the entity that holds the rights to the material, and platforms can be held responsible for the breach if content is uploaded to their platforms by anyone that does not hold the rights.

The focus on the increased onus on responsibility on the platforms for copyright violations represents a counter-cycle from the market liberalization given to platforms stemming from legislation like Section 230. The most detailed and recent example comes from Europe, which adopted Article 17 of the Copyright in the Digital Single Market Directive (European Parliament and Council 2019). The provision sets a new legal regime for the platforms’ content moderation as well as for their contractual relationship with users. The Directive aims not only to hold platforms legally responsible for copyright by modernizing digital copyright laws but also to provide public policy for how platforms moderate and set rules for content, a task that had been left up to the private governance of the platforms.

That there is a major power imbalance between content creators and big online platforms (like Facebook, YouTube, and Instagram) raises the issue of whether the law can and should do more to safeguard users’ rights to their online content. This becomes more apparent when the platform and the creator are not located in the same country. These regulations may damage users who depend on these platforms, especially those who rely on them for a substantial source of income, in addition to hurting freedom of speech and democratic principles. But this private administration of crucial channels for expression to (and via) creative output is scarcely egalitarian. It demonstrates how platforms have power over what content creators produce online and how they can monetize that content (Quintais, De Gregorio, and Magalhães 2023). The reality is these systems of governance tend to protect the intellectual property rights of companies over those of individuals (Poell, Nieborg, and Duffy 2021).

Internal governance

Whereas national laws and practices determine the extent to which platforms are required to govern, platforms themselves ultimately decide how they govern (Poell, Nieborg, and Duffy 2021). Much of how platforms regulate, moderate and interact with content and creative workers is determined by internal governance that is specific to individual platforms. Platforms often use the phrase "terms of service" or "community guidelines" to describe this internal governance, although several studies have referred to it as "platform law" (Belli and Venturini 2016; Kaye 2019).

Terms of service are contractual agreements that are uniformly specified and unconditionally supplied to all users. Given that customers cannot negotiate and have the option only to accept or decline these agreements, it can be said that these conditions of service fall within the legal classification of adhesion agreements. These agreements effectively create a "take it or leave it" dynamic, eliminating the conventional practice of negotiated terms between parties involved in a contract (Lemley 2006; Venturini et al. 2016). Due to their lengthy and complex nature, coupled with the use of legal jargon that is difficult for non-lawyers to comprehend, individuals seldom read these contracts (Bygrave 2015).

One area of terms of service agreements important to content creators concerns the rules on sharing and publishing content and the collecting and processing of personal data. Terms of service of the major digital platforms prohibit images of or references to violence, graphic content, and obscenity; however, there is significant latitude for subjectivity amongst platforms as to types of permissible content. For example, music platforms including Spotify, Apple Music, Tidal and Deezer allow graphic language, including references to violence and sexuality which are criticized for perpetuating negative stereotypes and attitudes towards women.

All platforms have rules for content moderation. Caplan and Gillepsie (2020, 2) define content moderation as "the removal of individual videos or the suspension of entire accounts for violating guidelines around sexual content, violence, harassment, hate speech, or misinformation …; the removal of videos deemed to be a copyright infringement, privacy violations, or spam". Today, content moderation plays an increasingly important role in setting cultural norms and cultural consumption habits. What is allowed and not allowed to be posted on cultural platforms has direct repercussions on creative workers, because when content is rejected, so is the possibility of compensation. This fact intersects with the increasing outcry for platforms to do more to remove fake news, hate speech or sexual misogyny from the internet, making platforms the de facto arbitrators of cultural distribution (Gillespie 2018). The more platforms like YouTube intervene to regulate content, the more precarious the creators’ employment becomes.

Algorithms are the predominant tool used not only to moderate content but also to sort and rank content. In 2022, 500 hours of new videos were uploaded to YouTube every minute and 60,000 new tracks to Spotify every day (Statista 2022). Algorithms and other forms of machine learning such as music and speech recognition allow platforms not only to process massive amounts of information at sufficient speeds but also to adhere to content moderation policies. These policies spell out how the platforms deal with "sensitive content" as well as how they sort and promote content to maximize their profit and appease advertisers (Poell, Nieborg and Duffy 2021).

Platforms also use human editors to moderate and sort content. In general, the more tightly controlled the regulatory space, the more human editors will intervene to choose content. An example of this is the Apple App Store, where tight moderation strongly aligns with Apple's business model, especially the interest in providing "family-friendly" apps. A second example is Spotify's curation of playlists. Human-edited playlists such as "Rap Caviar" and "Mood Booster" receive more subscribers than algorithm-created playlists. Again, the motivation for human intervention in music platforms is predominantly economic. Evidence suggests that both Spotify and Apple Music are exploring models where they hold the rights to songs either through acquisition or production. For example, Spotify has been creating its own music, particularly instrumental tracks for playlists like "Chill" and "Peaceful Piano," which have millions of followers. These tracks are produced in-house and added to popular playlists, potentially replacing tracks from independent rights holders. This strategy allows Spotify to have greater control over content and reduces the royalties it must pay to third-party rights holders.

Content moderation and sorting, either by algorithms or humans, have obvious effects on creative workers. Inclusion in a popular playlist can lead to increased wages, whereas removal or rejection can lead to lost wages and “demonetization”. In a study measuring the success of songs included in Spotify’s most popular playlists, Aguiar and Waldfogel (2021, 657) found that "Spotify has substantial power to influence song success as well as consumption decisions". This affects not only well-known songs but also new artists and songs, given that "Being ranked #1 on the U.S. New Music Friday list raises a song's streams by about 14 million" (Aguiar and Waldfogel 2021). These examples show the inconspicuous link between penalties (such as removal or rejection) and promotions (such as inclusion in popular playlists) from content moderation and the effects on creative workers' remuneration (Caplan and Gillespie 2020).

Going one step further, platforms' algorithms and governance structures tend to be performative in the sense that these systems do more than just manage and regulate content — they actively shape and influence user behaviour, social norms and market dynamics through their design and operational logic (Callon 2010). They do so by embedding certain values, priorities and incentives into their design and operations, to which users then adapt, thereby reinforcing and perpetuating these structures. An example is how platform users may adapt their behaviour based on the feedback they receive from algorithms. For example, content creators on YouTube might produce more clickbait or longer videos if the algorithm favours these formats for higher engagement and monetization. This aspect — whereby creators adjust their creations not to fulfil their own artistic ambitions, but rather to meet the demands of the algorithm — means that the creative workers are constantly conforming to the algorithms criteria to succeed on the platform. Not only does it curtail creativity and innovation of the creator, but it may also limit a user’s listening or viewing experience as cultural products match what is already available. One example is the phenomenon of YouTube "reaction videos" or "meme reviews" where creators react to popular videos, memes, trailers, and other online content. The popularity of reaction videos and similar formats can contribute to a cultural homogenization where viral videos and memes receive disproportionate attention and influence. This may limit the exploration and appreciation of more nuanced or lesser-known cultural products.

Business model

The scale and scope of market competition have exploded for platforms over the past decade (Rietveld and Schilling 2021). Platformization has not only affected creative industries but also required many traditional sectors across agriculture, manufacturing and services to reorganize their distribution through platform ecosystems.

Content sharing had humble beginnings, from Mark Zuckerberg’s initial launch of Face Mash in October 2003 as a networking platform amongst Harvard students to the original concept of YouTube as an online dating service in 2005. The major tech companies and platforms followed similar growth paths, benefiting from “first mover” status and network effects to attract substantial amounts of private venture capital. This rapid early growth was sustained through public offerings in capital markets, allowing the platforms to capture large portions of technology markets.

Platforms are intermediaries, taking advantage of the power of technology and the internet to reduce friction between supply and demand. Multisided market strategies are a key feature of platform business models. “Multisided” means that there are at least two classes of the platform’s main users. Examples of double-sided platforms include eBay and Amazon, which connect buyers and sellers, while examples of triple-sided platforms include YouTube (users, content creators and advertisers) and Uber Eats (drivers, restaurants, and customers).

Platforms have become a dominant business model for the creative industry. However, as described by Hesmondhalgh et al. (2021), platforms still operate and in many cases are bequeathed to the media and entertainment industry’s legacy actors such as Warner and Sony. These legacy actors, as the rights holders for much popular content in music, film, books and images, still have a stranglehold on profit generation in the industry. And despite the “democratization” of the creative industry brought about by any individual ability to distribute content through digital platforms, much of the value of the industry is held by the rights holder and the stars and fan favourites they represent (Poell, Nieborg, and Duffy 2021). This control by record labels, industry professionals and distributors represents a gatekeeping function where relatively few of people and processes determine which content is disseminated and consumed and, consequently, remunerated. In the digital age, new gatekeepers have emerged, including digital platforms, streaming services and algorithms (Siciliano 2022; Siciliano 2023).

Revenue source models

The main element of any business model is the source of revenue. For content platforms there has always been a trade-off among network effects, ensuring more and more users join, and pricing strategy. To induce network effects, most platforms offer free access (the basic or free plan), especially during phases of expansion, and then offer various levels of pricing depending on the customer's perceived utility of the platform. In the logic of the economic theory of supply and demand, the platforms strive to lower prices as much as possible to boost demand and build a consumer base, hence the free base model that most platforms offer (Basu and Muylle 2023).

Figure 2: Revenue sources of big five tech companies (per cent), 2022

Source: Ang 2022

However, for creative platforms to remain competitive, they need to devise a revenue model through one of three main sources: advertising, subscriptions or a product. In the advertisement model, ad space within videos, music or other content is sold to companies to promote their products, whereas in a subscription model, users pay to have ad-free and usually better access to content. Purely streaming platforms (such as YouTube, Spotify and Apple Music) operate on a hybrid revenue model that combines subscriptions and advertising, whereas social media platforms mainly rely on advertising. Today, the model for content creation has shifted towards short video platforms such as TikTok and Instagram (Li, Jiang, and Zhan 2022). In China, short video app users account for 88 per cent of internet users (China Internet Network Information Center 2021). Advertisers have come to prefer short video platforms, because they offer more flexibility on when, where and how often ads can be placed (Li, Jiang, and Zhan 2022).

In the multisided platform structure, revenue can also be extracted from third parties, also known as complementors, who are drawn to the platforms through indirect network effects. The larger the consumer base, the more likely complementors join the platforms. These may include game developers, e-commerce, and advertisers. Revenue can be generated for example through commission from e-commerce merchants or fees from advertisers. A fundamental chicken-and-egg problem affects the evolution of a platform, given that the value proposition for each side (buyers, sellers, possibly others) of a multisided platform depends on the presence and participation of the other (Basu and Muylle 2023).

Access to data, or datafication, is a fundamental part of the platform revenue model. Datafication transforms user activities into valuable data points that can be analysed, packaged and used in various ways (Crain 2019). One primary method through which these platforms commodify user data is by leveraging it to tailor advertising content. Targeted advertising allows platforms to offer advertisers highly specific audience segments, improving the effectiveness of ads and, consequently, the platforms’ attractiveness to advertisers. This targeted approach increases ad revenues significantly, as advertisers are willing to pay a premium for the ability to reach precisely defined demographics with their marketing messages.

Beyond advertising, social media and streaming platforms also capitalize on datafication through by developing sophisticated algorithms that personalize user experiences. By analysing user data, these platforms can recommend content that individuals are likely to enjoy or find engaging, thereby increasing user engagement and time spent on the platform. This extended time not only enhances user satisfaction but also creates more opportunities for exposure to ads, further boosting revenue. Additionally, the data gathered can inform content acquisition strategies, original content production and feature development, ensuring that platforms remain competitive and continue to grow their user base. The value generated from this personalized approach contributes to capital accumulation by retaining current users and attracting new ones, creating a cycle of growth and revenue generation.

Moreover, the commodification of data extends into the broader economy through the sale or sharing of aggregated data and analytics services to third parties. Social media and streaming platforms may offer insights derived from their vast data reserves to businesses seeking to understand market trends, consumer behaviour, and other insights that can inform decision-making. This aspect of datafication opens additional revenue streams beyond direct advertising and subscription fees, contributing to the platforms’ overall capital accumulation. As data becomes an increasingly critical asset in the digital economy, the ability of these platforms to monetize their data through various channels underscores the centrality of datafication in contemporary business models.

However, data applications not only benefit the platforms but also help content creators increase their exposure and remuneration. The Google Analytics service or the Meta Business Suite allows creators to understand their audiences’ viewing habits and design promotional campaigns to increase their fanbases. Conversely, as Poell et al. (2021) observed, the availability of data services may only make creative workers more dependent on platforms to give their work the possibility of standing out in an infinite sea of digital content.

It is possible to extend the network-effect-generating power of user-generated content even further, by paying consumers to contribute content, in the form of reviews, opinions, ideas and solutions. This setup not only can motivate greater participation but also can motivate higher-quality participation, which drives greater sharing and therefore positive network effects. In social network platforms, for instance, the proportion of “lurkers,” or participants who consume without contributing, can be quite high. Paying for content creation can be a way to convert consumers into contributors. Google has done this very effectively, for instance, in its YouTube video platform. People who post popular content are rewarded with money and other resources to develop content.

Remuneration models

Platforms distribute the revenue they earn from advertising and subscriptions to content producers depending on a series of metrics which determine the commercial “success” of a particular piece of content. These metrics include the number of views, number of viewing hours and the number of subscribers as well as other factors determined by an algorithm. Platforms normally do not reveal their exact compensation formulas, and payment terms vary depending on dips and expansion of supply and demand. Platforms can unilaterally change compensation terms, forcing creative workers to constantly adapt their interactions with the platforms as well as their creative material.

One of the most widely known compensation programmes is YouTube’s Partner Programme (YPP). For creators to be able to join YPP, their videos must be watched by the public for 4,000 hours over 12 months and have a minimum of 1,000 subscribers. Once they have reached these metrics, they can activate AdSense, which monetizes the video, enabling creators to receive a share of the advertising revenue. However, there is no fixed revenue share that creators receive, and, as the YouTube partner agreement makes explicit, “There are no guarantees under the YouTube partner agreement about how much or whether you'll be paid” (YouTube partner agreement 2023).

Compensation by platforms in the music industry is widely debated, and YouTube’s policies have recently come under government scrutiny in both the United States3 and the United Kingdom4 over concerns of equitable remuneration. The industry's standardized policy, used by all the major platforms, is a pro rata system whereby the revenue generated from subscriptions, after subtracting a percentage retained by the platform operator, is pooled, then paid out based on the share of listens that a stream generates (Giblin and Doctorow 2022). Thus, the monthly payout per stream is based on its market share across all users, not on the total number of streams (Meyn et al. 2023, 115).

User-centric allocation is an alternative remuneration model whereby the revenue an individual consumer contributes is distributed only according to the listening behaviour of that customer. In this case, a customer’s payments are distributed only to the artists to whom this customer listened (Meyn et al. 2023). Artists whose fans have little diversity in their listening behaviour and low usage will prefer the user-centric remuneration model, since the artists can gather a larger share of the subscription fees from their respective users. In a pro rata remuneration model, a customer with low usage would only marginally affect the royalties of these artists. By contrast, artists whose fans have little diversity but high usage will prefer the pro rata remuneration model, which can increase the artists' share of total streams on the platform.

The selection of a platform's remuneration model direct reflects a broader institutional framework that typifies the music industry. The dominant players remain major production companies and music distributors who, in the United Kingdom, on average retain up to 80 per cent of revenues distributed by the platform, of which up to 20 per cent goes to musicians (UK Parliament: Digital, Culture, Media and Sport Committee – House of Commons 2021). Individual artists are prohibited from uploading their music directly onto major platforms like Spotify and Apple Music and are required first to license their music to professional distributors who propose various shares of royalty payments to the artists.

Creative workers and digital platforms in the labour market

The first part of this paper outlines concepts of governance and market forces that embody the digital content industry and increasingly dictate the employment conditions of creative workers. This section turns to the second part of the research framework, which looks at the main employment dimensions to be considered in an analysis of creative workers and digital platforms. Key variables to consider include employment and job creation, working time, wages, employment status, skills acquisition, gender, social protection, mental health and social dialogue.

The aim is to describe the importance of each dimension as it relates to creatives’ working conditions and show how platforms potentially change and influence each area. The context for the descriptions will be provided by introducing specific examples from well-known platforms while documenting key literature and evidence to identify any patterns in the improvement or decline in working conditions.

Contribution to the economy and job creation

Despite a significant setback caused by the COVID-19 epidemic, the creative sector is growing and represents 3.1 per cent of global gross domestic product (GDP) (UNESCO 2022). In the United States in 2019, arts and cultural economic activities accounted for 4.3 per cent of GDP, an increase of 3.7 per cent from the previous year (US Bureau of Economic Analysis 2023). In Australia, the broader cultural and creative sector contributed US$111.7 billion to Australia’s economy (6 per cent of GDP, end 2016–17) (ILO 2023). The Republic of Korea has a fast-growing cultural and creative sector, with a 2.6 per cent global market share and US$114 billion in revenues (OECD 2021); it was expected to grow 4.4 per cent through 2022 (ILO 2023).

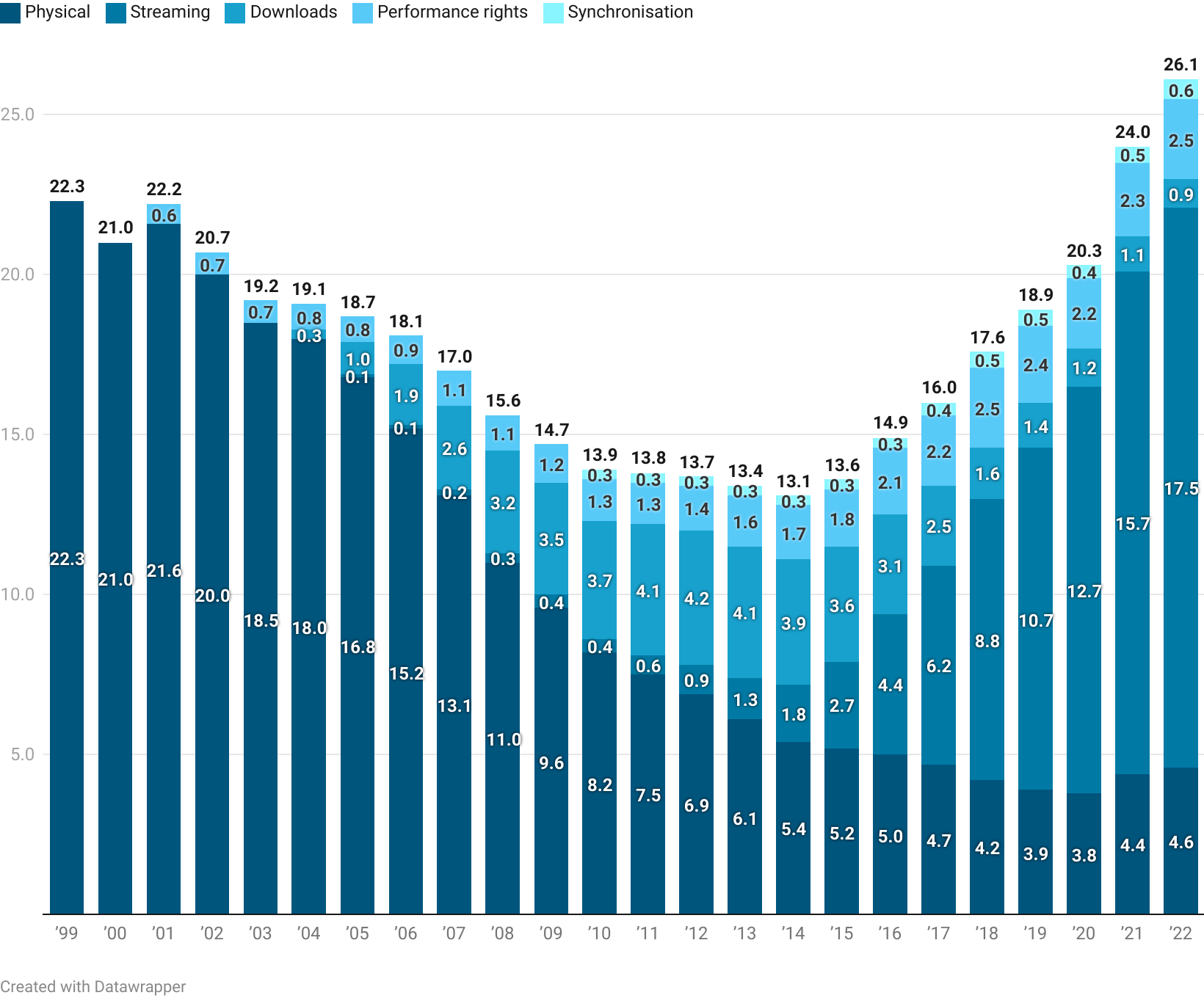

Technology has been important to cultural production since the second half of the twentieth century thanks to continual innovation. The best example might come from the viewing of film, which saw the progression from cinema to TV sets and later VCRs, DVDs and, today, personal computers and streaming. In music, the onset of streaming and digital platforms has revitalized the industry. Figure 3, published by the International Federation of Phonographic Industry (IFPI 2022), visualizes the vital role streaming has played in returning the global recording industry to growth (Hesmondhalgh et al. 2021). Similar patterns can be observed in film and other forms of content production.

Figure 3: Global recorded music industry revenues 1999–2022 (US$ billions)

Source: International Federation of Phonographic Industry, 2022

Yet despite the growth in cultural industries over the past years, creative labour markets are oversupplied, with too many people trying to fill too few positions, leading to higher-than-average levels of unemployment and underemployment. In both the global financial crisis of 2008/09 and the COVID-19 pandemic, creative workers were disproportionately affected compared to workers in other sectors (Liemt 2014; IDEA Consult et al. 2021; ILO 2022a). And with the current speed of technological development, especially in artificial intelligence and creative digital platforms, working conditions could decline further.

The ILO (2022) estimates that the media and culture sector (MCS) accounts for 1.4 per cent of global employment or 46.2 million jobs. The sector accounted for 0.9 per cent of employment in low-income countries, 1.1 per cent in middle-income countries and 3.1 per cent in high-income countries. As a percentage of global media and culture employment, middle-income countries accounted for 56 per cent, followed by high-income countries (39 per cent) and low-income countries (5 per cent). In 2019, the United States accounted for approximately 23 per cent of global employment in the media and culture sector, followed by India (over 21 per cent) and the United Kingdom (10 per cent).

Little empirical research has investigated creative digital platforms’ contribution to overall employment. One could consider that the participatory and democratizing dimensions brought on by platforms mean that increasing numbers consider themselves content creators and are employed in the cultural sector, but this rise may be dominated by an increase only in amateur artists on platforms. As discussed below, income from streaming remains low, and barriers to fair compensation are getting higher.

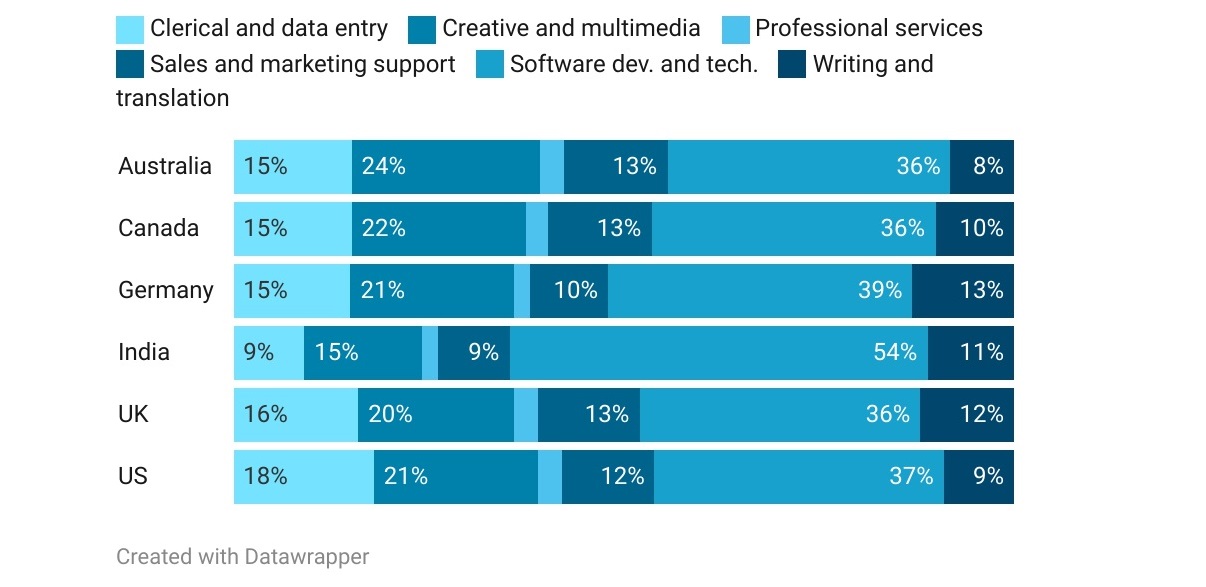

One indicative source estimating the scope of creative employment through digital platforms is Oxford's Online Labour Index (OLI 2020), which tracks the number of projects and tasks posted on the major online labour platforms across countries and occupations. Data is sourced from posted vacancies on freelancer platforms such as upwork.com and mturk.com, and data is analysed according to “demand for jobs” and “supply of workers”. Figure 4 shows the high demand for creative and multimedia work representing 20.8 per cent in that occupational category5, second only after “software development and technology”. Although OLI does not include data from creative platforms such as social media or streaming, content creation is sourced through freelancer platforms and therefore OLI could be a relevant proxy measure for the strong demand for creative content.

Figure 4: Online labour demand, by country and occupation, 2020

Source: OLI 2020

The industry for its part is keen to support the growth of employment opportunities through platforms. A 2019 study published by Oxford Economics and YouTube (Oxford Economics and YouTube 2019) claims that YouTube contributed $16 billion to GDP in the United States (0.075 per cent of total GDP) and created the equivalent of 345,000 full-time jobs.

Income and remuneration

The question of how and how much creative workers are compensated is a key dilemma and a major source of debate amongst decision-makers in the industry, the creators, policymakers, and academics. Many different terms are used, often for the same concept, depending on who is the focus of the discussion: income (labour income), remuneration, wage, compensation and earnings. The most appropriate term here when considering a worker’s perspective is income, which the ILO defines as “the amount that an employed person earns from working” (ILO 2019).

While creators do have to agree to terms of service agreements which may contain elements defining the relationship between the creator and the platform, most platforms do not commit to providing any form of remuneration or benefits. The creative platforms view creators as having “independent contractor” or “self-employed” status where the platform is not required to fulfil obligations considered in employment protection legislation, such as minimum wages or contributions to social security.

As described above, a key part of a creative platform's business model is how content creators should be remunerated, either through the sharing of advertising revenue or through a pro rata or user-centric sharing of subscription fees. These compensation models are based on a modified "piecework" pay approach, whereby, upon reaching a certain threshold, creators are paid either directly or proportionately based on the number of views, subscribers, streams, and so on. However, the conditions and probabilities that affect how many times a piece of content is viewed vary among platforms and depend on factors including the search history and preferences of users, comments and interactions with the content and inclusion of content in popular playlists, for example. This practice is also known as content "curating", mainly controlled by algorithms, whereby content receives a rank or a score that determines how prominently it will appear in an end user's feed. This rank directly influences how much particular content will be streamed, which then influences a creator’s income.

It is widely recognized that only a small segment of content creators receive compensation. As mentioned earlier, the structure of earnings resembles a pyramid, with a small group of high-income 'stars' at the peak, a moderate number of professional and semi-professional creators in the middle tier, and a large base of amateur and non-earning users at the bottom. According to Spotify, "Of the nine million people who have distributed any songs to Spotify, 5.6 million of them have released fewer than ten tracks all-time. Many of these artists are likely hobbyists or early in their careers or may not be leveraging streaming as part of their career paths" (Spotify 2024b).

A similar pattern can be observed in the YouTube Partner Program (YPP), where the threshold for full monetization remains relatively high. Creators become eligible for advertising revenue sharing once they reach 1,000 subscribers and 4,000 valid public watch hours within a 12-month period (YouTube, 2024). While YouTube has introduced lower entry thresholds for limited monetization features, access to meaningful earnings remains concentrated among a smaller group of creators.

Reliable statistics on the scale and distribution of earnings on YouTube remain limited. In 2021, YouTube reported that more than two million creators globally participated in the YPP (YouTube, 2021), but there is little publicly available information on their levels of compensation or on the share of monetized creators relative to the total number of channels.

It is just as difficult to discern the progression in creators’ compensation from platforms over time, whether incomes, on average, are decreasing or increasing. YouTube has grown exponentially since its launch in 2005. It hit 1 billion users in 2013 and 2.3 billion users in 2022 and gained revenue of $29.24 billion in 2022 (Aslam 2023). In 2021, YouTube reported that it had paid $30 billion to creators over the previous three years (Wojcicki 2021), substantially outpacing any of the other major social platforms (Facebook, TikTok, and so on). A study of musicians in the United Kingdom (Hesmondhalgh et al. 2021) reported that the average per-stream rate paid to music creators from 2012 to 2019 has fallen, whereas revenues paid to the recording industry have risen. At the same time, streaming in the United Kingdom has become the main source of revenue for both recording rights holders and music publishing companies.

It's also important to consider the different sources of income that creative workers receive and whether earnings from digital platforms represent primary or secondary sources of income. More generally, it has been documented that many artists, both professional and amateur, have additional income sources from outside the cultural industry and, in some cases, as a more important source of income (Musicians Union 2012; DiCola 2013). Income from digital platforms is one of many different sources of income for creative workers. For example, DiCola (2013) identified 40 different revenue streams of US-based musicians. Other sources include live performances, teaching, composing, and selling merchandise. The evidence on the share of total income that content creators receive from digital platforms is mixed. A Europe-wide survey (Bancroft et al. 2020) found that 90 per cent of workers classified as “performers” receive less than €1,000 per year from streaming, whereas research from the United States (Joplin and Mulligan 2019) found that streaming income, along with earnings from live performances, make up the majority of artist revenues today and that for independent artists, streaming is their primary source of income at 30 per cent. Presumably, artists in conventional artistic occupations such as musicians and photographers would have the opportunity to access more sources of income than a digital content creator who may rely solely on the platform.

As described, creative workers enter into unilateral user agreements that govern, among other things, payment and compensation. These terms can be modified unilaterally by platforms, often with limited notice or transparency, and may result in demonetization or loss of income streams—effectively shifting risk onto creators and, in some cases, leading to unpaid labour.

Demonetization is closely linked to platform content moderation practices. A prominent example is YouTube’s “Adpocalypse” in 2017, when major advertisers—including government agencies and multinational brands such as Coca-Cola and Johnson & Johnson—suspended advertising after their content was shown alongside extremist or harmful material. In response, YouTube significantly tightened its monetization and content policies, leading to widespread demonetization and reduced revenues for many creators.

These changes included stricter eligibility criteria for the YPP, notably the introduction of thresholds requiring 1,000 subscribers and 4,000 watch hours. At the same time, creators affected by demonetization have reported limited clarity and transparency regarding the reasons why specific content was restricted.

The literature also highlights income disparities and differential treatment associated with gender, ethnicity, sexual orientation and political expression (O’Brien et al. 2016; Saha 2018). There is emerging evidence that platform moderation and monetization systems may disproportionately affect certain groups of creators. In the case of YouTube, automated filtering and ad-suitability classifications have been reported to disadvantage creators producing “culturally progressive content”; for LGBTQ creators, this can mean that “any representation of their identity could be deemed sexually suggestive and ad-unsafe” (Cunningham and Craig 2019, 113).

The preceding discussion highlights important research gaps regarding both the levels and distribution of compensation for creators on digital platforms, as well as the question of what constitutes fair remuneration. These patterns have led some authors to question the underlying platform business model, which combines elements of participatory labour with monetization strategies that capture value from user-generated content—often without proportional compensation to creators—particularly through advertising revenues.

Employment patterns

While countries apply different interpretations and applications of employment status, the basic concept separates workers into three statuses: employers, employees and the self-employed (also known as independent contractors or own-account workers). The designation is important because it is the basis for a country's employment law and determines entitlements to rights and protections such as social security, sick pay, vacation and so on. With the emergence of the platform economy and changes in the way work is organized, countries have started to redefine the working relationship (ILO 2023) and adapt national regulations.

Scholars have documented the rise in temporary and part-time employment, wage inequalities, gaps in social protection and other forms of precariousness visible over the past four decades (Castells 1997; Braverman 1998; Standing 2011; Fuchs 2014). This is particularly apparent in the creative sectors where workers are more likely to be self-employed, work part-time or hold multiple jobs inside and outside of the sector (Liemt 2014). However, although there are signals, there is little research to determine if and to what extent this is associated with platformization.

As mentioned above, there is no employment relationship between a creative platform and creator, creators are assumed to be self-employed and income from platforms is rarely a sole source of income. It seems that platforms have inherited and benefited from the notion of creative producers as “entrepreneurs” and from broader industry and platform practices concerning the individualization of responsibility and risk (Nieborg and Poell 2018).

In general, levels of self-employment amongst workers in creative sectors are higher than in total employment. In Europe, 32 per cent of cultural workers are self-employed versus 14 per cent in the total economy (Eurostat 2023). In the United States, creative workers (“artists”) are 3.6 times as likely as other workers to be self-employed (National Endowment for the Arts 2019). Atypical work patterns are more frequent in the cultural and creative sectors and bear “little resemblance to traditional notions of the ‘career’ with their expectations of linear development and progression of the hierarchy” (Gill 2010). Self-employment is associated with higher levels of insecurity and intermittent work. As income-generating opportunities and demand for content grow on digital platforms, levels of self-employment are also expected to increase.

Furthermore, for most creatives income from platforms would not be enough for them to subsist on, and many have multiple jobs. This may include a fixed source of income as an employee and irregular sources of income through "gigs", short-term contracts or freelance work. On creative platforms, some of this gig work is unpaid and aspirational, especially for new entrants who need to invest considerable time and energy to build up an online following and interact with their audience.

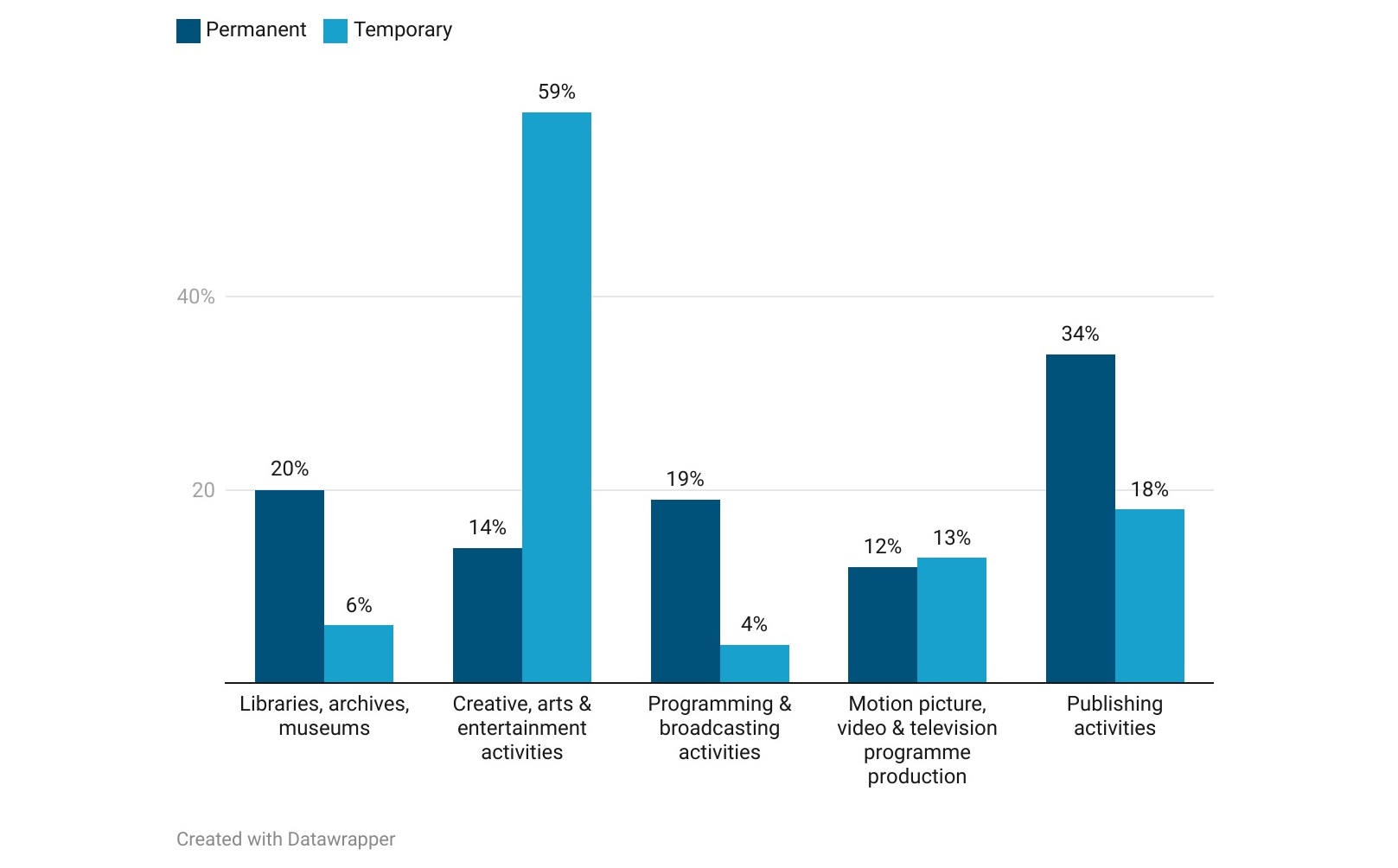

Globally, the creative and arts sub-sector had the largest share of workers on temporary contracts in the media and culture industry. In 2019, this sub-sector accounted for 59 per cent of all workers on temporary contracts in the media and culture industry, followed by the publishing sub-sector. The programming sub-sector had the fewest workers on temporary contracts (see Figure 5).

Figure 5: Sectoral shares by type of job contract, global, 2022

Source: ILO 2022a

An oft-cited argument, especially coming from industry, is that creative workers prefer the flexibility and autonomy that come with self-employment. However, the reality is more complex and causes of self-employment also include the nature of cultural production work, for example, songs and video clips are often one-off endeavours with defined work periods. The causes also include a pervasive trend within the industry to transfer financial risk and obligation from would-be employers and platform operators to the creators themselves.

Informality

Atypical, unremunerated, unprotected or nonstandard employment are all dimensions of informal jobs. Informal jobs are unregistered and unregulated and therefore lack secure employment contracts, workers' benefits, social protection and workers’ representation. Informal employment correlates with self-employment status, especially in low- and middle-income countries, where legal mechanisms to regulate and enforce independent work are weak. The existing data regarding the registration status of workers on digital labour platforms indicates that the proportion of self-employed workers who are not registered, and therefore operate in the informal sector, is larger than the proportion of informal workers in the conventional offline economy. Empirical evidence supporting this assertion has been documented in Eastern Europe (Aleksynska 2021) as well as in India (Berg et al. 2018).

While creative platforms are distinct from digital labour platforms, the causes of informality, such as the lack of an employment relationship and the unpredictable and unstable nature of the work, are similar. Given that much creative platform work is a secondary job or alternative source of income, we would expect some of it to be undeclared and therefore invisible. This means not only that the prevalence of this form of employment could be underestimated but also that workers cannot benefit from social security benefits and that countries do not collect tax revenue.

Informality is a feature mainly of employment in low- and middle-income countries, and its determinants and policy measures are specific to each country. The importance of issues related to the informality of creative work on platforms will however grow as platforms look for cheaper sources of creative content. For example, trends point to the growth of creators in India and China, where YouTube and TikTok are seeing their biggest growth among creators and where informality rates are relatively high.

Gender issues