Unpacking informality

A multidimensional policy decomposition

Acknowledgements

We would like to express our gratitude to Sangheon Lee, Rafael Diez de Medina, Kieran Walsh, Michael Frosch, Florence Bonnet, Sergei Suarez Dillon, Juan Manuel Garcia, Judith Van Doorn, Helmut Schwarzer, and Yves Perardel for their valuable comments. We also benefited from the publication of the anonymized microdata sets by the National Administrative Department of Statistics of Colombia (DANE), as well as from the initial processing carried out by the Data Production and Analysis Unit of the ILO’s Department of Statistics. All errors are the responsibility of the authors.

Abstract

This paper proposes a policy-decomposable approach to analysing informality that preserves the standard binary indicator of informal employment. The additive decomposition highlights (i) the role of the composition effects by status in employment, and (ii) the role of the within status policy-relevant criteria, explaining both the level of informality and its changes over time. We illustrate the method using Colombia’s labour force survey for 2022–2024. Results show that informality is dominated by own-account work in unregistered/non-bookkeeping units, complemented by employees without pension contributions. A nested shift-share analysis indicates that the decline in informal employment over this period was driven mainly by reduced informality among own-account workers -reflecting a small composition effect away from own-account work and improved registration/bookkeeping within the group-, and secondarily by higher employee pension affiliation. The decomposition provides a practical monitoring tool for policy dialogue, clarifying which policy levers are likely to matter most for further reductions in informality.

Introduction

Nearly 60% of the total employed population worldwide is in informal employment (ILO, 2018; ILO, 2023). Although there is increasing availability of statistics and studies about this phenomenon, policy making is not advancing at the same pace. Part of the problem is related to the fact that, as informality is a multifaceted reality, the same terminology has often been used to mean different things, and historical variation in concepts and operational criteria complicated both measurement and policy design.

In terms of measurement, traditionally informality has been analysed through a binary lens, formal versus informal, which often oversimplifies a spectrum of realities. This aggregation is useful for tracking the extent of informality over time and across countries, but on its own it says little about why jobs are informal, the diversity of conditions within the informal (and formal) economy, and which policy levers matter.

This paper proposes a policy-decomposable procedure that keeps the ILO-consistent binary indicator of informal employment and unpacks it into additive components aligned with concrete policy variables usually included in the definition (for example, pension affiliation, paid leave, registration/bookkeeping, tax compliance etc). The ILO methodology is based on information on employment status and use specific criteria in each case, using variables that are related to specific policy dimensions. By recovering the original variables – or unpacking informality - we move from a single headcount rate into a small set of policy related drivers, which allows more targeted, monitorable policy dialogue

We illustrate the approach using Colombia’s GEIH microdata for 2022–2024 and show that the modest decline in informality over this period was driven primarily by a reduction in own-account workers operating in unregistered/non-bookkeeping units, with a secondary contribution from improved employee pension affiliation.

Related literature

The original conceptualization of informality, notably developed through the International Labour Organization (ILO)’s World Employment Programme (WEP) in the early 1970s, treated informality as a broad, complex, and heterogeneous phenomenon. The seminal Kenya Report (1972) recognized the informal sector not as a residual category but as a dynamic, productive, and employment-generating component of the economy.

Crucially, these early analyses viewed informality involving diverse characteristics: enterprise and labour registration, production methods, labour relations, and integration with formal markets.

Despite these multidimensional insights, the empirical toolkit of the time was limited, and most analyses remained qualitative and descriptive, lacking the statistical machinery to measure such complexity systematically.

By the 1990s, the need for international statistical standardization led to more formalized but simplified approaches to defining and measuring informality. The 15th ICLS (1993) defined the informal sector based on the characteristics of production units (i.e., enterprises), primarily household unincorporated enterprises, and also considered criteria such as legal organization/ownership, type of accounts, registration and, in many instances, size thresholds. The 17th ICLS (2003) recognized that the 15th ICLS definition did not fully capture the extent of informal employment and therefore complemented it with a broader job-based concept of informal employment that spans formal sector enterprises, informal sector enterprises and households. In this framework, employees are considered to have informal jobs when their employment relationship is, in law or in practice, not subject to national labour legislation, income taxation, social protection or entitlement to certain employment benefits (e.g., advance notice of dismissal, severance pay, paid annual or sick leave)1.

More recently, the 21st ICLS (2023) adopted statistical standards on the informal economy, defining it around the underlying concept of informal productive activities- that is, productive activities of persons or economic units that, in law or in practice, are not covered by formal arrangements, including forms of work other than employment (e.g., unpaid traineeships, volunteer work, etc). Related to employment, this includes the informal market economy. Importantly, the resolution operationalizes this conceptual core by specifying precise criteria and their combinations to classify economic units, work relationships, and productive activities, and it also emphasizes “the degree of exposure to economic and personal risk due to a lack of effective coverage by formal arrangements”2.

While these standards enabled cross-country comparisons and provided statistical clarity, they often encouraged a binary reporting logic: an enterprise or job was either formal or informal. Even when multiple indicators were collected, - such as access to social protection, business registration, paid annual leave or sick leave, etc - results were typically collapsed into a single categorical outcome. At the same time, the 21st ICLS indicator framework (2023) explicitly promotes complementary indicators that retain the dichotomy but add nuance, for example by reporting the share of employees with a formal main job who have effective access to paid leave benefits, as well as the share of employees with an informal main job who nonetheless have access to some employment benefits.

Now a days, there is increasing consensus that measuring informality through a formal/informal dichotomy fails to capture its multidimensional, heterogeneous, and policy related implications3. The ILO acknowledged this consensus in 2023, when the 21st ICLS (2023) Resolution, broadened the scope of informality statistics to reflect its multidimensional nature and calls for the production of indicators set out in the resolution and its supporting indicator framework, relevant to countries’ policy needs and data systems. These indicators describe degrees of vulnerability, access to protections, and the diversity of informal conditions among workers and economic units, across six dimensions (extent, composition, exposure, working conditions and productivity, contextual vulnerability, and other structural factors).

In practice, there are some interesting emerging approaches. Hamaguchi et al. (2025) propose a Composite Informality Index (CII) based on Multiple Correspondence Analysis, incorporating firm-level traits such as tax registration, business licensing, and bookkeeping practices. Shahid et al. (2020) develop a five-point index to position firms along a continuum from fully informal to fully formal, while Thoto et al. (2021) adopt a multidimensional perspective to capture overlapping degrees of legality. At the household level, Egger et al. (2024) introduce a measure of the depth of informality, defined as the proportion of income or hours worked without social insurance, highlighting household-level income diversification as a key welfare strategy. At the institutional level, the Colombia’s statistical agency (DANE, 2023) developed the Multidimensional Index of Business Informality (IMIE) that applies dual cut-offs to identify firms with deprivations across dimensions such as entry, production, inputs, and taxation. By assigning weights to each dimension, the IMIE enables a granular understanding of where informality is most concentrated, improving the targeting of formalization policies. These emerging approaches aim to developing multidimensional policies or strategies to reduce informality and improve livelihoods. [Normal for body text]

Decomposing labour informality

We propose an additive decomposition of the most common indicator of informality: the share of workers with informal jobs to total employment as defined in the ILO’s international guidelines. It is worth emphasizing that our goal is not to create a new measure or indicator of labour informality, but to decompose the most frequently used indicator into its additive components.

The ILO (2023) defines formal employment as “any activity of persons to produce goods or provide services for pay or profit in relation to a formal job, where the activities are effectively covered by formal arrangements”. This definition can be implemented across different categories of workers as per the 20th ICLS (2018) classification of work relationships4 - namely independent workers, dependent contractors, employees, and contributing family workers - and by combining legal criteria with observable operational indicators that encompass a set of protections or obligations –relevant for each country - as signals of formality.

In practice, the process of measurement can be understood in two steps. First, the sector is classified by the intention of production and the formal status of the economic unit: units with formal recognition (e.g., registration, bookkeeping) are in the formal sector, while the informal sector consists of market-producing economic units that lack such recognition. Second, informal employment is determined at the job level, with operational criteria varying by status in employment: for independent workers (employers, own-account workers), job formality follows the formal status of their unit (i.e., they hold a formal job if they operate in a formal economic unit, and an informal job if they own or operate an informal economic unit); for employees, additional job-level criteria are checked, typically employer contributions to statutory social insurance and, where needed, access to paid annual leave and paid sick leave, to determine whether the job is formal or informal.

Using this approach, an indicator of informal employment is then created by collapsing all these diverse indicators into a single binary variable. This allows the construction of a headcount index at the national level: the share of informal employment as a percentage of the total workforce. This indicator has become increasingly relevant to describe a country’s capacity to create not only jobs, but also quality jobs, in the sense that they comply certain conditions of work captured by these variables.

However, useful as it is, this indicator does not by itself reveal which policies are needed to reduce informality, even though many indicators related to policy dimensions were used in its construction5. Therefore, the challenge is how to perform a multidimensional decomposition that retrieves the fundamental variables used to build the informality dichotomy, in a way that is consistent with current standards on informality measurement .

An application: the case of Colombia

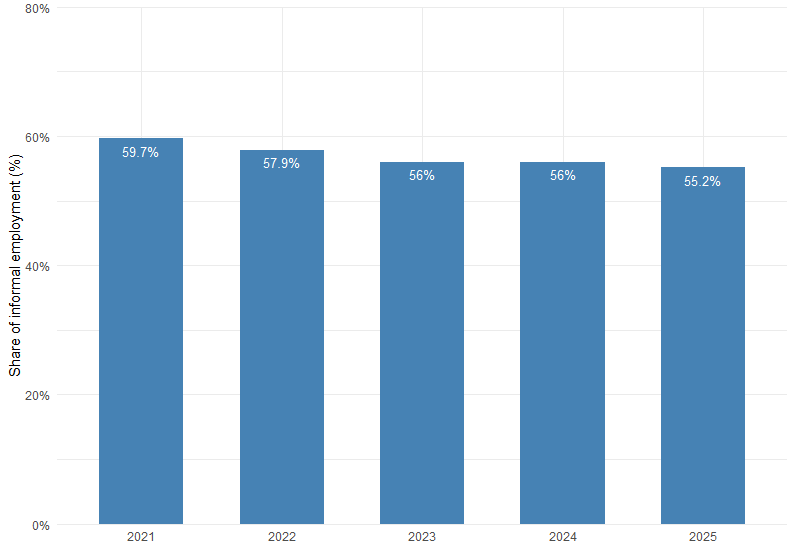

In this section we implement the proposed decomposition using data from Colombia. According to DANE, in Colombia the share of informal employment fell from 59.7% in the period June to August 2021 to 57.9% in 2022 and 55.2% in 2025. Therefore, we can use this reduction to first decompose the aggregate informality rates into its policy components and then use that information to assess what drove the reduction of informality in this period.

Figure 1. Colombia: % of informal employment 2021-2025

Source: DANE (Departamento Administrativo Nacional de Estadística). Extracted 23 October 2025

Note: Data refer to the June-August quarter of each year and use population projections based on the 2018 Census. Information prior to 2021 is not comparable, and thus not included in this graph, because (i) population projections relied on the 2005 Census; (ii) a different operational definition of informality was used; and (iii) earlier published figures covered either 13 or 21 main cities, not the national total.

Data and definitions

The construction of the indicator on informal employment in Colombia used in this document, follows the latest statistical standards introduced above and depends on the status in employment of the worker6. For all employees (EES), including those in the public sector, private sector and domestic work, the primary criterion is contributions to a pension fund (used as an operational measure of contributions to statutory social insurance)7. If the worker reports pension contributions made by the employer on their behalf, the job is formal; if the worker reports no employer contribution to a pension fund, it is informal. When the pension contribution response is recorded as “other / not asked / don’t know / NA”, we apply additional characteristics: the job is considered formal only if the worker reports having access to both paid annual leave and paid sick leave; otherwise, it is informal. In sum, for employees, social-insurance coverage is decisive and, when unknown or unavailable, jointly observed paid-leave entitlements establish formality.

For contributing family workers (CFW), the decisive criterion is effective coverage by formal arrangements, where such arrangements exist in the country. A CFW working in a production unit classified in the formal sector (i.e., units with formal registration with a governmentally established system of registration8 or keeping a complete set of accounts for tax purposes9), the primary evidence is contribution to a pension fund. If such contributions are reported, the job is formal: if not, informal. Paid annual-leave or sick-leave entitlements are not utilised for this status. However, in Colombia, pension contributions targeting CFWs are not yet in place and thus not reported. For CFW working in economic units classified as in the informal sector, the job is informal.

For employers (EPY) the classification relies on the classification of the unit of production. If the unit is registered or keeps accounts for tax purposes, the job is formal; if neither is present, it is informal. Personal entitlements (pension or leave(s)) are not utilised for this status either.

The classification for own-account workers (OAW) depends on the intended destination of production, in particular whether it is mainly for own-final use or mainly for the market. If the intended destination is reported mainly for own-final use, the unit of production is placed in the household sector (i.e., outside employment for pay or profit) and the work relationship is considered informal. If production is mainly for the market, formality is determined by the status of the unit of production: units reporting registration or bookkeeping for tax purposes are formal, and thus the own-account worker is in formal employment; own-account workers in units classified as in the informal sector or in household production are in informal employment.10

Due to the status and the sequence in which they are applied, these rules are mutually exclusive and exhaustive, which facilitates the decomposition by original variables used in the definition in an additive way.

For the calculations, we use the Gran Encuesta Integrada de Hogares (GEIH), the country’s labour force survey implemented by the National Administrative Department of Statistics (DANE), since 2006. The GEIH surveys roughly 240,000 households annually and provides nationally representative information on labour market structure, income, and employment quality. Its design is probabilistic, stratified, and based on multi-stage cluster sampling, ensuring statistical robustness and comparability over time. The survey’s modules on informality build on earlier “1-2-3 Survey” methodologies and were deliberately preserved in the transition to GEIH to maintain consistency with international standards and ILO recommendations.

Before presenting the decomposition, Table 1 provides an overview of descriptive statistics that highlight the high prevalence and heterogeneous nature of informality in Colombia. The data reveal that between 55 and 57 percent of employment is classified as informal, while between 48 and 50 percent11 of employment is in informal or household production units.

Employees12 represent about 50% of total employment, and among them, nearly 70% report employer contributions to a pension fund, while roughly 60 percent has access to paid annual leave and paid sick leave. Note that for employees and for domestic workers, both pension and health coverage were initially considered; however pension contributions by the employer are taken as the determining operationalization criterion, as they more narrowly reflect statutory, employment-link coverage in the country, whereas health coverage is broader and include subsidized and beneficiary regimes which are not held by the employer13. For own-account workers, that represent some 40% of total occupation, formalization remains limited: fewer than half report registration, only 13 percent keep formal accounts for tax purposes, and just over one quarter keep books. By contrast, larger enterprises show higher levels of compliance, with about 80 percent reporting tax or chamber registration and around two-thirds registered as legal entities. Overall, the statistics reveal an employment structure dominated by informality, with limited social protection coverage and weak institutionalization among small units and own-account workers.

Table 1. Colombia. Overview of descriptive statistics. 2022-2024

|

Variable/Indicator |

2022 |

2023 |

2024 |

|---|---|---|---|

|

Total employment (thousands) |

22’032 |

22’788 |

23’036 |

|

Share of employment in informal/household production units (%) |

49.54 |

48.16 |

47.83 |

|

Share of informal employment in total employment (%) |

57.16 |

55.92 |

55.60 |

|

Distribution by Status in Employment (%) |

|

||

|

|

49.98 |

50.51 |

51.22 |

|

1.1 Of employees, contribute to a pension fund |

69.24 |

70.03 |

69.67 |

|

1.2 Of employees, have access to both paid annual and sick leave |

59.42 |

59.07 |

61.87 |

|

1.3 Of employees, have health insurance** |

93.62 |

93.94 |

94.29 |

|

|

2.94 |

2.92 |

3.06 |

|

2.1 Of domestic workers, contribute to a pension fund |

18.58 |

20.62 |

20.19 |

|

2.2 Of domestic workers, have access to both paid annual and sick leave |

17.41 |

18.61 |

18.69 |

|

2.3 Of domestic workers, have health insurance** |

92.12 |

93.71 |

93.98 |

|

|

2.88 |

2.79 |

2.65 |

|

3.1 Of employers, registered unit of production |

51.63 |

51.08 |

52.46 |

|

3.2 Of employers, keeps books of accounts |

41.40 |

44.35 |

43.30 |

|

|

42.2 |

41.74 |

41.07 |

|

4.1 Of own-account workers, registered unit of production |

12.08 |

13.09 |

13.19 |

|

4.2 Of own-account workers, keeps books of accounts |

9.28 |

10.84 |

10.89 |

|

|

1.99 |

2.04 |

2.01 |

Source: Authors calculations based on GEIH processing. Notes: Percentages for the main status-in-employment categories sum to 100. Indented rows report the percentage of workers within each status category who have the indicated characteristic. * By definition, the “employee” category includes domestic workers; however, they are presented separately here because their informality rates differ markedly and they are often subject to specific policy approaches; ** Health insurance includes contributing members of the contributory regime (EPS), affiliates of the subsidized regime, and beneficiaries

Methodology

As mentioned, the empirical definition of informal or formal employment in Colombia is based on employment status14. public employees, employees of private business domestic workers contributing family workers , employers , and own account workers (). As mentioned above, the informality conditions are different in each case.

To express the definition of formal employment mathematically, let denote an individual worker, time and status in employment. Formal employment can be defined using the rules above for each employment status, and individual informality is . Then, the standard calculation of the aggregate informality rate is simply the proportion of informal workers in total employment:

|

|

(1) |

Unpacking policy drivers

To unpack the policy drivers, we need to link these employment status-based criteria with variables related to protection or obligations used in each case15. For that, we split the informal indicator within each status into mutually exclusive reason cells - e.g., employees without pension; employees with no clear indication on pensions (NA) and lacking both paid leave entitlements; employers in unregistered/non-bookkeeping units; own-account without market production or in informal units, etc. We then compute each cell’s share of total informal employment and its contribution to total employment. This partition translates the legal/administrative tests (pension, paid leave, registration/bookkeeping) into additive ‘policy drivers’ of informality that sum exactly to the overall rate. Mathematically, let indicate status membership for worker and represent that worker is in status and informal for reason at time . Define total employment be and employment in status in time be . Then we can define the policy cell contribution, as a share of total employment as:

|

|

(2) |

Note that is the employment share of status s in total employment and is share of employment within due to reason . Then by definition, the policy cell contribution is . Table 2 shows the results of this decomposition. Summing up over reasons , the total contribution of status is .

Table 2. Colombia. Decomposition of informal employment by employment status.

|

Distribution of informal employment by reason for informality |

2022 |

2024 |

||

|---|---|---|---|---|

|

Share in total informality |

Contribution to total informality (pp) |

Share in total informality |

Contribution to total informality (pp) |

|

|

Employees without pension* |

26.13 |

14.93 |

26.87 |

14.94 |

|

Employees without both leave types* |

0.26 |

0.15 |

0.33 |

0.18 |

|

Domestic workers without pension |

4.14 |

2.37 |

4.31 |

2.39 |

|

Domestic workers without both leave types |

0.04 |

0.02 |

0.06 |

0.03 |

|

Employer without registration nor bookkeeping |

2.08 |

1.19 |

1.95 |

1.08 |

|

Own account worker without registration nor bookkeeping |

63.74 |

36.43 |

62.87 |

34.96 |

|

Own account worker in households** |

0.14 |

0.08 |

0.01 |

0.01 |

|

Contributing family workers (working in informal units or without pension) |

3.49 |

1.99 |

3.61 |

2.01 |

|

TOTAL |

100.0 |

57.2 |

100.0 |

55.6 |

Source: Authors calculations based on GEIH processing. Notes: * By definition, the “employee” category includes domestic workers; however, they are presented separately here because their informality rates differ markedly and they are often subject to specific policy approaches. ** For own-account workers, the operationalization follows the 13th ICLS approach.

Applied to GEIH microdata, the policy-reason partition shows a remarkably stable structure between 2022 and 2024. The dominant source of informality is own-account work in unregistered/non-bookkeeping units: it accounts for 63.74% of informal employment in 2022 and 62.87% in 2024, with contributions to total employment of 36.43 and 34.96 percentage points, respectively. The second largest component is wage employees without pension affiliation (26.13% and 26.87% in 2022 and approximately 14.9 p.p. in both years). All other cells (e.g., domestic workers without pension, employers in informal units, and employee without leaves are small and essentially flat.

This decomposition has direct policy implications. On the one hand, because over 60% of informality arises from own-account workers, and informality rates among employees are lower, it is clear that there is a need for policies promoting a reallocation of employment towards higher-productivity jobs with lower informality rates. On the other hand, there is also a need for policies within each status. For own-account workers, operating without registration appears to be the main margin for further reductions in informality, pointing to the need for formalization mechanisms that are tailored to the characteristics and needs of own-account workers and linked to concrete incentives rather than treated as a compliance obligation alone. In addition, pension affiliation among employees remains the largest gap within this group, and gains here require coordinated efforts from the Ministry of Labour and pension related institutions to make affiliation more accessible and to strengthen compliance mechanisms.

Comparing 2022 and 2024. What drives the reduction?

Another important result is that the overall informality rate declines from 57.16% (2022) to 55.60% (2024), a -1.56 p.p. reduction. To assess which policy variables where behind this reduction, we apply the nested shift share analysis following Gupta (1993). For this, we proceed in two steps.

First, we run a simple shift-share analysis at the employment-status level. For this, let denote the within-status informal share, defined as ., and let denote the employment share of status . Then, the contribution of status to total informality, measured in percentage points of total employment, can be expressed as and the overall informality rate can be written as . Using this notation, we can decompose the change in informality as:

|

|

(3) |

The first term of this equation is the change in the informality rate due to changes in status in employment (composition effect) and the second term is the change in informality due to changes within each status (within status effect). Note that we are using time neutral (midpoint) weights as:

The results of this exercise are presented in Table 3 and indicate that the within-status effect for the 2022-2024 decline in informality is -0.97 pp, while the composition effect is -0.59 pp. However, dynamics are heterogeneous across groups. Own-account workers (OAW) account for virtually the entire aggregate decline (-1.54 pp). Their employment share fell (42.20% to 41.07%), generating a sizable negative composition effect (-0.96 pp), and informality within the group also decreased (86.52% to 85.13%), adding a further within-status reduction (-0.58 pp). Among employees (EES), informality within the group fell (30.18% to 29.53%), consistent with improved pension affiliation; however, the expanding weight of employees in total employment offset most of this gain, leaving a small net contribution (0.04 pp). Domestic workers (DOM) show a similar pattern on a smaller scale: a modest decline in within-group informality counterbalanced by a slight rise in their employment share, yielding a negligible net effect (0.04 pp). The status of employers (EPY) contributed also modestly to the reduction through a fall in their employment share with minimal within-group change.

Table 3. Colombia. Shift share analysis by employment status.

|

Status |

Share in employment ‘22 |

Share in employment ‘24 |

Informality within status ‘22 |

Informality within status ‘24 |

Contribution to informality ‘22 |

Contribution to informality ‘24 |

Composition effect |

Within-status effect |

Net change |

|---|---|---|---|---|---|---|---|---|---|

|

EES* |

49.98 |

51.22 |

30.18 |

29.53 |

15.08 |

15.12 |

0.37 |

-0.33 |

0.04 |

|

DOM |

2.945 |

3.06 |

81.05 |

79.31 |

2.39 |

2.43 |

0.09 |

-0.05 |

0.04 |

|

EPY |

2.88 |

2.65 |

41.26 |

40.88 |

1.19 |

1.08 |

-0.10 |

-0.01 |

-0.11 |

|

OAW |

42.20 |

41.07 |

86.52 |

85.13 |

36.51 |

34.97 |

-0.96 |

-0.58 |

-1.54 |

|

CFW |

1.99 |

2.01 |

100.00 |

100.00 |

1.99 |

2.01 |

0.01 |

0.00 |

0.01 |

|

Total |

100.00 |

100.00 |

— |

— |

57.16 |

55.60 |

-0.59 |

-0.97 |

-1.56 |

Source: Authors calculations based on GEIH processing. Notes: * By definition, the “employee” category includes domestic workers; however, they are presented separately here because their informality rates differ markedly and they are often subject to specific policy approaches. EES: Employees; DOM: Domestic workers; EPY: Employers; OAW: Own-account workers; CFW: Contributing Family workers.

These patterns suggest that the reduction of informality in Colombia between 2022 and 2024 involved both a reallocation away from own-account activity and increased formality within it, complemented with improvements among employees.

In the second step of this analysis, following Gupta (1993), we decompose the within-status component to the policy reasons (registration/bookkeeping for OAW, or pension/leave compliance for employees) in order to identify which institutional variables can explain the observed changes.

For this, recall that the within component has the following form: . As we have defined then . Then the within component can be rewritten as and the policy cell contribution can be expressed as the term:

|

|

(4) |

Note that summing over r, returns the within effect of status s, and summing over all s returns the total within component.

The results are shown in Table 4 and indicate that the within–status decline in informality (−0.97 pp) is driven mainly by two policy reasons: (i) among own-account workers (OAW), a reduction in “no registration/bookkeeping” (-0.51 pp), and (ii) among employees (EES), a fall in “no pension” (-0.36 pp). Smaller contributions include domestic workers share without pension (-0.06 pp), a reduction of own account work in households, and a reduction in “no paid leaves” for employees and domestic workers. In the case of Employers (EPY) they exhibit a very small negative within contribution (-0.01 pp) associated with “no registration/bookkeeping,” and contributing family workers (CFW) basically do not change.

Table 4. Colombia. Decomposition of the within status effect into policy drivers.

|

Status |

Policy Reason |

Policy-cell share within status 2022 |

Policy-cell share within status 2024 |

Within status share (pp) |

Within -effect component (pp) |

Within status effect (pp) |

|---|---|---|---|---|---|---|

|

EES* |

No pension |

29.88 |

29.17 |

-0.71 |

-0.36 |

-0.33 |

|

EES* |

No paid leaves |

0.30 |

0.36 |

0.06 |

0.03 |

|

|

DOM |

No pension |

80.35 |

78.30 |

-2.05 |

-0.06 |

-0.05 |

|

DOM |

No paid leaves |

0.71 |

1.01 |

0.31 |

0.01 |

|

|

EPY |

No reg/bkp |

41.26 |

40.88 |

-0.38 |

-0.01 |

-0.01 |

|

OAW |

No reg/bkp |

86.33 |

85.12 |

-1.22 |

-0.51 |

-0.58 |

|

OAW** |

In households |

0.18 |

0.02 |

-0.17 |

-0.07 |

|

|

CFW |

No pension |

100.00 |

100.00 |

0.00 |

0.00 |

0.00 |

|

Total |

-0.97 |

|||||

Source: Authors calculations based on GEIH processing. Notes: * Domestic workers are excluded, as they are reported in a separate category. ** For own-account workers, the operationalization follows the 13th ICLS approach.

These results point to targeted formalization margins rather than diffuse changes. On the employee side, the improvement is predominantly related to pension affiliation, consistent with enhanced compliance within this group. On the self-employment side, the decisive margin is business registration/bookkeeping among own account workers, precisely the channel most responsive to administrative simplification, streamlined registries (e.g., RUT/Cámara), assisted onboarding or digital “e-formality” tools.

The relative weights provide a clear policy ranking: registration/bookkeeping among own account workers explain more than half of the within-status decline, while pension affiliation among employees accounts for about one-third. The remaining items make much smaller contributions. Therefore, the within-status component of the 2022-2024 decline is primarily a business registration story among own-account workers, complemented by increased pension affiliation among employees, while the remaining policy drivers played comparatively minor roles.

Conclusions

Understanding and measuring informality is essential for designing effective employment, tax, and social protection policies. However, traditional classifications of informality have used a binary approach, formal versus informal, which is indispensable for comparability and analysis, but insufficient for policy.

In this paper we propose an additive decomposition of the most common measure of informality: the share of informal employment. By unpacking this aggregate into its constitutive components, the decomposition provides a disaggregated view of two key components: changes in the composition of employment by status in employment, and changes in the protection and registration mechanisms that define formality within each status. The composition component reflects structural transformation and macroeconomic and institutional conditions, whereas the within-status component reflects social protection, regulatory, registration or enforcement measures. This yields a rich empirical basis for policy dialogue and monitoring.

Applied to Colombia 2022-2024, we find that over 60% of informality arises from own-account workers operating outside the perimeter of tax or mercantile registries rather than in employee protections, where pension affiliation remains the largest gap. This approach also allows to assess changes in time. In the Colombian case, overall informality fell by about 1.6 percentage points in the period analysed, an improvement explained almost entirely by an increase in registration (or bookkeeping) of own account workers complemented by an increase in the share of employees with pension affiliation. Other policy related reasons played a minor role.

Two policy implications follow for this specific case. First, as over 60% of informality arises from own-account workers, and informality rates among employees are lower, there is scope and need for policies promoting a change in the structure of employment towards higher productivity jobs with lower informality rates. Second, regarding the policy reasons, enhancing own account registration and bookkeeping (for example, by simplifying and/or digitizing, and linking them to tangible benefits), among own-account workers together with sustaining improvements in pension affiliation among employees are likely to yield the largest reductions in informality.

From the methodological point of view, this approach allows clarifying not only how much formality exists, but also why it exists and provides governments with an evidence-based tool to design policies that promote the transition to formality. More broadly, the approach preserves the well-known definition of informal employment and at the same time reveals why this indicator changes. This makes it suitable for routine monitoring and for evaluating reforms that target the transition to formality focusing on specific levers (e.g., digital registration drives, inspection upgrades, pension onboarding, etc).

Future work can extend this decomposition to other countries where other variables are used. In the case of Colombia, we could assess the sensitivity of this analysis to the introduction of the new ICSE18 classification which brings updated employment status groups.

References

Amaral, P. S., and Quintin, E. (2006). A competitive model of the informal sector. Journal of monetary Economics, 53(7), 1541-1553.

Departamento Administrativo Nacional de Estadística (DANE). (2023). Índice multidimensional de informalidad empresarial (IMIE) 2022. Boletín técnico. Bogotá D.C., 29 de diciembre de 2023.

Díaz, J. J., Chacaltana, J., Rigolini, J., & Ruiz, C. (2018). Pathways to Formalization: Going Beyond the Formality Dichotomy – The Case of Peru. Policy Research Working Paper 8551. Social Protection and Jobs Global Practice, World Bank.

Egger, E.-M., Poggi, C., & Rufrancos, H. (2024). Does the depth of informality influence welfare in urban Sub-Saharan Africa? Oxford Economic Papers, 76, 187–206. https://doi.org/10.1093/oep/gpac052

Foster, J., Greer, J., & Thorbecke, E. (1984). A class of decomposable poverty measures. Econometrica: journal of the econometric society, 761-766.

Gallien, M., & van den Boogaard, V. (2021). Rethinking Formalisation: A Conceptual Critique and Research Agenda. ICTD Working Paper 127. Institute of Development Studies. https://doi.org/10.19088/ICTD.2021.017

Gupta, P.D. (1993). Standardization and decomposition of rates: a user’s manual (N0. 186). US Department of Commerce, Economics and Statistics Administration. Bureau of the Census.

Hamaguchi, N., Hino, H., Piot, C., & Yin, J. (2025). Multi-dimensional informality and heterogeneity of microenterprises in urban Africa. The Japanese Economic Review. https://doi.org/10.1007/s42973-025-00212-w

International Labour Organization (ILO). (1972). Employment, incomes and equality: a strategy for increasing productive employment in Kenya. Geneva.

International Labour Organization (ILO). (1993). Statistics of employment in the informal sector (Report III). 15th International Conference of Labour Statisticians (ICLS). Geneva.

International Labour Organization (ILO). (2003). Decent work and the informal economy (Report VI). Geneva: ILO.

International Labour Organization (ILO). (2003). Adopted guidelines concerning a statistical definition of informal employment. 17th International Conference of Labour Statisticians (ICLS). Geneva.

International Labour Organization (ILO). (2018). Women and men in the informal economy: A statistical picture (3rd ed.). Geneva: International Labour Office.

International Labour Organization (ILO). (2018). Resolution concerning statistics on work relationships (Resolution I). 20th International Conference of Labour Statisticians (ICLS). Geneva.

International Labour Organization (ILO). (2023). Resolution concerning statistics on the informal economy. 21st International Conference of Labour Statisticians (ICLS). Geneva.

International Labour Organization (ILO). (2023) Room document N° 5. Contextualizing informality: The informal Economy Indicator Framework. 21st International Conference of Labour Statisticians (ICLS). Geneva.

Shahid, M. S., Williams, C. C., & Martinez, A. (2020). Beyond the formal/informal enterprise dualism: Explaining the level of (in)formality of entrepreneurs. International Journal of Entrepreneurship and Innovation. https://doi.org/10.1177/1465750319896928

Thoto, F., Jayne, T., Yeboah, F., Honfoga, B., & Adegbedi, A. (2021). Degrees of formalization of agricultural entrepreneurs: Going beyond registration. Journal of Small Business & Entrepreneurship. https://doi.org/10.1080/08276331.2021.1980681